By REIT Structure · By Geography · By Property Grade · By Occupier Sector

Global listed office REITs generated record net operating income in 2025 as return-to-office mandates by JPMorgan Chase, Amazon, and Goldman Sachs drove occupancy to post-pandemic highs in Class A and trophy assets across New York, London, Tokyo, and Singapore while the FTSE EPRA Nareit Developed Extended Index posted a 10-year compound annual total return of 4.9%, affirming listed real estate as a durable income and capital growth vehicle for institutional allocators.

MARKET SYNOPSIS

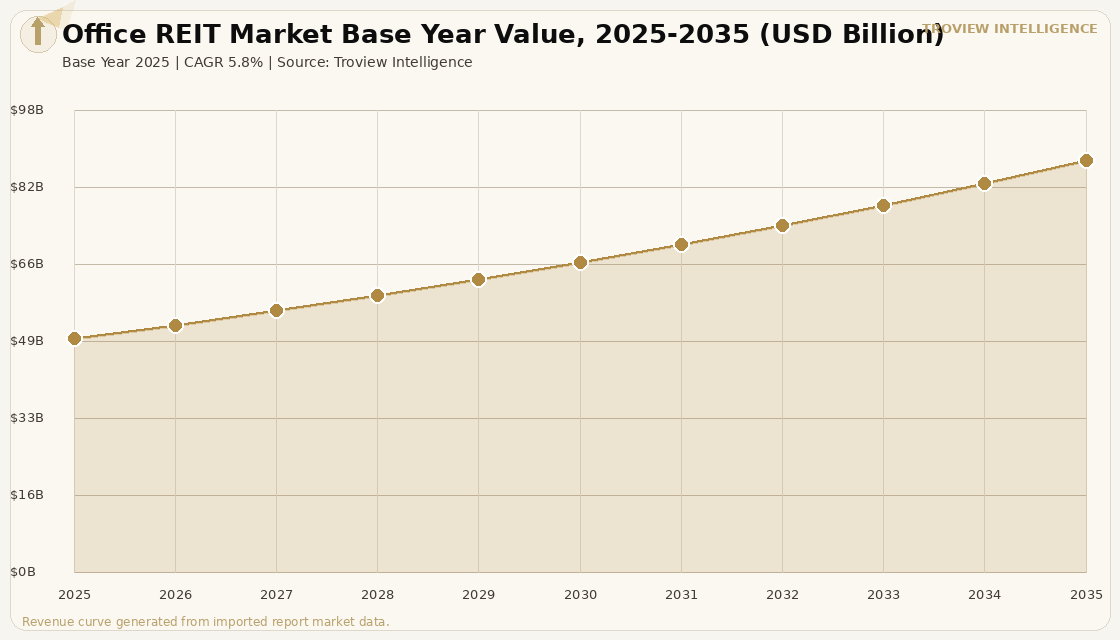

The global office REIT market size was USD 49.84 Billion in 2025 and is expected to register a revenue CAGR of 5.8% during the forecast period, reaching USD 87.77 Billion by 2035. Market revenue growth is supported by a decisive recovery in institutional-grade office demand across North America, Europe, and Asia Pacific, anchored by corporate return-to-office mandates that have restored occupancy in Class A buildings to above 85% mid-week utilisation in major gateway markets. The FTSE EPRA Nareit Developed Extended Index, which tracks listed real estate equities globally across 497 constituents in 38 countries with a total equity market capitalisation exceeding USD 2.5 trillion as of late 2024 per Nareit data, posted a 10-year compound annual total return of 4.9%, demonstrating the durability of listed REIT structures as income vehicles through multiple rate cycles. Office REITs specifically have benefited from the flight-to-quality dynamic that has concentrated demand in the top quartile of the building stock, enabling landlords to re-rate rents materially in trophy and Grade A assets while secondary stock faces conversion pressure and structural vacancy. The North American office REIT market leads globally, underpinned by the United States REIT framework established under the Real Estate Investment Trust Act, which requires high pay-out ratios and delivers tax-transparent dividend income to institutional and retail investors.

