By Geography · By Asset Type · By Brand House · By Retail Format

96 new luxury boutiques opened on Europe's main shopping streets in 2025, a 13% increase year-on-year with vacancy near zero on the most famous high streets, as LVMH, Kering, and Richemont accounted for nearly a third of all openings, luxury street rents grew 3.6% in 2024 and are now 3% above 2018 levels, LVMH's Bernard Arnault transformed La Samaritaine near the Louvre into a retail and hospitality destination by acquiring the building outright, and Prada Group's Miu Miu posted a 49% retail sales surge in H1 2025 confirming that the luxury brands successfully targeting Gen Z and Millennials are delivering the growth that compensates for the slowdown in China.

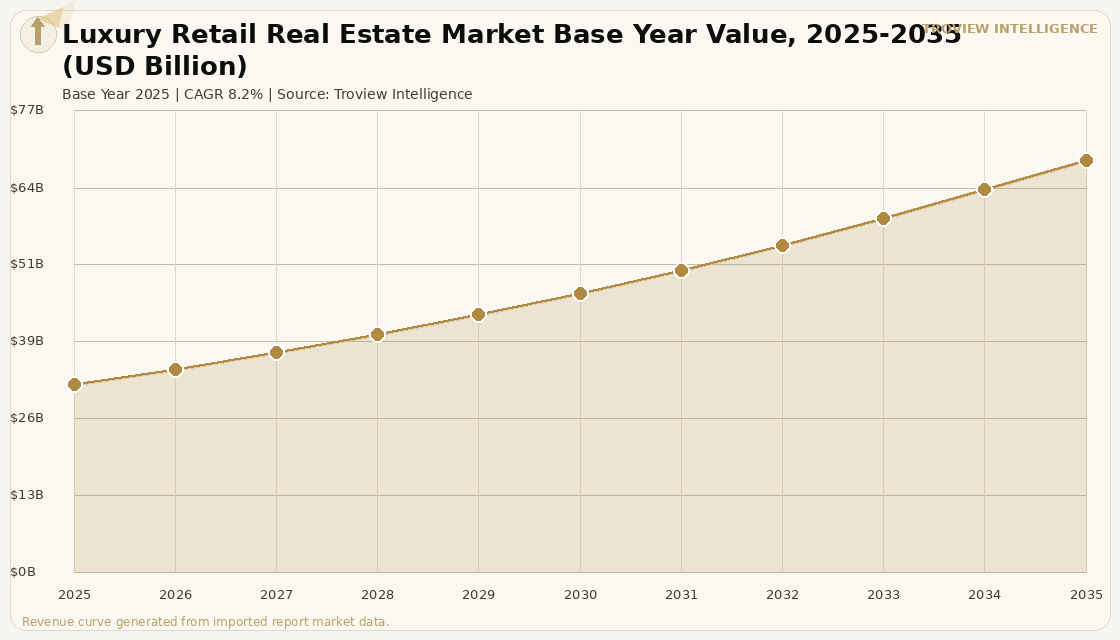

MARKET SYNOPSIS

The global luxury retail real estate market size was USD 31.46 Billion in 2025 and is expected to register a revenue CAGR of 8.2% during the forecast period, reaching USD 68.86 Billion by 2035. The global luxury retail real estate market encompasses the rental and operational revenues generated by dedicated luxury retail corridors, standalone brand flagship buildings, luxury-focused department stores, and the premium retail precincts within five-star hotels and resort developments that serve the ultra-high-net-worth and aspirational luxury consumer base. 96 new luxury boutiques opened on Europe's main shopping streets in 2025, a 13% increase year-on-year, with LVMH, Kering, and Richemont accounting for nearly a third of all new openings per Luxury Tribune reporting, while the vacancy rate is near zero on the most famous high streets and competition between luxury houses intensified against a backdrop of rising rents and a scarcity of premium locations. Luxury high street rents across Europe's 20 key luxury streets grew 3.6% in 2024 and are now 3% higher on average than in 2018 per industry data, with 17 of 20 key streets having vacancy below 5% and six having no vacancy at all.

