| TROVIEW INTELLIGENCE | London Medical Office Building Market | Q2 2026 |

| TROVIEW INTELLIGENCE · CITY INTELLIGENCE REPORT |

By Submarket · By Property Category · By Tenant Type · By Investor Class

Submarket Profiles: Harley Street and W1 · Earl's Court and Kensington · Canary Wharf · North London · South West London

Bupa completed two hospital acquisitions in London in 2025 New Victoria Hospital in August and King Edward VII's Hospital in October alongside London Medical on Harley Street in August 2024, creating a three-hospital network with Cromwell Hospital and simultaneously opening a 20,000 square foot Canary Wharf diagnostic hub at 50 Bank Street and a mental health centre at Broadgate Central, Cedars-Sinai opened its first international clinic in London's Harley Street health district in 2026 providing primary care, executive health, and diagnostics, HCA Healthcare UK opened a fertility satellite clinic at 50 Bank Street and a standalone facility at Canary Wharf, US operators now account for approximately 50% of London's independent hospital supply per Investors in Healthcare March 2026, non-NHS inpatient admissions reached a record 939,000 nationally in 2024 with London dominant, and private hospital admissions reached a record high of 245,000 episodes in Q1 2025 per PHIN data confirming that London's medical office building market is undergoing the most significant consolidation and quality upgrade since the private healthcare sector became a meaningful component of the capital's real estate economy.

| Standard License: USD 2,200 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

