| TROVIEW INTELLIGENCE | Submarine Cable Landing Station Real Estate Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Geography · By Cable Type · By Ownership Model · By End-User Sector

TeleGeography's 2025 Submarine Cable Map recorded 597 active or under-construction cable systems and 1,712 landing points globally a build map that investment in new subsea cable projects is expected to reach approximately USD 13 billion between 2025 and 2027, nearly double the amount invested between 2022 and 2024 per TeleGeography reporting of December 2025, as hyperscalers including Amazon Web Services, Google, Meta, and Microsoft displaced traditional telecom consortia as the world's largest private investors in submarine cable infrastructure, Amazon received Cork County Council planning approval in April 2026 for its Fastnet cable landing station the first wholly-owned transatlantic subsea cable for AWS with 320 Tbps capacity connecting Maryland to County Cork and the 2023 to 2025 cable boom added 78 new systems and over 300,000 kilometres of cable, each requiring a landing station real estate asset that serves as the physical interface between submarine cable infrastructure and terrestrial data centre networks.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

MARKET SYNOPSIS

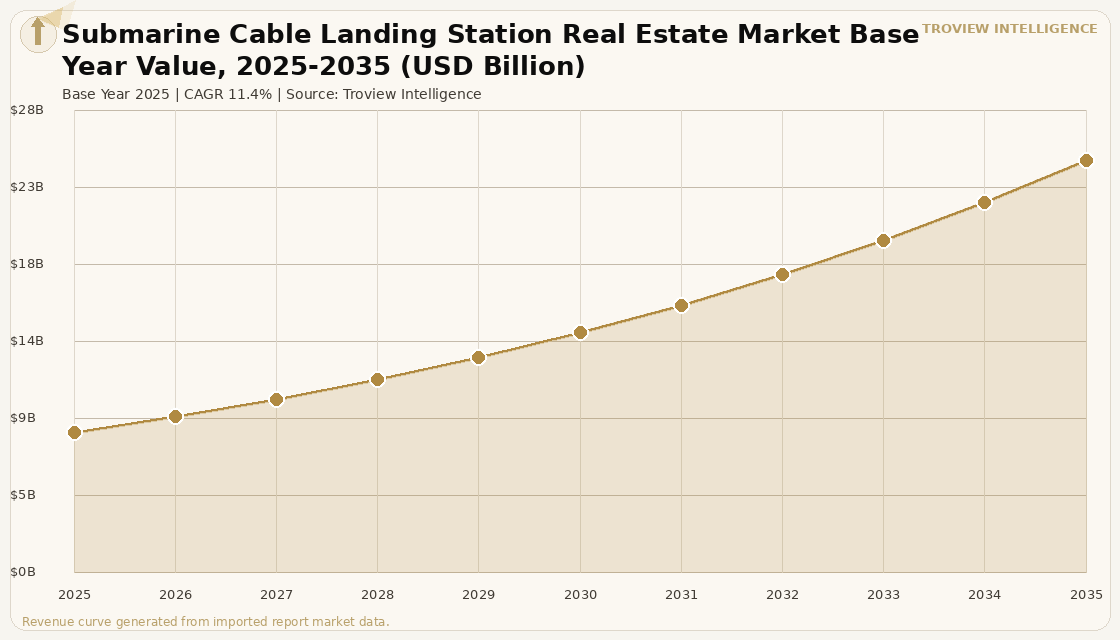

The global submarine cable landing station real estate market size was USD 8.37 Billion in 2025 and is expected to register a revenue CAGR of 11.4% during the forecast period, reaching USD 24.63 Billion by 2035. The market encompasses the real estate, civil infrastructure, terminal station equipment, and associated data centre co-location facilities that constitute cable landing stations the physical interface points where submarine cable systems transition from the marine environment to terrestrial fibre networks. Market revenue growth is supported by an unprecedented acceleration in private hyperscaler investment in submarine cable infrastructure: TeleGeography data published in December 2025 records 597 active or under-construction cable systems with 1,712 landing points globally, with investment in new subsea cable projects expected to reach approximately USD 13 billion between 2025 and 2027, nearly double the USD 6.5 billion invested between 2022 and 2024, as the industry transitions from traditional telecom-consortium ownership models to hyperscaler-dominated private networks that require dedicated, purpose-built landing station real estate adjacent to or co-located with the operator's own data centre campuses. The 2023 to 2025 submarine cable boom added 78 new cable systems and over 300,000 kilometres of deployed cable per Arnet Infrastructure analysis of February 2026, each requiring a minimum of two landing station real estate assets one at each cable terminus creating a structural expansion in the addressable market for cable landing station real estate at a rate proportional to the cable build programme. For instance, in April 2026, Amazon Web Services, United States, received formal planning permission from Cork County Council, Ireland, to construct a cable landing station at Owenahincha, County Cork, serving as the European terminus of the Fastnet transatlantic subsea cable system connecting Maryland, United States, to Ireland with 320 Tbps capacity sufficient to transmit the entire digitised Library of Congress three times per second with the system specifically designed to handle growing AI traffic loads and scheduled for operational service in 2028 per Submarine Networks reporting of April 2026. These are some of the key factors driving revenue growth of the market.

