By Facility Type · By Geography · By Tenant Sector · By Property Grade

Global pharmaceutical companies pledged USD 475 billion year-to-date in US manufacturing investments by October 2025 as reshoring accelerated, while European life sciences venture capital rebounded to EUR 13.2 billion in 2025, and the Paris region's purpose-built lab and R&D supply is set to more than double by end-2026 to 250,000 square metres a market defined by structural undersupply in emerging clusters colliding with a post-pandemic correction in oversupplied US hubs that is sorting the durable science cities from the speculative builds.

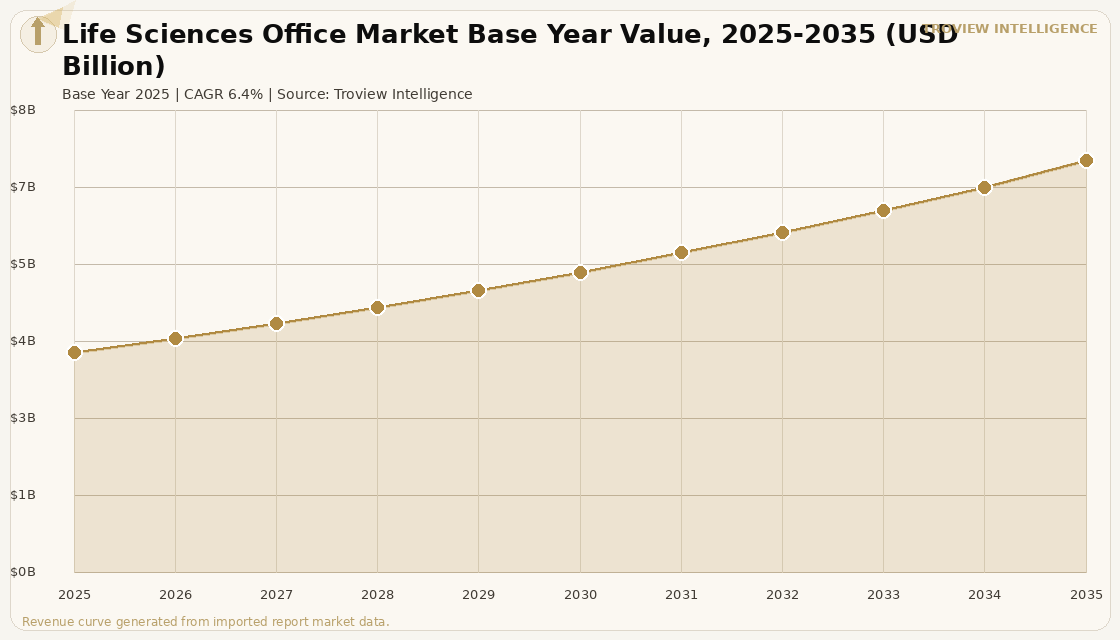

MARKET SYNOPSIS

The global life sciences office market size was USD 3.82 Billion in 2025 and is expected to register a revenue CAGR of 6.4% during the forecast period, reaching USD 7.14 Billion by 2035. Market revenue growth is supported by the sustained expansion of pharmaceutical and biotechnology R&D spending globally, the proliferation of purpose-built lab-office campuses in established science clusters, and government-backed reshoring strategies that are accelerating capital deployment into domestic biomanufacturing and research infrastructure. Global pharmaceutical companies pledged USD 475 billion year-to-date in US manufacturing investments as of October 2025, per US pharmaceutical sector investment disclosures compiled through October 2025, with reshoring momentum sustaining demand for specialised research and development real estate in US biomanufacturing corridors. The European life sciences sector benefits from the EPRA framework identifying European deep tech and life sciences spinouts collectively valued at approximately USD 398 billion, having created more than 167,000 jobs across over 7,300 companies according to Cambridge Innovation Capital data, demonstrating the scale of the underlying tenant base driving laboratory and innovation campus demand. Lab leasing activity in the United States reached 3.4 million square feet in Q4 2024, a 28% year-over-year increase per US government sector employment data and life sciences venture capital funding records, with venture capital into the sector increasing 19% year-over-year to USD 30.4 billion in that period.

Life sciences office real estate is defined by the co-location of laboratory-enabled workspaces, advanced biosafety-classified wet labs, computational biology infrastructure, and conventional office space within integrated campus environments that serve pharmaceutical, biotechnology, medical device, and contract research organisation tenants. The rent premium for life sciences space globally runs 30% to 45% above conventional office space in core urban clusters, reflecting the specialised fit-out costs, enhanced mechanical and electrical systems, and biosafety infrastructure that differentiate purpose-built life sciences buildings from standard commercial office product. European life sciences venture capital rebounded strongly in 2025, with total healthcare and life sciences VC volumes reaching EUR 13.2 billion, up 2.8% on 2024, per European Private Equity and Venture Capital Association data, sustaining the demand pipeline from early-stage biotech companies that require incubator and scale-up lab space in proximity to academic medical centres and clinical trial infrastructure. For instance, in June 2026, Kadans Science Partner, Netherlands, officially inaugurated The Hive at Campus Grand Parc in Villejuif, France, delivering 25,000 square metres of oncology-dedicated laboratory and office space as the first Kadans development in France, with the Paris Saclay Cancer Cluster receiving the first biocluster designation under the French government's France 2030 strategy and the Ile-de-France Region awarding a EUR 1 million grant for the innovation centre within the building. These are some of the key factors driving revenue growth of the market.