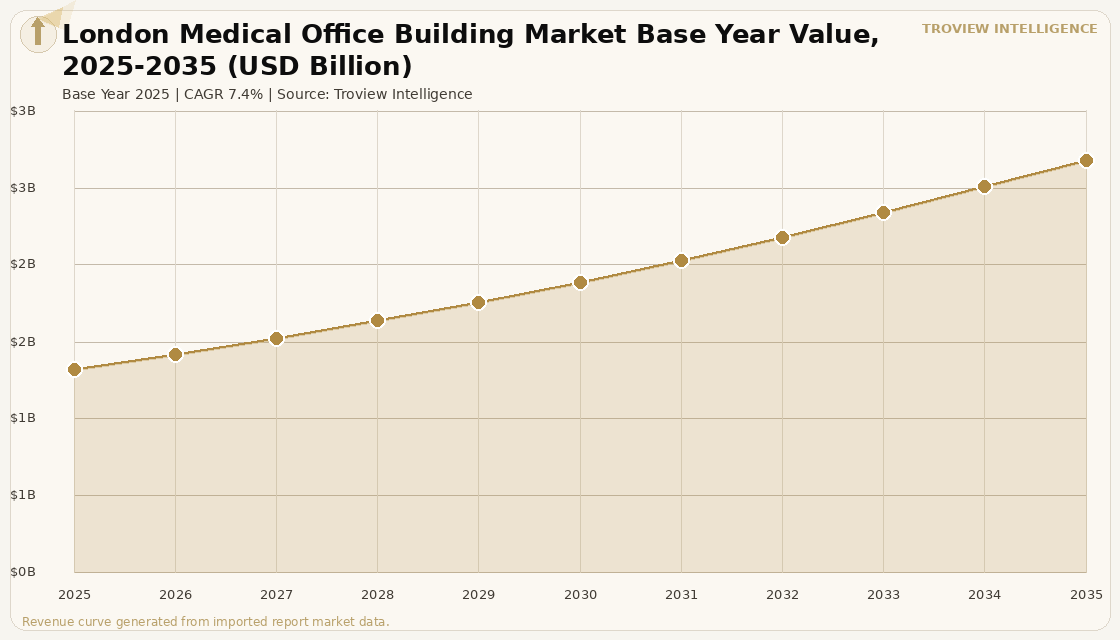

The London medical office building market size was USD 1.49 Billion in 2025 and is expected to register a revenue CAGR of 7.4% during the forecast period, reaching USD 3.02 Billion by 2035. The market encompasses private hospital campuses, specialist physician consulting suite buildings, diagnostic and imaging centre real estate, private outpatient and ambulatory care facility buildings, and GP and primary care medical centre buildings within Greater London, serving the highest concentration of private healthcare demand, international medical tourism, and premium self-pay patient volumes of any city in Europe. London's private medical office building market is distinguished from all other UK medical property markets by the combination of Harley Street's 150-year heritage as a global centre of medical excellence, the concentration of premium private hospitals including Cromwell Hospital, The London Clinic, King Edward VII's Hospital, the Portland Hospital, and HCA Healthcare UK's hospital campus, and the city's role as the primary destination for medical tourists from the Middle East, North America, and Asia seeking high-quality specialist care not available in their home countries. Private hospital admissions reached a record high of 245,000 episodes in Q1 2025 and remained elevated at 234,000 in Q2 2025, with H1 2025 volumes remaining at over 99% of H1 2024 volumes per PHIN data cited by Savills, with levels of activity that would previously have represented all-time highs having now become the normalised level for the sector. Bupa, United Kingdom, acquired New Victoria Hospital in Kingston upon Thames in August 2025, followed by the acquisition of King Edward VII's Hospital in London's Harley Street health district in October 2025, completing its most substantial investment in UK hospital services since 2008 and creating a three-hospital London network alongside Cromwell Hospital that provides an integrated primary-to-secondary care pathway per Bupa company announcements and verified trade press. For instance, in 2026, Cedars-Sinai International, United States, opened Cedars-Sinai Clinic London, its first flagship outpatient clinic outside the US, spanning four floors in London's Harley Street health district to provide primary care, executive health, concierge medicine, diagnostic services, and specialist consultation, with CEO Heitham Hassoun confirming that London serves as a regional hub for UK patients and global travellers including those from the US per Healthcare Today reporting of June 2026. These are some of the key factors driving revenue growth of the market.

US operators now account for approximately 50% of London's independent hospital supply and their presence is expected to grow further, with Sarah Skuse, partner at Bevan Brittan, confirming to Investors in Healthcare in March 2026 that North American capital continues to flow into the UK, with investors viewing the market as undersupplied and strategically important. HCA Healthcare UK, United States, expanded its London footprint by opening a 20,000 square foot outpatient, diagnostic, and dental hub at 50 Bank Street in Canary Wharf serving the 130,000 professionals and 150,000 residents in the local area, alongside a fertility satellite clinic at The Shard Outpatients and a standalone specialist fertility facility at Canary Wharf, and confirming additional new openings as part of a wider programme of growth across HCA UK's London network per Healthcare Today reporting. Bupa simultaneously opened a 20,000 square foot outpatient, diagnostic, and dental hub at 50 Bank Street in Canary Wharf serving as a comprehensive primary-to-secondary care access point, alongside a mental health centre at Broadgate Central intended as the first of 70 UK mental health centres by 2027 with 20 sites operational at launch. The concentration of investment in Canary Wharf medical office buildings with both Bupa and HCA establishing major outpatient facilities at 50 Bank Street simultaneously reflects the structural demand for high-quality medical office space from the financial services employee population of the Canary Wharf estate who prioritise access to premium health services within walking distance of their offices. These are some of the key factors driving revenue growth of the market.

However, the London medical office building market faces structural constraints that temper the pace of new supply addition and limit the geographic distribution of premium medical office development. The Harley Street and W1 medical district faces genuine space scarcity for new medical office development, as the majority of buildings in the area are Georgian townhouses subject to heritage planning restrictions that limit significant structural modifications and prevent the installation of the specialist clinical infrastructure medical gas piping, structural floor loading for imaging equipment, specialist ventilation, and disabled access compliance required for modern clinical medical office standards, creating a structural supply ceiling in the market's highest-value zone. The concentration of premium private hospital and specialist clinic activity in central and south-west London Harley Street, Cromwell Hospital, Portland Hospital, King Edward VII's creates a geographic imbalance in London medical office building investment that leaves East London and North London substantially underserved relative to their resident populations' demand for accessible specialist medical care. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect London's medical office building market specifically through the dampening effect on premium medical tourism from the Middle East and the Gulf Cooperation Council countries, whose patients historically generate the highest average revenue per episode at London's premium private hospitals including Cromwell Hospital, the Portland Hospital, and the London Clinic. These factors substantially limit London medical office building market growth over the forecast period.

