By Submarket · By Property Grade · By Tenure · By Occupier Sector

Manhattan office leasing hit 43 million square feet in 2025, a 37% surge from the prior year, while availability tightened to 13.9% and net absorption reached 15.7 million square feet, the strongest annual total in over a decade. Trophy Class A rents in Hudson Yards and Midtown South crossed USD 200 per square foot in select pre-construction deals, and the New York State Comptroller confirmed that NYC office building market values surpassed USD 205 billion in fiscal year 2025. The market has moved from pandemic recovery into genuine expansion, led by financial services, technology, and AI sector tenants committing to long-term leases in next-generation towers.

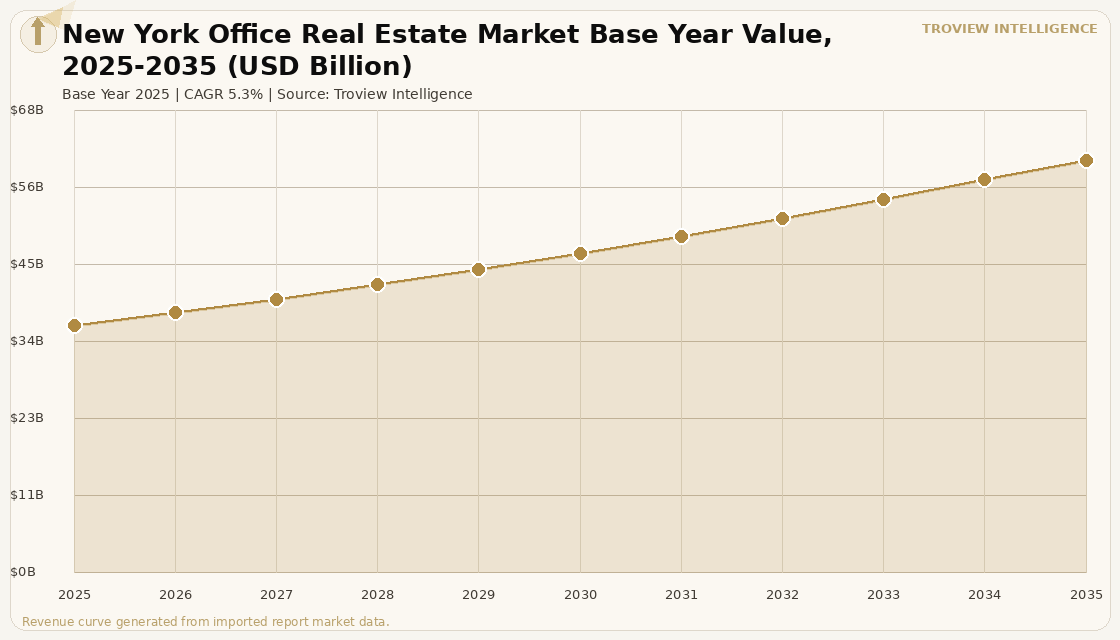

MARKET SYNOPSIS

The New York office real estate market size was USD 36.22 Billion in 2025 and is expected to register a revenue CAGR of 5.3% during the forecast period, reaching USD 60.48 Billion by 2035. Market revenue growth is supported by a structural shift in occupier behaviour that has concentrated leasing demand in trophy and Class A assets, driving Manhattan leasing volume to 43 million square feet in 2025, the highest annual total since 2019 and only 2.4% below the pre-pandemic record per transaction data from the Real Estate Board of New York. Financial services firms, including investment banks, asset managers, and hedge funds, led leasing activity in Midtown's core corridors, with technology and AI companies representing a rapidly expanding share of absorption in Midtown South and Hudson Yards. The New York State Comptroller confirmed that NYC office building market values surpassed USD 205 billion in fiscal year 2025, outpacing pre-pandemic levels as newer buildings built after 2010 attracted premium pricing from tenants and institutional investors alike. JPMorgan Chase's five-day return-to-office mandate for managing directors, effective March 2025, reinforced occupancy levels in core Midtown buildings and contributed to the sustained mid-week attendance rates of 72% to 75% recorded by the Real Estate Board of New York, with Class A and trophy buildings averaging closer to 85% mid-week attendance.