The global luxury retail real estate market is being shaped by two concurrent forces: the major luxury conglomerates' strategic acquisition of their flagship real estate removing themselves from the rental market entirely in their most important locations and the opening of new luxury retail infrastructure in emerging markets including India and the Middle East where supply scarcity rather than demand is the primary constraint on growth. LVMH's Bernard Arnault acquired and transformed La Samaritaine in Paris near the Louvre into a retail and hospitality destination, a landmark transaction demonstrating the willingness of luxury houses to pay permanent real estate ownership premiums to secure prestigious locations forever. Rents on New York's upper Fifth Avenue, which peaked at USD 3,500 per square foot in 2015, have stabilised around USD 2,000 per square foot, representing a durable institutional leasing market that luxury brands maintain despite the per-unit cost. Prada Group's Miu Miu posted a 49% retail sales surge in H1 2025 and Tapestry's Coach brand achieved 14% sales growth in fiscal Q4 2025 with Gen Z and Millennials comprising 60 to 70% of new North American customers per luxury retail industry analysis, confirming that the brands successfully repositioning toward younger demographics are generating the performance that justifies continued physical luxury real estate investment. For instance, in November 2025, Galeries Lafayette, France, opened its first India flagship in Mumbai's historic Fort area, a five-floor 90,000 square foot store housing over 250 luxury and designer brands in partnership with Aditya Birla Fashion and Retail Limited, with Galeries Lafayette Group's executive chairman Nicolas Houzé describing the launch as a defining moment in the company's international journey, per Reuters reporting of November 2025. These are some of the key factors driving revenue growth of the market.

However, the global luxury retail real estate market faces structural constraints. In the first half of 2025, many leading luxury conglomerates including LVMH and Kering reported declining revenues amid challenging market conditions, with slowing Chinese consumer demand which has been the primary driver of global luxury growth for over a decade and US tariff uncertainty creating near-term headwinds per luxury brand investor disclosures. US tariffs on European luxury goods represent a direct cost increase for brands whose manufacturing is concentrated in France, Italy, and Switzerland and whose largest revenue market is North America. The luxury retail real estate market in emerging markets including India faces a structural constraint not of demand but of supply, with India having only three genuine luxury malls and more than a dozen brands ready to enter the market if space became available per DLF's luxury mall management team. The high construction and fit-out standards required for luxury retail real estate custom architectural finishes, specialist lighting, climate control, high-specification security systems mean that luxury-designated buildings carry construction costs 40 to 60% above standard commercial retail. These factors substantially limit global luxury retail real estate market growth over the forecast period.

Luxury retail real estate is the one segment where the tenant's brand equity matters more than the landlord's building quality. In a conventional retail lease, the landlord holds the asset and the tenant rents the shop. In luxury retail on Rue du Faubourg Saint-Honoré or Bond Street, the luxury house is frequently the real estate owner, investing hundreds of millions to transform a historic building into a brand temple. Bernard Arnault's La Samaritaine is the purest expression of this logic: a permanent acquisition of irreplaceable real estate to ensure that Louis Vuitton, Chanel, and Dior never have to negotiate their Paris lease with a third-party landlord again. The investment thesis for luxury retail real estate is not just about rent income. It is about the scarcity of locations that carry the address premium that a luxury brand requires to reinforce its global positioning." Troview Intelligence Head of Global Luxury Retail Real Estate Research

SEGMENT INSIGHTS

By Geography

Europe and Asia Pacific are expected to account for a significantly large revenue share in the global luxury retail real estate market during the forecast period.

Based on geography, the global luxury retail real estate market is segmented into Europe, Asia Pacific, North America, and Middle East and Africa. Europe dominates by luxury real estate investment intensity and per-square-metre rent, with the Champs-Élysées in Paris, Via Montenapoleone in Milan, New Bond Street in London, and Bahnhofstrasse in Zurich commanding the highest rents per square foot in global luxury retail. Asia Pacific is expected to register the fastest revenue CAGR over the forecast period, driven by Japan's sustained luxury spending amplified by yen depreciation where LVMH cited a 32% performance increase in Q1 2024 due to weak yen and tourist inflows, India's emerging luxury mall infrastructure where supply scarcity constrains brand entry, and Southeast Asia's growing luxury consumer base. North America's market has stabilised from its post-pandemic surge, with New York's Fifth Avenue at approximately USD 2,000 per square foot representing a durable benchmark. The Middle East's luxury retail real estate market, anchored by Dubai Mall's Fashion Avenue and Mall of the Emirates, is experiencing the fastest rent growth at 14.9% year-on-year per UAE prime retail market data.

By Asset Type

Standalone luxury brand flagship buildings are expected to account for a significantly large revenue share in the global luxury retail real estate market during the forecast period.

Based on asset type, the global luxury retail real estate market is segmented into standalone brand flagship buildings, dedicated luxury retail precincts within mixed-use developments, luxury-focused department stores, hotel and resort boutique retail, and luxury high street ground floor units. Standalone brand flagship buildings dominate investment value per square metre, as luxury houses increasingly acquire rather than lease their most strategically important locations, with LVMH, Chanel, and Kering acquiring buildings on Avenue de Montaigne, around Place Vendôme, and on the Champs-Élysées in Paris per market analysis. Dedicated luxury retail precincts within mixed-use developments Dubai Mall's Fashion Avenue, Jio World Plaza in Mumbai's BKC, and GINZA SIX in Tokyo are the fastest-growing segment by new supply delivery, as developers in emerging luxury markets build purpose-designed luxury environments that provide the tenant mix, footfall, and security environment that global luxury brands require.

