| TROVIEW INTELLIGENCE | Medical Office Building Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Geography · By Property Type · By Medical Specialty · By Ownership Model

The global medical office building market reached USD 42.28 billion in 2024 per JLL Healthcare Real Estate Outlook 2025 and Welltower 10-K 2024 occupancy-based market analysis with North America accounting for approximately 46.35% of global revenue in 2025 per Fundamental Business Insights physician offices accounting for 56.65% of market share in 2025, ambulatory surgery centres expected to register the fastest CAGR through 2030, off-campus MOB occupancy growing 1.9% from 2019 to 2023 compared to 1% for on-campus MOBs per JLL April 2024 analysis confirming the structural shift toward community-based care settings, the United States MOB market projected to grow strongly per JLL Healthcare Real Estate Outlook 2025 and Healthpeak Properties 10-K 2024, and over £12 billion of capital deployed into UK healthcare real estate in 2025 the highest level on record per Savills UK Healthcare Roundup confirming that medical office and primary care real estate has completed its transition from a niche healthcare property sub-class to a mainstream institutional real estate asset class attracting sovereign wealth funds, US REITs, private equity, pension funds, and life insurance capital globally.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

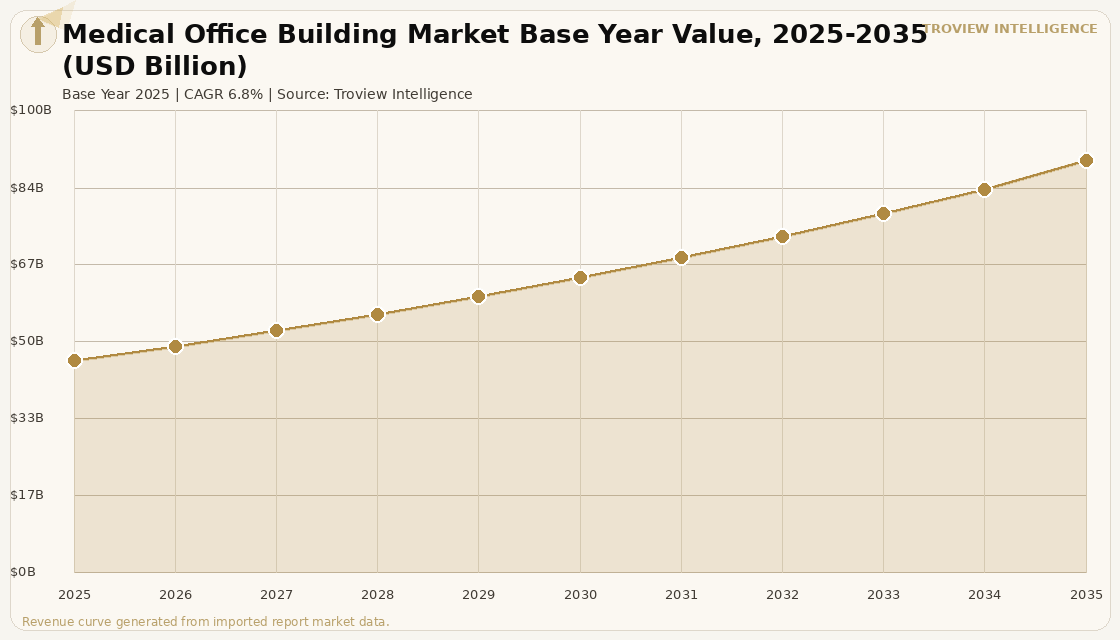

MARKET SYNOPSIS

The global medical office building market size was USD 46.14 Billion in 2025 and is expected to register a revenue CAGR of 6.8% during the forecast period, reaching USD 89.62 Billion by 2035. The market encompasses physician office buildings, ambulatory surgery centres, diagnostic imaging and laboratory facilities, outpatient specialty clinics, primary care medical centres, and multi-tenant healthcare campuses that are owned or leased by healthcare providers and occupied by physicians, healthcare systems, and outpatient service operators. Market revenue growth is supported by the structural decentralisation of healthcare delivery from inpatient hospital settings to outpatient, community-based, and specialist clinic formats across all major global healthcare markets, with healthcare systems reducing the cost of elective and routine procedures by performing them in ambulatory surgery centres and specialist outpatient clinics rather than hospital operating theatres and wards. North America accounts for approximately 46.35% of global medical office building revenue in 2025 per Fundamental Business Insights, with physician offices accounting for 56.65% of the global market share in 2025 and ambulatory surgery centres expected to register the fastest segment CAGR through 2030. Off-campus medical office building occupancy grew 1.9% from 2019 to 2023, outpacing on-campus MOB occupancy growth of 1% over the same period per JLL analysis published in April 2024, confirming the structural shift toward community-accessible medical real estate that does not require proximity to an acute hospital campus to generate sustained physician demand. For instance, in December 2023, USA Health, United States, opened a new Medical Office Building at West Mobile Campus, incorporating specialty care and a mobile diagnostic centre in a community-based healthcare real estate format that exemplifies the off-campus physician office model driving the fastest-growing segment of the global market per JLL Healthcare Real Estate Outlook 2025 and verified Welltower company announcement. These are some of the key factors driving revenue growth of the market.