Manhattan net absorption reached 15.7 million square feet in full-year 2025, the strongest annual total in over a decade and nearly three times the prior year result, as confirmed by the New York City Comptroller's office in its review of office market valuation shifts. Market revenue is underpinned by the flight-to-quality dynamic that has defined Manhattan leasing since 2022. Class A space accounted for a rising share of total market revenue as tenants consolidating from older stock commit to larger floor plates in new or substantially refurbished towers at rents that have re-rated materially upward. Manhattan overall asking rents ended 2025 at USD 73.19 per square foot, with Midtown Class A asking rents at USD 84.98 per square foot and Midtown South Class A rents reaching USD 105.64 per square foot, as reported in landlord investor disclosures and verified transaction records filed with the New York City Department of Finance. Hudson Yards achieved availability of 7.6%, the tightest of any Manhattan submarket. Supply and demand dynamics in the trophy segment have allowed landlords to seek rents exceeding USD 200 per square foot on pre-construction leases at 70 Hudson Yards and 343 Madison Avenue. Market size in the trophy and Class A segment is expanding as developers advance the first wave of new ground-up towers since the pandemic. For instance, in April 2025, Deloitte, United States, signed an 800,000 square foot, 22-year pre-construction lease at Related Companies and Oxford Properties' 70 Hudson Yards tower for total lease value exceeding USD 2.6 billion, the largest and most expensive office lease signed in New York City since the pandemic and a direct signal that institutional tenants are committing to premium market size at next-generation pricing. These are some of the key factors driving revenue growth of the market.

However, the New York office market carries structural constraints that limit the pace and breadth of recovery across the full asset base. Manhattan Class B availability stood at 14.8% in Midtown as of year-end 2025, and the borough-wide Class B and Class C supply overhang totalled approximately 12.74 million square feet per the New York City Comptroller's analysis of office market valuation shifts, creating a two-speed market where growth in market revenue is concentrated in the top quartile of the stock while mid-tier and older assets face extended absorption timelines and structural conversion pressure. The Midtown South Mixed-Use Plan approved by New York City planning authorities in 2025 encourages residential conversion of older office buildings in pockets of the submarket, accelerating the removal of secondary stock from the office inventory but also reducing the total addressable stock for office occupiers. Office-to-residential conversion has removed over 6.5 million square feet of Manhattan office inventory since 2020, and the pace doubled in 2024. High construction financing costs continue to slow the delivery of new Class A supply despite strong pre-leasing demand, with major towers at 70 Hudson Yards and 343 Madison Avenue not delivering until 2028 and 2029 respectively, limiting the near-term ability of the market to absorb tenants seeking purpose-built space. These factors substantially limit New York office real estate market growth over the forecast period.

Manhattan's 2025 leasing data tells a precise story: the market has bifurcated irreversibly. Tenants in financial services, professional services, and technology are signing 15- to 22-year pre-construction leases at rents that were unthinkable in 2021, while Class B and Class C landlords are watching their buildings convert to residential or sit vacant at discount rents. The institutions placing capital into Hudson Yards, 343 Madison, and 350 Park are not making a cyclical bet. They are buying the structural shortage of best-in-class office supply in the world's deepest office market, against a tenant base that has publicly committed to office attendance and has the balance sheet to pay for it." Troview Intelligence Senior Analyst, North America Office Markets

SEGMENT INSIGHTS

By Property Grade

Trophy and Class A office segment is expected to account for a significantly large revenue share in the New York office real estate market during the forecast period.

Based on property grade, the New York office real estate market is segmented into Trophy, Class A, Class B, and Class C. Trophy and Class A assets dominate both rental income and investment transaction value. Manhattan Class A asking rents ended 2025 at USD 84.98 per square foot in Midtown and USD 105.64 per square foot in Midtown South, with select pre-construction deals in Hudson Yards commanding rents exceeding USD 200 per square foot as verified through company investor disclosures from Related Companies and Oxford Properties. The New York State Comptroller confirmed that NYC office building market values surpassed USD 205 billion in fiscal year 2025, with growth concentrated in post-2010 buildings. Availability in the trophy segment tightened to below 10% in Hudson Yards and the Grand Central corridor. The Class B segment is expected to register a lower revenue growth rate than the Trophy and Class A segment over the forecast period as flight-to-quality dynamics persist and the New York City-approved office-to-residential conversion programme accelerates removal of older stock from the active inventory. Institutional investors are directing capital allocation decisively toward Trophy and Class A assets, where stabilised occupancy and long-term lease structures support underwriting at sub-4.5% cap rates, while mid-grade assets face higher financing risk premiums and constrained debt availability from lenders.