The global office REIT market is structured around the dominance of listed vehicles in North America, Japan, Australia, Singapore, and the United Kingdom, where REIT-enabling legislation has created transparent, liquid investment structures that allow institutional capital to access income-producing office assets without direct property ownership. The Tokyo Stock Exchange REIT market reached a total market capitalisation of approximately JPY 24 trillion as of March 2025, with 57 listed J-REITs, per the Japan Exchange Group guidebook, making it the second-largest listed REIT market globally after the United States. Asia Pacific REITs held a combined market value of approximately USD 235.8 billion as of year-end 2024 per EPRA data, confirming the region's structural importance to global office REIT capital allocation. Active managers of real estate funds reduced exposure to North America in 2025 and increased allocations to diversified Asia Pacific and retail Europe according to Nareit's global active managers tracker, reflecting a shift in risk-adjusted return expectations toward markets with tighter office supply and rising rents. For instance, in January 2026, Nippon Building Fund Inc., Japan, announced the acquisition of two prime office properties in central Tokyo, including Nihonbashi Honcho M-SQUARE completed in October 2025, for a total acquisition price of approximately JPY 46.9 billion from Mitsui Fudosan Co., Ltd. and Kajima Corporation, reflecting the continued appetite of Japan's largest office J-REIT to recycle capital from older assets into newly delivered Grade A buildings at tightening cap rates in the world's lowest-vacancy major office market. These are some of the key factors driving revenue growth of the market.

However, the global office REIT market faces structural constraints that moderate the pace of revenue recovery across the full investment universe. The Bank of Japan's policy rate hike in January 2025 raised both long-term and short-term interest rates in Japan, increasing borrowing costs for J-REITs that rely on leverage to enhance distributable income, and creating upward pressure on financing costs that has narrowed the positive spread between office yields and funding rates in Tokyo's core submarkets. In the United States and Europe, office REITs focused on suburban and secondary markets face continued earnings pressure as hybrid working policies reduce demand for non-prime locations, and Class B and C buildings face conversion or demolition rather than re-letting at market rents. BXP disclosed that it has completed asset dispositions exceeding USD 1 billion as part of a USD 1.9 billion multi-year asset sales plan to recycle capital from non-core suburban holdings into premier gateway market developments. Higher interest rates across developed markets have also compressed the yield spread that historically attracted institutional capital into listed office REITs relative to risk-free alternatives, requiring office REIT managers to demonstrate earnings growth through rent uplift and occupancy gains rather than yield compression. These factors substantially limit global office REIT market growth over the forecast period.

The global office REIT market has split into two parallel stories and institutional allocators need to be precise about which one they are buying. The trophy and Grade A segment in Tokyo, Singapore, New York, and London is operating at or near structural vacancy floors, with rents re-rating in ways that will compound earnings meaningfully through 2030 for REITs concentrated in those assets. The suburban and secondary segment is structurally impaired. The conversion pipeline that is removing Grade B and C stock from the office inventory is not a headwind for the top-tier REIT managers it is a tailwind, because it reduces the competing supply available to their tenants and strengthens their pricing power in every renewal cycle." Troview Intelligence Head of Global Listed Real Estate Research

SEGMENT INSIGHTS

By REIT Structure

Equity office REITs are expected to account for a significantly large revenue share in the global office REIT market during the forecast period.

Based on REIT structure, the global office REIT market is segmented into equity REITs, mortgage REITs, and hybrid REITs. Equity office REITs dominate both market capitalisation and distributable income, owning and operating office buildings directly and distributing rental income to unitholders after deducting operating costs, management fees, and financing charges. Listed equity office REITs in the United States, Japan, Australia, Singapore, and the United Kingdom collectively account for the majority of global office REIT market revenue, underpinned by regulatory frameworks that require distribution of 90% or more of taxable income. Mortgage office REITs are expected to register a lower revenue growth rate than equity REITs over the forecast period as rising interest rates in the United States and Japan have compressed the net interest margin available to mortgage REITs financing office acquisitions, and as institutional capital increasingly favours direct ownership through equity REIT structures for its transparency and liquidity advantages.

By Geography

North America office REITs are expected to account for a significantly large revenue share in the global office REIT market during the forecast period.