However, the global life sciences office market faces structural constraints that limit the pace and breadth of recovery. In the United States, lab vacancy rates spiked to 27% by mid-2025, up 20.4 percentage points over three years with 61 million square feet of available lab space across major US clusters as a pandemic-era construction surge delivered far beyond what venture-backed tenant demand could absorb following the contraction of biotech venture capital from approximately 15% to 7% of US venture dollars. Industry transaction analysis estimates that approximately 18.7 million square feet of the 61 million square feet of available US lab space would likely shift to alternative uses by 2030 due to distress or functional obsolescence, representing a permanent write-down of speculative supply in markets including Boston, San Francisco, and San Diego. AI-native biotechs, which now account for one-sixth of all biotech venture capital deals, demonstrate a lower lab-to-office ratio of 45 to 55 and lease approximately one-third less space per employee than traditional biotechs, reducing the per-dollar-of-investment space requirement that historically correlated with venture capital deployment in life sciences real estate. These factors substantially limit global life sciences office market growth over the forecast period.

The global life sciences office market has developed a tale of two hemispheres. The US is digesting a pandemic-era construction boom that produced 61 million square feet of available lab space against a tenant base that has contracted, become more AI-native, and reduced its per-employee space consumption by a third. That correction is necessary and will take most of the decade to clear. Meanwhile, Europe and specifically Paris, Lyon, Cambridge, and Leiden are operating in the opposite condition chronically undersupplied, with purpose-built lab inventory doubling in the Paris region alone by end-2026, against a venture capital base that grew 2.8% in 2025 and a pharmaceutical investment commitment anchored by Sanofi, Pfizer, and AstraZeneca's combined EUR 1.87 billion France investment pledge. Institutional real estate capital should not treat these as the same market." Troview Intelligence Head of Global Life Sciences Real Estate Research

SEGMENT INSIGHTS

By Facility Type

Purpose-built laboratory and R&D campus assets are expected to account for a significantly large revenue share in the global life sciences office market during the forecast period.

Based on facility type, the global life sciences office market is segmented into purpose-built lab-office campuses, converted industrial and office lab space, incubator and accelerator facilities, biomanufacturing and GMP production buildings, and conventional office with lab fit-out. Purpose-built lab-office campuses dominate market revenue, commanding the 30% to 45% rent premium above conventional office space that reflects their specialised biosafety infrastructure, enhanced HVAC systems, and proximity to academic medical centres and hospital-adjacent research institutions. Converted industrial space represents the fastest-growing supply typology in undersupplied European markets, including the Paris region where the Institut Paris Region has documented conversions of light industrial premises into lab and R&D space as a bridging solution given the shortage of purpose-built inventory. Incubator and accelerator facilities are growing in institutional importance as anchor tenants for multi-building life sciences campuses, with Biolabs opening a healthcare innovation centre at Hôtel-Dieu in central Paris in partnership with AP-HP and the University of Paris.

By Geography

North American life sciences office clusters are expected to account for a significantly large revenue share in the global market during the forecast period, while Europe is expected to register the fastest revenue CAGR.

Based on geography, the global life sciences office market is segmented into North America, Europe, Asia Pacific, and Middle East and Africa. North America retains the largest share of global life sciences office revenue, underpinned by the depth and liquidity of US institutional capital markets, the concentration of pharmaceutical manufacturing capacity in New Jersey, Raleigh-Durham, and Boston, and the federal NIH funding base that anchors academic medical centre demand for lab space. Europe is expected to register the fastest revenue CAGR over the forecast period, driven by chronic undersupply of purpose-built lab real estate in established clusters including Cambridge, Paris, Amsterdam, Leiden, and Basel, where the absence of equivalent speculative development cycles has left vacancy structurally tight and demand from a growing venture-backed biotech tenant base continuing to exceed available supply. European venture capital into life sciences reached EUR 13.2 billion in 2025, up 2.8% on 2024, per European Private Equity and Venture Capital Association data.

By Tenant Sector

Pharmaceutical and established biotechnology companies are expected to account for a significantly large revenue share in the global life sciences office market during the forecast period.