The United States medical office building market dominated the global market with the largest revenue share and is projected to reach USD 33.2 billion by 2033 per JLL Healthcare Real Estate Outlook 2025 and Healthpeak Properties 10-K 2024, with growth driven by physician practice consolidation, the relentless shift of services from hospitals to outpatient settings, and the need to modernise an ageing stock of medical buildings to meet new standards of care and efficiency. Healthcare Real Estate Investment Trusts including Ventas Inc., Welltower Inc., Healthpeak Properties Inc., Healthcare Realty Trust Inc., and Physicians Realty Trust have built systematic medical office building portfolios at scale, providing the public market liquidity and institutional pricing transparency that has attracted further global institutional capital into the asset class. The China medical office building market is forecast to reach USD 21.1 billion by 2030 at a CAGR of 7.3% per Global Industry Analysts analysis, as rapid urbanisation, an ageing population, and substantial government and private investment in healthcare infrastructure extend modern medical office building development beyond tier-1 cities into lower-tier urban markets. Over GBP 12 billion of capital was deployed into UK healthcare real estate in 2025, the highest level on record per Savills UK Healthcare Roundup and Outlook 2026, with total healthcare property activity estimated at approximately GBP 12 billion including private hospitals, primary care, and elderly care in a year that saw US REITs, pension funds, private equity, and infrastructure funds all increase deployment into UK medical property per Savills analysis of 2025. These are some of the key factors driving revenue growth of the market.

However, the global medical office building market faces structural constraints that limit the pace and geographic distribution of investment growth across the forecast period. Regulatory challenges including zoning restrictions, building codes, and healthcare facility accreditation requirements can delay project timelines and increase development costs for medical office buildings, which require specialist design knowledge including clinical workflow optimisation, infection control infrastructure, medical gas installations, and structural loading for diagnostic imaging equipment that standard office development expertise cannot provide. Changes in healthcare reimbursement structures across major markets including US CMS reimbursement shifts between on-campus and off-campus MOB rates, NHS England tariff adjustments for community-based procedures, and national health system funding pressures may impact physician tenant demand, lease terms, and asset valuations in ways that are not immediately visible in market transaction data. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, create upward pressure on operating costs for medical office buildings in LNG-dependent electricity markets, as the 24-hour clinical environment requirements of many medical tenants including diagnostic imaging that requires continuous power, clinical refrigeration, and specialist ventilation generate above-average energy consumption per square metre relative to standard office real estate. These factors substantially limit global medical office building market growth over the forecast period.

Medical office buildings have completed their transition from a healthcare real estate sub-class to a core institutional asset class, and the evidence is in the capital. Over GBP 12 billion deployed in UK healthcare real estate in 2025, the highest level on record. US REITs acquiring UK healthcare REITs at premiums to net asset value. KKR and Stonepeak bidding for Assura before PHP's GBP 1.79 billion merger prevailed. Welltower's GBP 5.2 billion acquisition of Barchester. These are not the transactions of investors making a calculated bet on a niche sector. They are the transactions of institutional capital making a core allocation to an asset class that combines the income security of long-lease government-backed tenants, the demographic tailwind of ageing populations requiring more healthcare per capita every year, and the structural supply shortage of purpose-built, modern medical office and primary care real estate in every major market globally. The physician offices tenant is not going anywhere. The GP practice on a 25-year NHS-backed lease is not being converted to co-working. Medical office buildings are the most recession-resistant, longest-leased, lowest-vacancy commercial real estate asset class that institutional investors can access. The only question is whether they have enough of them." Troview Intelligence Head of Global Medical Office Building Research