Google, United States, is the world's largest private owner and investor in submarine cable networks, with investment across more than 14 subsea cable systems globally between 2016 and 2025, including the Grace Hopper system linking the US to the UK and Spain, the Nuvem transatlantic system connecting Portugal, Bermuda, and the US announced in 2023, and TalayLink connecting Australia and Thailand announced in November 2024 per verified company announcements and TeleGeography tracking. Meta Platforms, United States, is a co-owner and investor in the Havfrue system also known as the AEC-2 cable, with 108 Tbps design capacity connecting New Jersey to Denmark via Ireland and Norway alongside Aqua Comms, Google, and Bulk Infrastructure, and was planning further transatlantic cable investments with landing implications for Ireland's west coast as of Q1 2025 per Data Center Dynamics reporting. Microsoft Corporation, United States, filed for three Ireland-UK subsea cables in January 2025 and holds co-ownership or major capacity positions on AEC-1, Amitie, EXA Express, Marea, New Cross Pacific, and SeaMeWe-6 per TeleGeography data, making it one of the most active cable infrastructure investors among the hyperscaler group and generating landing station real estate requirements across multiple geographies. EXA Infrastructure, United Kingdom, completed its acquisition of Aqua Comms, Ireland, for approximately USD 59 million in December 2025 per RCR Wireless reporting of January 2026, creating a combined landing station and cable network operator with positions across the AEC-1, AEC-2, AEC-3/Amitie, and CeltixConnect cable systems and the primary cable landing station in Dublin's Clonshaugh Business Park. These are some of the key factors driving revenue growth of the market.

However, the global submarine cable landing station real estate market faces structural constraints that limit the pace and geographic distribution of new investment through the forecast period. Geopolitical security risk to cable landing station infrastructure has escalated materially, with the Russian vessel Yantar escorted from the Irish Sea in November 2024 after being caught patrolling above subsea cables and operating three drones per CSIS analysis of September 2025, and NATO's Project HEIST developing satellite rerouting capability for cable outage scenarios. These security incidents have increased the cost and complexity of landing station site selection, environmental impact assessment, and physical security infrastructure investment required for new cable landing station real estate development. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis affecting approximately 20% of global seaborne LNG flows, create upward pressure on the electricity costs of cable landing station operations which require continuous power for repeater power feeding, optical amplification, and network operations centre operations in landing station markets that depend on gas-fired electricity generation. Planning and permitting timelines for new cable landing stations in coastal marine environments are extending as environmental regulators in the EU, US, and Australia impose more rigorous coastal impact assessments, marine ecology surveys, and community consultation requirements on cable burial and landing infrastructure applications. These factors substantially limit global submarine cable landing station real estate market growth over the forecast period.

The submarine cable landing station is the most undervalued piece of real estate in the digital infrastructure ecosystem. Every byte of transatlantic data that Amazon, Google, Meta, and Microsoft transmit between their US and European data centre networks passes through a building that is typically 1,000 to 5,000 square metres in size, staffed by a handful of engineers, and generating no colocation revenue visible on an operator's income statement. But the hyperscalers are now building these stations themselves privately owned, purpose-designed for their own AI traffic loads because they have calculated that the cost of leasing capacity from a third-party landing station operator is lower than the risk of not controlling the physical interface between their submarine cable and their data centre network. Amazon's Fastnet station in Cork is not a real estate investment. It is a sovereignty decision. Once it opens in 2028, no third party will sit between Amazon's European data centres and its transatlantic network. Understanding that shift is the starting point for any serious institutional analysis of landing station real estate value over the next decade." Troview Intelligence Head of Global Submarine Cable Landing Station Research

