By J-REIT Structure · By Property Grade · By City Tier · By Occupier Sector

City Spotlights: Tokyo · Osaka · Nagoya · Fukuoka

Japan's 57 listed J-REITs reached a combined market capitalisation of approximately JPY 24 trillion as of March 2025 per the Japan Exchange Group, while Tokyo Grade A office vacancy fell to 1.0% in Q3 2025, the lowest in 18 years, and Grade A rents spiked 3.4% quarter-on-quarter to JPY 39,750 the largest single-quarter increase since Q3 2007 as the world's third-largest economy enters its most consequential office rental cycle in two decades.

MARKET SYNOPSIS

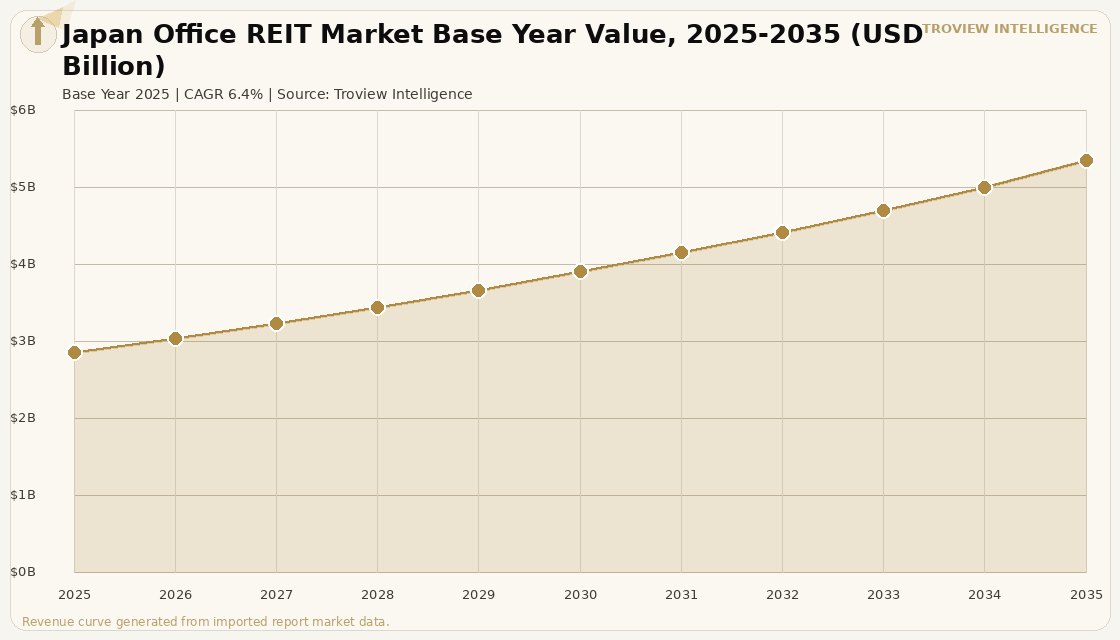

The Japan office REIT market size was USD 2.74 Billion in 2025 and is expected to register a revenue CAGR of 6.4% during the forecast period, reaching USD 5.12 Billion by 2035. Market revenue growth is supported by the structural tightening of Tokyo's office supply-demand balance, which has produced the most consequential rental growth cycle in Japan's commercial property market since the early 2000s. The Japan Exchange Group confirmed that 57 listed J-REITs held a combined market capitalisation of approximately JPY 24 trillion as of March 2025, with office-specialised J-REITs representing the largest single asset class by acquisition value within the J-REIT universe. Tokyo Grade A office vacancy fell to 1.0% in Q3 2025, the lowest in 18 years, while all-grade vacancy declined to 2.1% per Ministry of Land, Infrastructure, Transport and Tourism property market data, driven by large tenant relocations into new CBD supply and strong expansion demand from technology and financial services firms. Osaka all-grade office rents reached a new record high in Q3 2025, rising 1.4% quarter-on-quarter to JPY 14,760, the highest level since the survey began, confirming that Japan's office rental recovery extends beyond Tokyo into the country's second-largest business city. All five of Japan's largest real estate developers Mitsui Fudosan, Mitsubishi Estate, Sumitomo Realty and Development, Tokyu Fudosan Holdings, and Nomura Real Estate recorded or were on track for record profits for their fiscal year ending March 2025, which would be their second consecutive year of record earnings, per an analysis published by Nikkei in 2025.