By Brand House and Tenant

LVMH, Kering, and Richemont are expected to account for a significantly large revenue share of luxury retail real estate leasing globally during the forecast period.

Based on brand house and tenant, the global luxury retail real estate market is dominated by the three major luxury conglomerates. LVMH led European luxury store openings with 15 new locations in 2024, with LVMH, Richemont, and Kering collectively accounting for more than a third of all new European luxury store openings per industry data. LVMH is also responding to US tariff pressures by expanding local US production, with a second Louis Vuitton facility in Texas announced to reduce import costs per LVMH company announcements. The jewellery and watches segment a sub-category where Richemont's Cartier, Van Cleef & Arpels, and IWC brands excel opened 26 stores across Europe in 2024, up from 21 in 2023, as hard luxury continues to grow as a consumer preference independent of broader soft luxury fashion headwinds.

REGIONAL ANALYSIS

EUROPE HIGHEST

| New Boutiques 2025 | 96 on Europe's main luxury streets (+13% YoY) | Street Rent Growth | 3.6% in 2024; 3% above 2018 average |

| Vacancy | 17 of 20 key luxury streets below 5%; 6 at zero vacancy | Flagship Strategy | LVMH acquiring Paris landmarks outright to secure locations permanently |

Europe is the global benchmark for luxury retail real estate, with near-zero vacancy on the most prestigious high streets, 96 new boutique openings in 2025, and luxury street rents 3% above their 2018 pre-pandemic levels despite the broader luxury market's transition phase. Paris, Milan, and London account for the majority of new luxury investment, and brands are exploring adjacent streets when primary high streets have no availability, testing secondary luxury corridors as an escape valve for demand that cannot be accommodated on the most constrained primary streets. The strategic acquisition of flagship real estate by luxury houses LVMH acquiring buildings on Avenue de Montaigne, Chanel securing Place Vendôme locations, and Bernard Arnault's La Samaritaine transformation is permanently removing prime Paris luxury buildings from the third-party leasing market, concentrating the available leasing pool into a smaller addressable stock.

ASIA PACIFIC

| Japan LVMH H1 2024 | +32% performance from yen depreciation and tourist inflows | India Luxury Market | USD 12.1 billion (valued), ranks 4th globally in USD 100M+ wealth holders |

| India True Luxury Malls | Only 3 nationwide (DLF Emporio, DLF Chanakya, Jio World Plaza) | Galeries Lafayette India | First India flagship: Mumbai Fort, Nov 2025, 90,000 sq ft, 250+ brands |

Asia Pacific is the fastest-growing luxury retail real estate region, driven by India's constrained luxury mall supply, Japan's yen-amplified spending surge, and the continued expansion of luxury infrastructure in Singapore, Hong Kong, and Southeast Asian gateway cities. Japan's luxury retail market saw exceptional spending by inbound tourists benefiting from yen weakness, with LVMH citing a 32% performance improvement attributed to the combination in Q1 2024 investor updates. India's luxury retail real estate market is characterised by extreme demand-supply imbalance: India ranks fourth globally in individuals with net assets exceeding USD 100 million, yet has only three genuine luxury malls in the entire country. In November 2025, Galeries Lafayette opened its first India flagship in Mumbai's Fort area, a five-floor 90,000 square foot space housing over 250 luxury and designer brands in partnership with Aditya Birla Fashion and Retail.

NORTH AMERICA AND MIDDLE EAST STABLE

| New York Fifth Avenue | ~USD 2,000/sq ft/year (stabilised from USD 3,500 peak in 2015) | UAE Super-Regional Luxury | 14.9% rent growth YoY to AED 350-450/sq ft annually |

| Gen Z and Millennial Growth | Coach +14% FY Q4 2025, Miu Miu +49% H1 2025 | US Tariff Risk | LVMH expanding Texas manufacturing to reduce import costs |

North America's luxury retail real estate market is characterised by rental stabilisation on Fifth Avenue at approximately USD 2,000 per square foot, representing a durable institutional leasing market that brands maintain as a flagship investment despite the per-unit cost being half the 2015 peak. The US market faces near-term headwinds from tariff uncertainty, with Kering identifying proposed tariff increases as a potential profit margin risk, while LVMH is responding by expanding domestic US manufacturing. The Middle East's luxury retail real estate market, anchored by Dubai Mall's Fashion Avenue and the Mall of the Emirates' luxury concourse, is recording the fastest luxury rent growth of any major market, with UAE super-regional prime rents rising 14.9% year-on-year. The brands benefiting most in North America are those successfully targeting Gen Z and Millennials Miu Miu's 49% H1 2025 retail sales surge and Coach's 14% growth confirming that the youth demographic shift is creating genuine growth despite the broader conglomerate headwinds.