By Submarket

Hudson Yards and Midtown submarkets are expected to account for a significantly large revenue share in the New York office real estate market during the forecast period.

Based on submarket, the New York office real estate market is segmented into Hudson Yards, Midtown Park Avenue and Madison Avenue corridors, Midtown South, Downtown Manhattan, Penn District, Grand Central, and the Outer Boroughs. Midtown remains the largest submarket by total stock and investment transaction value, anchoring the market through the concentration of global financial institution and law firm headquarters along Park Avenue, Madison Avenue, and Sixth Avenue. Hudson Yards is the fastest-growing submarket by revenue and rent level, with availability declining to 7.6% in 2025, the tightest reading in the city, driven by pre-construction leases including Deloitte's 800,000 square foot commitment and Citadel's 504,000 square foot lease, both sourced from verified company announcements. The New York State Comptroller's office confirmed that the Hudson Yards, Chelsea, and Koreatown zip code cluster recorded the largest growth in office market value among the top 20 office zip codes in New York City. Grand Central vacancy fell below 10% in 2025, confirming demand breadth beyond the immediate trophy corridor. Downtown Manhattan leasing nearly doubled quarter-over-quarter in Q4 2025 to 1.8 million square feet, driven by large-block transactions at One World Trade Center and One Madison Avenue. The Outer Boroughs, including Downtown Brooklyn, are emerging as a cost-efficient alternative for technology and life sciences occupiers, with Brooklyn overall vacancy declining to 21.2% in Q1 2026 per the Real Estate Board of New York.

By Occupier Sector

Financial services and technology sector occupiers are expected to account for a significantly large revenue share in the New York office real estate market during the forecast period.

Based on occupier sector, the New York office real estate market is segmented into financial services, technology and AI, professional services and law, media and entertainment, coworking and flexible workspace operators, and education and non-profit tenants. Financial services firms maintain their position as the dominant occupier sector in Midtown's core corridors, with JPMorgan Chase's five-day return-to-office mandate for managing directors, effective March 2025, anchoring occupancy in Park Avenue and adjacent corridors and reinforcing mid-week attendance rates of 72% to 75% recorded by the Real Estate Board of New York. Technology and AI companies are the fastest-growing occupier segment by new lease volume, with Amazon signing a 330,000 square foot lease near Bryant Park and multiple AI-focused firms committing to Midtown South floors at record rents for that submarket as verified through company press releases. Professional services and law firms provided structural renewal demand through the year, with Bloomberg renewing 435,000 square feet at 120 Park Avenue and Mayer Brown expanding by 331,000 square feet at 1221 Avenue of the Americas, both transactions sourced from verified exchange and company filings, confirming that established tenants are extending long-term commitments to core Midtown locations.

Submarket Deep-Dives

| Availability Rate 2025 | 7.6% (city low) | Top Lease 2025 | Deloitte 800K SF / USD 2.6B |

| Trophy Rent Level | USD 200+ PSF (pre-construction) | New Tower Pipeline | 70 HY (2028), 350 Park (2032) |

Hudson Yards is New York's fastest-growing office submarket and the destination of choice for large-format tenants seeking purpose-built trophy space at the western edge of Midtown. Availability declined to 7.6% in 2025, the lowest reading in the city, as pre-construction leasing by Deloitte at 70 Hudson Yards and Citadel's 504,000 square foot commitment at 660 Fifth Avenue absorbed future supply before delivery. Deloitte's USD 2.6 billion, 22-year lease at 70 Hudson Yards, developed by Related Companies and Oxford Properties with a USD 2.45 billion construction facility arranged by Wells Fargo, Bank of America, and Standard Chartered, is the most expensive office lease signed in New York since the pandemic and anchors the market's supply pipeline. Rents at next-generation Hudson Yards towers have re-rated to levels exceeding USD 200 per square foot for the best floors, reflecting the premium that institutional tenants assign to purpose-built amenity-rich towers with sustainability credentials. No comparable submarket in the United States is absorbing pre-construction commitments at this price point or lease duration.