The Bank of Japan's policy rate hike in January 2025 raised interest rates for the first time in decades, creating a new cost-of-capital environment for J-REITs that historically operated in a near-zero rate environment where the positive spread between office cap rates and funding costs was the primary driver of distributable income growth. Despite this, the Bank of Japan's January 2025 outlook noted that investment appetite in the commercial real estate sector remained strong, with major transactions completing across the office sector throughout the year. Foreign institutional capital inflows into Japanese commercial real estate accelerated in 2025, drawn by the structural vacancy tightening, rising rents, and the continued relative attractiveness of Tokyo cap rates versus equivalent-grade assets in Singapore, Hong Kong, and Sydney. For instance, in January 2026, Nippon Building Fund Inc., Japan, announced the acquisition of two prime central Tokyo office properties from Mitsui Fudosan Co., Ltd. and Kajima Corporation for a total of approximately JPY 46.9 billion, including the newly completed Nihonbashi Honcho M-SQUARE, while simultaneously disposing of the 34-year-old Sumitomo Densetsu Building for JPY 10.0 billion and generating a capital gain of approximately JPY 5.1 billion, demonstrating the asset rejuvenation strategy that defines Japan's leading office J-REITs. These are some of the key factors driving revenue growth of the market.

However, the Japan office REIT market faces structural constraints that moderate the pace of earnings growth for J-REIT investors through the forecast period. The Bank of Japan's progressive policy rate normalisation, which began with the January 2025 rate hike, has increased J-REIT borrowing costs and compressed the net interest margin available to leveraged vehicles whose distributions depend on a positive spread between cap rates and debt costs. The TSE REIT Index closed at 1,691.63 points as of March 31, 2025, reflecting a period of investor caution toward J-REITs as rate expectations evolved, compared to the historical high of 2,612.98 points recorded in earlier years per the Japan Exchange Group guidebook. Japan's demographic profile, with a shrinking working-age population and 82.2% of Japanese workers expressing a preference to continue teleworking per a 2025 World Economic Forum survey, creates a dual dynamic where demand for premium headquarters space strengthens while demand for lower-grade floor space across all cities outside the five central wards of Tokyo faces long-term structural pressure. New Tokyo office supply increased to approximately 200,000 tsubo in 2025 from approximately 75,000 tsubo in 2024 per Miki-Shoji data, representing a significant supply increase that, while absorbed by strong pre-leasing, creates near-term vacancy risk in buildings not achieving pre-lease commitments. These factors substantially limit Japan office REIT market growth over the forecast period.

Japan's office REIT cycle is at its most interesting inflection point in twenty years. The combination of the lowest Grade A vacancy in Tokyo since 2007, rents rising at the fastest quarterly pace since 2007, and a Bank of Japan rate normalisation that is compressing J-REIT unit prices even as underlying property income accelerates creates a classic value opportunity for long-term institutional allocators. The J-REITs that have positioned their portfolios in Tokyo's five central wards with newly delivered or recently refurbished Grade A buildings will compound distributable income at rates that the TSE REIT Index's current pricing does not fully reflect. The rate headwind is real but temporary. The vacancy tailwind is structural." Troview Intelligence Senior Analyst, Japan Office Markets

SEGMENT INSIGHTS

By J-REIT Structure

Office-specialised J-REITs are expected to account for a significantly large revenue share in the Japan office REIT market during the forecast period.

