By Submarket · By Facility Size · By Occupier Sector · By Cooling Technology

Submarkets: Docklands · Slough · Park Royal · Hertfordshire · East London

London installed data centre capacity reached 2.45 gigawatts in 2025 and is projected to grow to 5.16 gigawatts by 2031 at a 13.21% CAGR, Telehouse International broke ground on a GBP 275 million 33 megawatt West Two facility in Docklands in October 2025, colocation take-up is forecast to reach 183 megawatts in 2025 a 58% increase from 2024 with vacancy expected to fall below 8%, and Equinix's GBP 3.9 billion Hertfordshire commitment is the largest single data centre investment in UK history, creating the largest campus in Europe when operational in 2029 to 2030.

MARKET SYNOPSIS

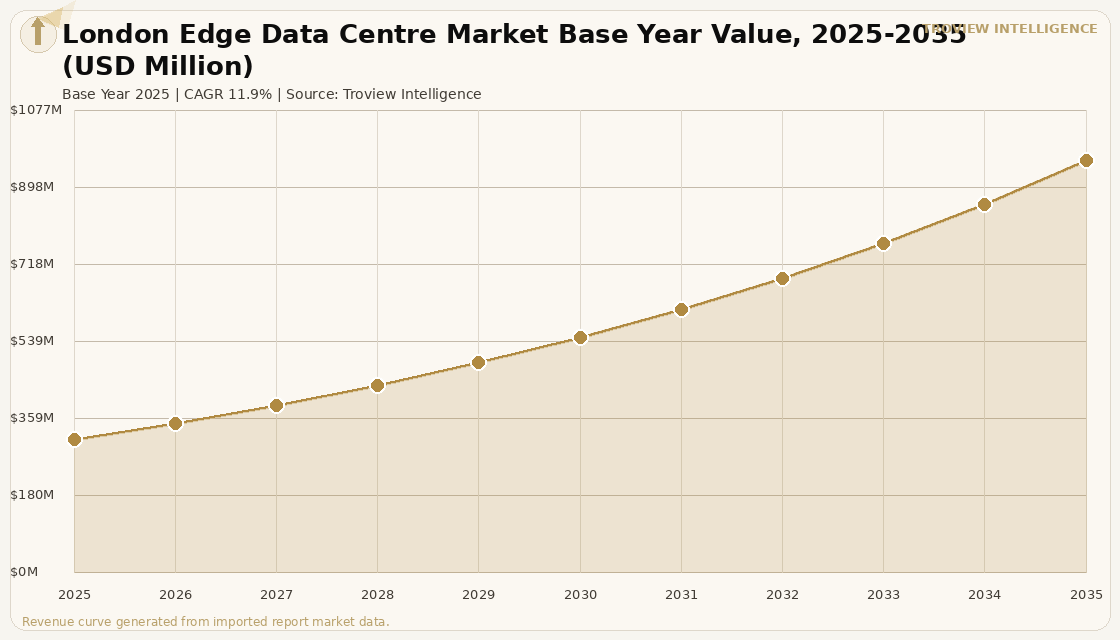

The London edge data centre market size was USD 312.4 Million in 2025 and is expected to register a revenue CAGR of 11.9% during the forecast period, reaching USD 961.8 Million by 2035. London is ranked first among UK data centre markets and second in EMEA, with 2.45 gigawatts of installed capacity across 274 facilities operated by 110 providers as confirmed by verified operator data, with colocation take-up forecast to reach 183 megawatts in 2025 a 58% increase from 2024 demonstrating demand acceleration driven by AI workload requirements from financial services, technology, and media occupiers seeking proximity to the London Internet Exchange. Equinix, Digital Realty, and NTT collectively exceed 45% of installed megawatts, giving the London market a moderately concentrated operator structure with deep interconnection fabric that attracts cloud-on-ramp demand from enterprises requiring sub-5 millisecond metro round-trip connectivity. For instance, in October 2025, Telehouse International Corporation of Europe, a subsidiary of KDDI Corporation, Japan, broke ground on Telehouse West Two, a GBP 275 million nine-storey facility in the Docklands campus adding 33 megawatts across 11,292 square metres of white space equipped for AI and high-performance computing workloads, with two new 132 kV substations and a completion date of 2028, per Techerati reporting of October 2025. These are some of the key factors driving revenue growth of the market.

The London data centre investment market is being shaped by the convergence of AI demand for high-density compute infrastructure and the structural constraints of grid capacity in core Docklands and Slough clusters. Large facilities from 10 to 20 megawatts accounted for 44.95% of London data centre market share in 2025 per industry capacity data, while mega facilities above 40 megawatts are projected to grow at the fastest CAGR of 27.60% through 2031 as hyperscaler demand drives power-density requirements beyond what mid-scale facilities can cost-effectively provision. Peripheral locations beyond the M25 including Basingstoke, Didcot, and Hertfordshire are attracting hyperscale builds by bundling renewable energy proximity and quicker grid connection timelines, with Equinix's GBP 3.9 billion South Mimms campus the most prominent example of this periurban shift in supply geography. Digital Realty's July 2024 Slough acquisition advanced its London metropolitan footprint to 14 facilities, while NTT's May 2025 land purchase for LON2 signals continued multi-gigawatt EMEA expansion planned through London as the regional hub.