London's medical office building market in 2025 and 2026 is being defined by a single strategic insight that multiple operators have reached simultaneously: the private healthcare patient in London does not want to travel to a hospital for a routine outpatient appointment. They want a 20,000 square foot health centre on the ground floor of their office building in Canary Wharf. They want a Cedars-Sinai clinic in Harley Street that can coordinate their care between London and Los Angeles. They want a Bupa mental health centre at Broadgate that is open seven days a week. The hospital is for surgery and complex inpatient care. Everything else should be accessible, local, and clinically premium. Bupa has understood this by building a tiered hospital network at Cromwell, King Edward VII's, and New Victoria, feeding patients through outpatient hubs at Canary Wharf and Broadgate. HCA has understood this by placing fertility satellite clinics at The Shard, Beaconsfield, and the Portland Hospital while simultaneously developing standalone outpatient hubs. Cedars-Sinai has understood this by building a concierge medicine and executive health clinic on Harley Street that coordinates care with its Los Angeles campus. These are not competing strategies. They are different implementations of the same insight about where London's premium healthcare demand is evolving, and the medical office buildings that serve that evolution are the investment case for the next decade." Troview Intelligence Head of London Medical Office Building Research

SEGMENT INSIGHTS

| 03 | SUBMARKET ANALYSIS |

Five Submarkets Defining London's Medical Office Building Geography

| Heritage | King Edward VII's Hospital | Cedars-Sinai London | Landlord |

| 150+ years as global specialist physician consulting district | 56 beds, Harley Street acquired by Bupa Oct 2025 | Harley Street flagship first US clinic outside US, 2026 | Howard de Walden Estate steward of Harley Street district |

The Harley Street and W1 medical district is London's most historically significant and globally recognised medical office building location, with over 150 years of accumulated physician practice, private hospital, and diagnostic clinic concentration that has made it synonymous with premium specialist medical care for both domestic and international patients. The Howard de Walden Estate serves as the primary landlord and long-term steward of the Harley Street health district, managing a portfolio of Georgian townhouse buildings that are let to specialist consultant physicians, private hospitals, and international healthcare operators as medical offices and clinic spaces. King Edward VII's Hospital acquired by Bupa in October 2025 with 56 beds, three operating theatres, and a 2022-opened specialist outpatient and diagnostic clinic is the district's most recent major transaction, adding Bupa's ownership to a street that already hosts the Portland Hospital, the London Clinic, and hundreds of independent specialist physician consulting rooms. Cedars-Sinai International's 2026 opening of its first international flagship clinic in the Harley Street health district four floors of primary care, executive health, diagnostics, and concierge medicine confirmed that US healthcare operators view Harley Street presence as a prerequisite for credible participation in London's international medical tourism market, with the Howard de Walden Estate's CEO noting that Cedars-Sinai's opening reflects growing demand from leading international providers to establish a presence in the area per Healthcare Today reporting.

EARL'S COURT AND KENSINGTON (CROMWELL HOSPITAL CAMPUS) LONDON'S PRIMARY TERTIARY PRIVATE HOSPITAL HUB

| Cromwell Hospital | Recent Investment | International Patients | Specialty Profile |

| Bupa flagship tertiary asset complex, oncology, cardiac, ortho | Extension into adjoining Lexham Gardens building | Primary target: Middle East, US, global HNW | ICU, robotic surgery, oncology partnerships, advanced diagnostics |

Earl's Court and Kensington form the primary cluster for London's tertiary and complex private hospital medical office real estate, anchored by Cromwell Hospital Bupa's flagship tertiary asset and the most clinically advanced private hospital in London by the complexity of surgical and diagnostic services offered. Cromwell has shifted over the past five years from lower-acuity elective activity toward more complex care including intensive care unit expansion, robotic surgery capability, oncology partnerships, and expanded diagnostics, positioning it as Bupa's flagship tertiary asset that handles the most complex surgical cases from Bupa's three-hospital London network per Bupa CEO Philip Luce's confirmation to Investors in Healthcare in March 2026. The hospital's recent capital investment includes the opening of a new extension into the adjoining Lexham Gardens building, expanding the facility's footprint and demonstrating Bupa's willingness to invest in adjacent real estate acquisition when it supports the clinical strategy of the flagship campus. Cromwell's international patient profile serving Middle East, US, and global high-net-worth patients who choose London specifically for tertiary care capabilities not available in their home countries makes the hospital's medical office building real estate value directly sensitive to the Iran-US geopolitical tensions and Middle East travel patterns that CoStar confirmed affect London airport hotel RevPAR, with the same geopolitical dynamic affecting Cromwell's patient volumes and medical office building income.

| Bupa Canary Wharf | HCA Canary Wharf | Catchment | Growth Driver |

| 20,000 sqft GP, specialist, diagnostics, dental (50 Bank St) | Fertility satellite clinic, standalone 50 Bank St/Canary Wharf | 130,000 professionals and 150,000 residents | Corporate health plan demand from financial services employees |