Based on J-REIT structure, the Japan office REIT market is segmented into office-specialised J-REITs, diversified J-REITs with office allocations, and private placement REITs. Office-specialised J-REITs, led by Nippon Building Fund Inc. and Japan Real Estate Investment Corporation, dominate the market by acquisition value and distributable income, concentrating their portfolios in large-scale Grade A office towers in Tokyo's five central wards. Nippon Building Fund Inc. became the first J-REIT in the industry to surpass the JPY 1 trillion mark in total assets under management per the Japan Exchange Group, confirming the scale advantage of office-specialised vehicles relative to diversified structures. Diversified J-REITs with office allocations are expected to register a lower revenue growth rate from their office components than office-specialised vehicles over the forecast period, as the latter's exclusive focus on Grade A Tokyo office assets allows them to capture the full benefit of the rental growth cycle without dilution from retail or logistics performance variability.

By Property Grade

Grade A and newly delivered office assets within J-REIT portfolios are expected to account for a significantly large revenue share in the Japan office REIT market during the forecast period.

Based on property grade, the Japan office REIT market is segmented into Grade A, Grade B, and Grade C office assets. Grade A assets dominate J-REIT revenue and net operating income, with Tokyo Grade A vacancy reaching 1.0% in Q3 2025, and rents spiking to JPY 39,750 per tsubo, the highest since Q1 2020 per Ministry of Land, Infrastructure, Transport and Tourism property data. The green certification premium is accelerating within the Grade A segment, with newly delivered buildings targeting CASBEE S-rank certification by 2027 per Japan's Ministry of the Environment green building framework commanding measurable rent premiums of 12% to 15% over legacy properties according to investor disclosures from Mitsui Fudosan. Grade B assets within J-REIT portfolios are expected to register declining NOI contributions over the forecast period as tenants upgrade to Grade A buildings on lease renewals and J-REIT managers dispose of older secondary assets in favour of newly delivered properties as demonstrated by Nippon Building Fund's January 2026 portfolio rejuvenation transactions.

By City Tier

Tokyo five central wards office J-REIT assets are expected to account for a significantly large revenue share in the Japan office REIT market during the forecast period.

Based on city tier, the Japan office REIT market is segmented into Tokyo five central wards, Greater Tokyo including Yokohama, Osaka, Nagoya, Fukuoka, and other regional cities. Tokyo's five central wards Chiyoda, Chuo, Minato, Shibuya, and Shinjuku represent the primary concentration of J-REIT office assets by acquisition value and account for the majority of Japan office REIT revenue. Osaka is the fastest-growing office J-REIT city by rent growth, with all-grade rents reaching a new record high of JPY 14,760 in Q3 2025 and all-grade vacancy declining to 2.3%, driven by landlords raising rents across both the Umeda and non-Umeda submarkets. Nagoya Grade A and all-grade rents also reached record highs in Q3 2025, with all-grade vacancy falling below 3.0% for the first time since Q2 2021, and Fukuoka vacancy declining 0.6 percentage points to 4.0%, supported by office expansion and relocation activity from companies seeking to establish regional presence outside Tokyo.

Four Cities Shaping Japan's Office REIT Market

| Grade A Vacancy Q3 2025 | 1.0% (18-year low) | Grade A Rent Q3 2025 | JPY 39,750/tsubo |

| New Supply 2025 | ~200,000 tsubo | All-Grade Vacancy Q3 2025 | 2.1% |

Tokyo is the largest and tightest major office market in Asia Pacific, with Grade A vacancy in the five central wards declining to 1.0% in Q3 2025, the lowest since Q3 2007, and all-grade vacancy at 2.1% per Ministry of Land, Infrastructure, Transport and Tourism data. Grade A rents spiked 3.4% quarter-on-quarter to JPY 39,750 in Q3 2025, the largest single-quarter increase since Q3 2007, pushing rents above the most recent peak of JPY 39,000 recorded in Q1 2020. New supply increased to approximately 200,000 tsubo in 2025 from approximately 75,000 tsubo in 2024 per Miki-Shoji market data, but strong pre-leasing and absorption from technology and financial services sector tenants maintained vacancy at historically tight levels. The Nihonbashi, Toranomon, and Yaesu redevelopment corridors are delivering next-generation mixed-use office towers that are attracting pre-construction lease commitments at rents above the all-grade average, supporting the asset rejuvenation strategies of Nippon Building Fund Inc. and Japan Real Estate Investment Corporation.