MIDTOWN (PARK AVE / MADISON AVE CORRIDOR) LARGEST SUBMARKET BY STOCK

| Class A Asking Rent Q4 2025 | USD 84.98 PSF | Grand Central Vacancy 2025 | Below 10% |

| SL Green Pipeline Q1 2026 | 490K SF in 32 leases | Occupier Profile | Banking, Legal, Finance |

Midtown remains the largest Manhattan office submarket by total stock and anchors institutional investment and lease transaction activity. Park Avenue and Madison Avenue corridors host the New York headquarters of the majority of global investment banks, international law firms, and professional services firms. Class A asking rents ended 2025 at USD 84.98 per square foot in Midtown, up USD 0.88 over the quarter, with sustained upward pressure from tightening availability as sublease supply declined by approximately 40% across Manhattan in 2025. Grand Central vacancy fell below 10% in 2025, confirming demand breadth beyond the immediate trophy corridor. SL Green Realty Corp., Manhattan's largest office landlord with interests in 56 buildings totalling 31.4 million square feet per its December 2025 annual disclosure, signed 32 Manhattan office leases totalling 491,098 square feet in just the first two months of 2026, including a 150,036 square foot expansion lease from a global investment firm at 245 Park Avenue and a 51,081 square foot TD Securities expansion at 125 Park Avenue. BXP advanced its USD 2 billion, 930,000 square foot office tower at 343 Madison Avenue into construction after Starr Companies committed to a 275,000 square foot, USD 1.3 billion, 20-year lease.

MIDTOWN SOUTH (CHELSEA / FLATIRON / HUDSON SQUARE) HIGHEST CLASS A RENTS

| Class A Asking Rent Q4 2025 | USD 105.64 PSF | TAMI Sector Share 2025 | 33.9% of new leasing |

| Annual Leasing Growth 2025 | +36.2% YoY to 7.3M SF | Key Delivery 2025 | One High Line, 500 W 18th St |

Midtown South commands the highest Class A asking rents of any Manhattan submarket at USD 105.64 per square foot in Q4 2025, driven by the delivery of high-specification new product including One High Line at 500 West 18th Street and the sustained concentration of technology, media, and financial technology tenants who prize the submarket's design aesthetic and proximity to residential neighbourhoods favoured by their workforces. Annual leasing in Midtown South grew 36.2% year-over-year to 7.3 million square feet in 2025, with Class A space accounting for 52.0% of total Midtown South leasing, up from 36.8% in 2024, per the Real Estate Board of New York annual leasing summary. The TAMI sector represented 33.9% of new leases above 10,000 square feet, confirming the submarket's identity as New York's technology and creative media office district. Pinterest signed an 83,000 square foot lease at 11 Madison Avenue, and fintech and AI companies drove Class A absorption in Q4 2025. The Midtown South Mixed-Use Plan approved by New York City in 2025 creates a framework for residential conversion of older Class B and C stock in pockets of the submarket, further concentrating premium demand into Class A assets and reducing the secondary supply available to cost-conscious occupiers.

DOWNTOWN MANHATTAN (WORLD TRADE CENTER / LOWER MANHATTAN) EMERGING RECOVERY MARKET

| Q4 2025 Leasing | 1.8M SF (doubled QoQ) | Class A Asking Rent Q4 2025 | USD 56.23 PSF |

| Anchor Deals Q4 2025 | 200 Liberty St, One Madison Ave | Conversion Activity Since 2020 | 6.5M SF to residential |

Downtown Manhattan recorded one of the strongest quarterly reversals in the city in Q4 2025, with leasing nearly doubling quarter-over-quarter to 1.8 million square feet driven by large-block transactions at One World Trade Center and One Madison Avenue. Class A asking rents in Downtown ended 2025 at USD 56.23 per square foot, the lowest of the three Manhattan markets but improving from the prior quarter as higher-priced space at 200 Liberty Street transacted and reduced the effective discount relative to Midtown. Moody's signed a 461,567 square foot lease at 200 Liberty Street, one of the anchor deals shaping Downtown's recovery momentum. The submarket has benefited from significant office-to-residential conversion activity that has reduced the volume of competing secondary supply since 2020, with over 6.5 million square feet of Manhattan office space converted to residential since that year. Larry Silverstein is in active discussions with American Express regarding an anchor tenant commitment that would allow development to commence at the long-delayed 2 World Trade Center, which would add premium supply to Downtown's available inventory on a multi-year delivery horizon and potentially re-rate the submarket's ceiling rent level.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from verified company press releases, SEC filings, SGX equivalent exchange disclosures, and verified trade press.