SEGMENT INSIGHTS

Four Regions Defining Global Landing Station Real Estate Investment

| TeleGeography Cable Systems | New Investment 2025-2027 | Primary US Landing Hubs | Key Private Investors |

| 597 active or under construction globally | USD 13 Billion (TeleGeography, Dec 2025) | Virginia, New Jersey, Florida, California | Amazon, Google, Meta, Microsoft |

North America is the largest source of private submarine cable investment globally, with Amazon, Google, Meta, and Microsoft collectively accounting for the majority of new cable system construction financing announced in 2024 and 2025, fundamentally restructuring the ownership model of the global cable landing station real estate market from telecom consortium assets to hyperscaler-owned dedicated infrastructure. The US Atlantic coast concentrated in Virginia, New Jersey, and Florida hosts the largest concentration of transatlantic cable landing stations in the Americas, with NJFX in New Jersey serving as the US terminus for the Havfrue/AEC-2 system among others and Amazon's planned Maryland landing for the Fastnet system adding a new high-capacity terminus to the Mid-Atlantic landing cluster. Amazon's Fastnet cable, designed specifically to handle growing AI traffic loads with 320 Tbps capacity per AWS company disclosure, is representative of the AI-driven capacity upgrade cycle that is generating new landing station real estate demand independent of the incremental traffic growth of traditional telecommunications services.

| Key Atlantic Landing Hubs | Celtic Interconnector EU Grant | Geopolitical Security | Regulatory Driver |

| Ireland, UK, Portugal, France, Spain | EUR 530M+ world's longest XLPE interconnector | Russian Yantar escorted from Irish Sea, Nov 2024 | EU digital sovereignty cable route diversification |

Europe's cable landing station real estate market is undergoing its most significant structural transformation since the late 1990s transatlantic build-out, as EU digital sovereignty policy, hyperscaler European data centre expansion, and the geopolitical security incidents of 2024 collectively drive investment in new and diversified landing station real estate across Ireland, the UK, Portugal, France, and Spain. The EU's Global Gateway Forum in October 2025 confirmed European Commission support for the Medusa cable system's expansion into the Middle East as part of building digital resilience across the EU-MENA corridor per InterGlobix Magazine reporting of January 2026, and the Celtic Interconnector between Ireland and France received over EUR 530 million in EU grants as a Project of Common Interest. The concentration of hyperscaler data centre infrastructure in Ireland 82 data centres with Amazon's USD 11.9 billion investment since 2012 makes the island's cable landing station real estate the most strategically valuable in the EU, as every byte of transatlantic data serving Amazon's, Google's, and Meta's European data centre networks must pass through an Irish or UK landing station.

| APAC Cable Growth | Key Hubs | Google TalayLink | India TRAI Projection |

| 48% increase in deployed cable km forecast | Singapore, Japan, Australia, India, Hong Kong | Australia to Thailand new Indian Ocean route | 4x data transmission capacity increase by 2025 |

Asia Pacific is the fastest-growing cable landing station real estate region, driven by the AI-driven route diversification programmes of Google, Amazon, and Meta that are adding new cable systems and landing stations across Australia, Japan, Singapore, India, and emerging Pacific rim markets. Google announced TalayLink in November 2024 to connect Australia and Thailand via a new Indian Ocean route west of the Sunda Strait, creating landing station real estate requirements at both Australian and Thai termini on a route that does not duplicate existing cable corridors, per TeleGeography and verified trade press of December 2025. India's Telecom Regulatory Authority announced in January 2025 that India's data transmission capacity is projected to increase fourfold by 2025 with the activation of new submarine cable systems, with India hosting 17 international subsea cables across 17 landing stations per India Department of Telecommunications official data and TRAI Annual Report 2024, and NTT DATA commissioning a USD 400 million submarine cable in India in March 2025 per NTT company announcement, adding to the landing station real estate footprint in a market where hyperscaler investment in data centre infrastructure is generating demand for dedicated private landing station assets.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from verified company announcements, planning authority records, TeleGeography data, and verified trade press.