| All-Grade Rent Q3 2025 | JPY 14,760 (record high) | All-Grade Vacancy Q3 2025 | 2.3% |

| Rent Growth Q3 2025 | +1.4% QoQ | Key Submarkets | Umeda, Nanba, Honmachi |

Osaka is the fastest office rent growth city in Japan in 2025, with all-grade rents recording a new record high of JPY 14,760 in Q3 2025, exceeding the previous all-time high registered in Q3 2020, as landlords raised rents across both the Umeda premium submarket and secondary areas. All-grade vacancy declined to 2.3% in Q3 2025, with Grade A vacancy also falling as the broader flight-to-quality dynamic that defines Tokyo's market is replicating itself in Osaka's core commercial districts. The Osaka Expo 2025 hospitality and infrastructure investment, which the Japan Tourism Agency estimated would generate JPY 2.9 trillion in economic activity, has attracted domestic and foreign corporate commitments to the Greater Osaka region, sustaining demand for headquarters and regional office space in the Umeda and business district submarkets. J-REITs with Osaka office exposure are benefiting from rent re-rating at levels not seen since the mid-2000s cycle.

| Grade A Rent Q3 2025 | Record high (survey history) | All-Grade Vacancy Q3 2025 | 2.4% (below 3% for first time since Q2 2021) |

| Demand Driver | Manufacturing, automotive, aerospace GCCs | J-REIT Exposure | NBF Nagoya Hirokoji Bldg (Nippon Building Fund) |

Nagoya Grade A and all-grade rents reached record highs in Q3 2025, with the all-grade vacancy rate falling below 3.0% for the first time since Q2 2021 per Ministry of Land, Infrastructure, Transport and Tourism data. Demand in Nagoya's office market is driven by companies in manufacturing, automotive, and aerospace supply chains that are establishing or expanding regional operations in Japan's industrial heartland corridor between Toyota City and the Chubu Centrair International Airport complex. Japan's Ministry of Economy, Trade and Industry designated Nagoya as a key node in the Advanced Industry Cluster policy framework, supporting demand for high-specification office space from manufacturers undergoing digital transformation. Nippon Building Fund Inc. holds the NBF Nagoya Hirokoji Building within its portfolio, providing J-REIT investors with direct exposure to Nagoya Grade A office income within a diversified Tokyo-dominated portfolio.

| All-Grade Vacancy Q3 2025 | 4.0% (-0.6pp QoQ) | Growth Driver | Technology, startups, GCCs |

| J-REIT Footprint | Growing via diversified J-REITs | Government Incentive | Fukuoka City startup ecosystem fund |

Fukuoka posted the second-largest vacancy improvement in Japan in Q3 2025, with all-grade vacancy declining 0.6 percentage points to 4.0%, supported by several company relocations into spaces exceeding 100 tsubo as expanding technology and professional services firms committed to Fukuoka as their regional headquarters for western Japan operations. Fukuoka City's startup ecosystem programme, backed by the Ministry of Economy, Trade and Industry's regional innovation cluster initiatives, has attracted technology companies and global capability centres that require modern, collaborative office space in Fukuoka's Tenjin and Hakata central submarkets. The Fukuoka Tenjin Big Bang urban redevelopment programme, a city government initiative to rebuild the Tenjin commercial district with height restrictions relaxed and floor area bonuses for sustainable designs, has created a pipeline of new office supply that is attracting pre-leasing commitments at rents above the existing Fukuoka market average.