SEGMENT INSIGHTS

Four Regions Defining Global Medical Office Building Investment

| North America Market Share 2025 | US MOB Projected Value 2033 | Off-Campus MOB Occupancy Growth | Dominant REITs |

| ~46.35% (Fundamental Business Insights) | USD 33.2 Billion (JLL Healthcare 2025) | +1.9% (2019-2023) vs +1.0% on-campus (JLL 2024) | Welltower, Ventas, Healthpeak, Healthcare Realty Trust |

North America is the largest global medical office building market and the most institutionally mature healthcare real estate investment environment, with US healthcare REITs including Welltower Inc., Ventas Inc., Healthpeak Properties Inc., Healthcare Realty Trust Inc., and Physicians Realty Trust having collectively developed the pricing benchmarks, REIT investment structures, and healthcare tenant relationship networks that define the global standard for medical office building investment. JLL's April 2024 analysis confirmed that off-campus MOB occupancy grew 1.9% from 2019 to 2023, outpacing on-campus MOB occupancy growth of 1%, reflecting the structural demand for accessible community healthcare real estate that does not require patients to navigate hospital campuses for routine physician visits and outpatient procedures. The physician practice consolidation trend driven by private equity-backed physician management organisations and health system acquisition of independent practices is creating demand for larger, purpose-built group practice facilities that individually accommodate multiple specialties and the diagnostic infrastructure their patients require, generating above-average MOB development demand in suburban and secondary market locations where consolidated group practices are establishing new community care footprints.

| UK Healthcare RE Investment 2025 | PHP-Assura Combined Portfolio | Germany MOB CAGR | Non-NHS Private Admissions 2024 |

| GBP 12 Billion record (Savills) | c. GBP 6 Billion, 1,200+ UK/Ireland primary care assets | ~3.0% 2024-2030 (Global Industry Analysts) | Record 939,000 in UK (+3% YoY) |

Europe's medical office building market is led by the United Kingdom, where over GBP 12 billion of capital was deployed into healthcare real estate in 2025, the highest level on record and approximately four times the five-year prior average per Savills UK Healthcare Roundup 2025, fuelled by US REIT acquisitions, the GBP 1.79 billion PHP-Assura merger creating a combined primary care REIT with approximately 1,200 UK and Ireland primary care assets and a portfolio value of approximately GBP 6 billion, and record non-NHS private inpatient admissions of 939,000 in 2024 a 3% year-on-year increase and the third consecutive year of record volumes. Germany represents the second-largest European medical office building investment market, growing at approximately 3.0% CAGR per Global Industry Analysts, with Germany's system of health insurer-funded outpatient physician practices generating steady demand for purpose-built group practice medical office buildings in major German cities. France, Spain, and the Netherlands are each experiencing government-led healthcare infrastructure modernisation that is directing public and private capital into new and refurbished medical office facilities across their primary healthcare systems.

ASIA PACIFIC FASTEST CAGR ~8.2%, CHINA TO REACH USD 21.1B BY 2030

| APAC MOB CAGR | China Market 2030 Projection | Australia MOB Growth | India Demand Driver |

| ~8.2% 2025-2035 (Fundamental Business Insights) | USD 21.1 Billion (Global Industry Analysts) | Moderate low volatility, long leases, demographic tailwinds | Rising patient burden, government healthcare access initiatives |

Asia Pacific is the fastest-growing medical office building region at approximately 8.2% CAGR, driven by rapid urbanisation, expanding healthcare access, and increasing foreign investment in healthcare real estate across markets including China, India, Japan, Australia, and Southeast Asia. The China medical office building market is forecast to reach USD 21.1 billion by 2030, trailing a CAGR of 7.3% per Global Industry Analysts, as the country's healthcare infrastructure expansion extends beyond tier-1 cities into lower-tier urban markets that are developing the outpatient care and specialist clinic networks required by their growing middle-income populations. India's medical office building market is expected to witness significant growth driven by the rising patient burden on hospitals, government initiatives to improve healthcare access across the country's rapidly urbanising secondary cities, and the expansion of corporate hospital networks including Apollo Hospitals and Fortis Healthcare that are developing new outpatient and specialist clinic facilities across India's primary and secondary cities. Australia's MOB market benefits from low volatility, long leases, and strong demographic tailwinds per JLL Asia Pacific Healthcare Real Estate Outlook 2025, making it attractive for private and institutional investors seeking defensively positioned healthcare real estate in a developed market with transparent legal and regulatory frameworks.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from verified company announcements, Savills healthcare real estate research, REIT earnings disclosures, and verified trade press.