However, the London edge data centre market faces structural constraints concentrated in grid access and planning friction. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy price volatility in a market where electricity already costs operators approximately 42 cents per kilowatt hour, materially affecting power purchase agreement negotiations and long-term operational cost modelling for facilities that cannot be relocated to lower-cost geographies. National Grid ESO's pause on new 132 kV connection offers in parts of Greater London and surrounding counties has created connection queues of seven to ten years, requiring developers to either fund bespoke upstream reinforcement at a cost premium of approximately GBP 150 million per 100 megawatt campus or wait for the GBP 9 billion National Grid reinforcement framework awarded in September 2025 to deliver connectivity. Water utility opposition to cooling water consumption in established clusters and local planning friction in Docklands and Slough are causing developers to relocate planned capacity to Park Royal, East London, and Hertfordshire sites where planning goodwill and grid connectivity are more favourable. These factors substantially limit London edge data centre market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "London's data centre market has a paradox at its core. It is the second-largest in EMEA. Colocation take-up is forecast up 58% in 2025. Vacancy is heading below 8%. And yet the primary constraint on growth is not demand it is electricity infrastructure that was built for a pre-AI energy consumption profile. The operators who have grid connections are printing rental growth. The operators who do not are building in Hertfordshire and calling it London. Telehouse's decision to invest GBP 275 million in Docklands in 2025 expanding a campus it has operated for 35 years is the clearest possible signal that the Docklands location premium for interconnection-dependent workloads remains intact even in the face of grid constraints. The question for the next cycle is whether the National Grid GBP 9 billion reinforcement programme arrives in time to support the demand pipeline, or whether the periurban shift to South Mimms and Reading permanently restructures the London supply geography." Troview Intelligence Senior Analyst, London Data Centre Markets

SEGMENT INSIGHTS

Submarket Deep-Dives

| Campus Connectivity | Telehouse West Two | On-Site Power | Cooling Spec |

| 530+ carriers, London Internet Exchange | GBP 275M, 33MW, 2028 completion | 132kV substation, 73MW campus | Indirect adiabatic, PUE ~1.16 |

Docklands is London's primary interconnection submarket, anchored by the Telehouse campus that has operated for over 35 years and currently provides access to 530 carriers and service providers through the London Internet Exchange hosted on-site. Telehouse West Two, the nine-storey GBP 275 million facility breaking ground in October 2025, adds 33 megawatts across 11,292 square metres of white space and two additional 132 kV substations to a campus that already delivers 73 megawatts of total on-site power capacity with an indirect adiabatic cooling system achieving a power usage effectiveness ratio of approximately 1.16. Global Switch's London East, North, and the forthcoming London South facility bring the Global Switch Docklands campus to approximately 126 megavolt-amperes of proposed utility capacity, making Docklands the most power-dense single data centre district in the United Kingdom and one of the most interconnected in Europe.

| Equinix Facilities in Metro | Grid Status | Digital Realty Acquisition | Vacancy Outlook |

| 16 facilities London+Slough | 132kV connection pause constrained | 14 facilities post-July 2024 acq. | Falling below 8% by 2026 |

Slough is the largest single co-location campus cluster in the London metropolitan area, anchored by Equinix's LD4, LD5, LD6, and LD10 campus sites that collectively form one of the most interconnected data centre clusters in Europe for financial services and cloud-on-ramp demand. Digital Realty's July 2024 acquisition of the Slough site advanced its London metropolitan footprint to 14 facilities, positioning the company alongside Equinix as the co-dominant institutional operator in the western London metro corridor. Grid connection constraints in Slough have prompted developers to evaluate alternative locations, with National Grid ESO's pause on 132 kV offers creating queues that affect planned expansion at existing facilities and deter new entrants. Operators in Slough are responding by adopting closed-loop and adiabatic cooling systems that reduce water consumption by up to 80% to mitigate water utility opposition while managing the operational cost impact of electricity at UK average rates of 42 cents per kilowatt hour.

Hertfordshire EQUINIX GBP 3.9BN CAMPUS, EUROPE'S LARGEST PLANNED

| Investment Committed | Campus Size | Power Capacity | Target Operational |

| GBP 3.9 billion (Equinix) | 85 acres, 2M sqft, 250MW | Bespoke 400kV feed | 2029-2030 |

Hertfordshire's South Mimms site represents the most significant single data centre investment in UK history, with Equinix committing GBP 3.9 billion to a 250 megawatt campus across 85 acres that will constitute one of Europe's largest data centre campuses when operational between 2029 and 2030. Planning permission was approved in January 2025 immediately following the UK government's AI Opportunities Action Plan, with the facility designed for three buildings and 2 million square feet of total floor space. The 400 kV bespoke grid feed selected by Equinix added 18 months to the pre-construction timeline and approximately GBP 150 million in additional cost relative to a standard 132 kV connection, demonstrating the scale of the grid investment challenge facing large-format edge data centre development in the Greater London catchment. Construction is targeted to commence in 2027, with the campus expected to create 2,500 construction jobs and 200 permanent positions at full operation.