Canary Wharf and East London represent the fastest-growing medical office building submarket in London, driven by the concentration of financial services and professional employees in the Canary Wharf estate and the emerging tech and creative economy presence in Shoreditch, Whitechapel, and the surrounding East London districts whose workers generate corporate health plan demand for accessible, premium outpatient medical services adjacent to their offices. Bupa opened its Health Care centre at Canary Wharf at 50 Bank Street integrating primary care, secondary specialist services, and dental care under one roof for the 130,000 professionals and 150,000 residents in the local area per Healthcare Today reporting, providing a comprehensive health access point that co-locates GP consultations, specialist referrals, diagnostics, and dental services in a single 20,000 square foot ground-floor medical office facility. HCA Healthcare UK simultaneously established a fertility satellite clinic in the Canary Wharf area, joining its network of fertility satellite clinics at The Shard Outpatients, the Beaconsfield Clinic, and the Portland Hospital, with HCA CEO John Reay confirming additional new openings as part of a wider programme of growth across HCA UK reflecting the company's confidence in the future and commitment to meeting rising demand per Healthcare Today reporting. The simultaneous arrival of Bupa and HCA in Canary Wharf's medical office building market establishes the 130,000-professional Canary Wharf estate as a proven demand location for corporate-serving outpatient medical office buildings, with the format expected to replicate across other major London office districts including the City, Midtown, and South Bank.

| HCA Royal Free London | The Shard Outpatients | Independent Sector | Primary Care |

| Private patients unit on Royal Free NHS campus | HCA fertility and specialist clinic at The Shard | Hampstead, Highgate independent specialist practice cluster | PHP-Assura GP surgery portfolio in North London |

North London and Hampstead represent London's primary medical office building submarket for NHS-private partnership facilities and the independent specialist consultant practice cluster serving North London's high-net-worth residential population. HCA Healthcare UK's private patients unit at the Royal Free London NHS Foundation Trust campus in Hampstead exemplifies the NHS-private partnership medical office building model, where private healthcare operators lease space within NHS hospital campuses to serve insured and self-pay patients alongside the NHS patient population, generating rental income for the NHS trust while providing HCA access to Royal Free's specialist clinical capabilities. The PHP-Assura combined portfolio holds a proportion of its 1,200-plus UK primary care assets in North London, with NHS-backed GP practices on long-lease NHS rent-reimbursed terms constituting the most income-secure medical office building tenancy in the submarket. The independent specialist practice cluster in Hampstead and Highgate serving North London's affluent residential population of medical professionals, financial executives, and international residents generates demand for standalone specialist physician consulting suite buildings that complement the hospital-campus and outpatient hub formats of the central London and Canary Wharf submarkets.

SOUTH WEST LONDON (KINGSTON, RICHMOND, WIMBLEDON) NEW VICTORIA HOSPITAL, SUBURBAN PRIVATE HEALTHCARE MOB GROWTH

| New Victoria Hospital | Specialty Profile | Target Patient | Growth Driver |

| Kingston upon Thames acquired by Bupa Aug 2025 | High-volume elective: orthopaedics, gynaecology, gastroenterology | Insured and self-pay, particularly MSK and routine surgical | South West London residential wealth, NHS waiting list relief |

South West London and the Kingston, Richmond, and Wimbledon corridor constitute London's primary suburban private hospital and medical office building growth zone, anchored by Bupa's August 2025 acquisition of New Victoria Hospital in Kingston upon Thames an independent private hospital known for specialist services in gynaecology, gastroenterology, orthopaedics, and other high-volume elective surgical pathways. New Victoria operates as a high-volume elective site focused on insured and self-pay patients, particularly in orthopaedics and other routine surgical pathways, with investment priorities including capacity and equipment for high-volume elective procedures per Bupa CEO Philip Luce's description to Investors in Healthcare. The South West London submarket benefits from the intersection of South West London's affluent residential population generating the highest private health insurance take-up rates of any London borough cluster and the acute NHS waiting list pressure in the region where GP referral to NHS treatment timelines are driving insured and self-pay patients to seek private elective procedures at independent hospitals including New Victoria. The submarket's combination of accessible suburban locations, existing private hospital campuses, and catchment populations with high private insurance penetration creates the demand foundation for both hospital campus real estate investment and new outpatient hub medical office building development in the primary healthcare access gaps between existing hospital sites.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from verified company announcements, Bupa press releases, Savills healthcare research, and verified trade press.