Based on tenant sector, the global life sciences office market is segmented into large pharmaceutical companies, established biotechnology firms, early-stage venture-backed biotechs, contract research organisations, medical device and medtech companies, and academic and hospital research institutions. Large pharmaceutical companies have accounted for their highest share of R&D leasing activity in recent history, signing one-third of midsize and large R&D leases year-to-date through October 2025 as venture-backed leasing has receded from its 2022 peak. The AI-native biotech segment is the fastest-growing tenant category by company count, now representing one-sixth of all biotech venture deals per US venture capital sector data, and demonstrating distinctive real estate requirements characterised by a lower lab-to-office ratio and higher digital infrastructure specifications than traditional wet-lab-dependent biotechs. Contract research organisations represent a structurally stable tenant segment, signing long-term 10 to 15 year leases with expansion clauses that provide income certainty for life sciences real estate developers and institutional investors.

REGIONAL ANALYSIS

NORTH AMERICA LARGEST

| Available Lab Space (US) 2025 | 61M sq ft (industry data) | US Lab Vacancy Rate | 27% (up 20.4pp in 3 years) |

| US Pharma Reshoring Pledge | USD 475 Billion YTD Oct 2025 | Top Clusters | Boston, San Francisco, San Diego, Raleigh-Durham |

North America is the largest global life sciences office market, anchored by the Boston-Cambridge, San Francisco Bay Area, and San Diego clusters that collectively account for the majority of global life sciences venture capital deployment and pharmaceutical R&D leasing activity. The US market entered a correction phase from 2023 onward as pandemic-era speculative construction delivered well beyond venture-backed tenant demand, with lab vacancy rising to 27% by mid-2025 compared to near-zero vacancy in 2022. Occupancy at the three largest US clusters Boston, San Francisco, and San Diego declined to 80.1%, 79.0%, and 73.3% respectively in Q2 2025, from mid-90% levels in 2022. The pharma reshoring dynamic initiated by federal manufacturing policy discussions in 2025 is creating a structural demand signal in specialised biomanufacturing and GMP corridor real estate in New Jersey, Raleigh-Durham, and the Research Triangle, as global pharmaceutical companies committed USD 475 billion year-to-date in US manufacturing investments by October 2025 per US manufacturing sector investment disclosures. Alexandria Real Estate Equities, the largest US life sciences REIT, continues to anchor major campus developments including the Alexandria Center for Science and Technology Mission Bay Megacampus in San Francisco.

EUROPE FASTEST-GROWING

| European Life Sciences VC 2025 | EUR 13.2 Billion (+2.8% YoY) | European Deep Tech & LS Spinouts | ~USD 398 Billion combined valuation |

| Paris Region Lab Supply (existing) | ~108,000 m² (doubling by end-2026) | Key Clusters | Cambridge, Paris, Leiden, Basel, Lyon |

Europe is the fastest-growing major life sciences office region, characterised by chronic undersupply of purpose-built lab real estate across its leading clusters relative to the depth and growth of the venture-backed tenant base. European venture capital into life sciences reached EUR 13.2 billion in 2025, up 2.8% on 2024, per European Private Equity and Venture Capital Association data, sustaining demand from early-stage biotechs requiring incubator and scale-up lab space. Cambridge Innovation Capital data confirms that European deep tech and life sciences spinouts are collectively valued at approximately USD 398 billion, having created over 167,000 jobs across more than 7,300 companies, representing the institutional foundation of the European life sciences real estate tenant base. France is experiencing its largest pharmaceutical manufacturing investment boom in decades, with Sanofi, Pfizer, and AstraZeneca committing a combined EUR 1.87 billion in France investments at the 2024 Choose France summit, and the French government's France 2030 strategy designating five bio-clusters for active development support with 42 biotherapy production projects receiving state funding. The Paris region's existing marketable life sciences real estate area of approximately 108,000 square metres is on track to more than double to 250,000 square metres by end-2026 per Institut Paris Region analysis, representing one of the largest proportional supply increases among European life sciences clusters.

ASIA PACIFIC EMERGING

| APAC Life Science Market (2025) | USD 19.46 Billion sector value | Leading Markets | Japan, Singapore, South Korea, Australia |

| Key Driver | Government R&D mandates, university spinout activity | Fastest-Growing Countries | China, India, Singapore |

Asia Pacific is an emerging growth market for life sciences office real estate, with Japan, Singapore, South Korea, and Australia representing the most institutionally developed clusters and China and India demonstrating the fastest growth rates from a smaller base. Japan's Ministry of Economy, Trade and Industry has designated life sciences as a priority sector under the country's economic security strategy, supporting pharmaceutical company investment in domestic R&D infrastructure and creating demand for laboratory and research office space in Tokyo, Osaka, and Tsukuba. Singapore's Biopolis campus, developed and managed by JTC Corporation as a designated life sciences park, anchors a concentrated cluster of pharmaceutical and biotech company research operations that benefit from Singaporean government R&D incentives and a talent base developed through the National University of Singapore and Nanyang Technological University. The APAC life sciences sector value was USD 19.46 billion in 2025, projected to exceed USD 54.81 billion by 2034 per sector analysis, confirming the scale of the underlying industry that generates demand for specialised research real estate across the region.