Based on geography, the global office REIT market is segmented into North America, Europe, Asia Pacific, and Middle East and Africa. North America dominates global office REIT market revenue, with the United States REIT market representing the most developed listed real estate ecosystem globally. The Asia Pacific office REIT segment is expected to register the fastest revenue growth rate over the forecast period, driven by Japan's combination of structurally tight office supply, strengthening corporate demand, and a Bank of Japan rate normalisation environment that is attracting foreign institutional capital from pension funds and sovereign wealth vehicles seeking yield above Japan Government Bond levels. Nareit's global active managers tracker confirms that institutional managers reduced North American allocations in 2025 and increased Asia Pacific exposure, with Japan and Singapore the primary beneficiaries of this rotation.

By Property Grade

Trophy and Grade A office assets held within listed REITs are expected to account for a significantly large revenue share in the global office REIT market during the forecast period.

Based on property grade, the global office REIT market is segmented into trophy, Grade A, Grade B, and Grade C assets. Trophy and Grade A buildings dominate REIT net operating income globally, as the flight-to-quality dynamic has concentrated tenant demand and rental growth in the top quartile of the stock across every major market. BXP's 54.6-million-square-foot portfolio spanning 187 properties, disclosed in its September 2025 investor filings, is focused exclusively on premier office assets in six major gateway markets, a strategy that has delivered NOI stability through the post-pandemic cycle. Grade B and Grade C office assets within REIT portfolios are expected to register declining income contributions over the forecast period as landlords accelerate conversion programmes and tenants continue to consolidate into higher-specification buildings with hospitality-grade amenities, sustainability credentials, and digital infrastructure.

REGIONAL ANALYSIS

NORTH AMERICA LARGEST MARKET

| Leading REIT | BXP (USD 3.5B+ Revenue) | Market Structure | Equity REIT dominant |

| Key Markets | New York, Boston, LA, San Francisco | Return-to-Office Driver | JPMorgan 5-day mandate Q1 2025 |

North America is the largest office REIT market globally, anchored by the United States REIT regulatory framework established under the Real Estate Investment Trust Act, which created one of the most liquid and transparent listed real estate markets in the world. BXP, operating a 54.6-million-square-foot portfolio across six major gateway markets per its September 2025 investor disclosures, and SL Green Realty Corp., Manhattan's largest office landlord with interests in 56 buildings totalling 31.4 million square feet per its December 2025 annual report, represent the largest pure-play listed office REIT vehicles in the region. Return-to-office mandates from JPMorgan Chase, Goldman Sachs, and Amazon in 2025 drove mid-week attendance to 72% to 75% in core Midtown New York buildings per the Real Estate Board of New York, restoring occupancy levels that support revenue growth for Class A and trophy concentrated REITs. BXP's multi-year asset recycling plan targeting USD 1.9 billion in dispositions, with USD 1 billion completed by January 2026, reflects the North American REIT market's active capital allocation dynamic between non-core disposals and premier development funding.

EUROPE ESG-LED

| Largest Market | United Kingdom and Germany | Key Driver | MEES and EPC compliance deadlines |

| Leading Vehicles | British Land, Derwent London, Gecina | Rate Environment | ECB rate cut cycle 2025 |

The European office REIT market is recovering from a prolonged valuation correction driven by rising interest rates between 2022 and 2024, with the European Central Bank's rate cut cycle initiated in 2024 and continued through 2025 reducing financing costs and improving the yield spread that underpins REIT earnings. The United Kingdom and Germany represent the largest listed office REIT markets in Europe, with UK REIT legislation enabling tax-transparent structures that have attracted capital into London West End and City office assets. Minimum Energy Efficiency Standards regulations in the United Kingdom, which require all commercial properties to meet EPC Band B by 2030, are accelerating capex cycles for REIT managers, with assets failing to meet the standard facing rental discounts and potential stranding. Gecina, France's largest listed office REIT, is navigating a bifurcated Paris market where La Defense Grade A vacancy has tightened while peripheral office stock faces structural challenges from hybrid work adoption. Nareit's global active managers tracker confirmed that European retail sector allocations increased in 2025, but European office REITs are beginning to attract renewed capital as rate normalisation stabilises valuations and ESG-compliant assets command green premiums.

ASIA PACIFIC FASTEST

| Asia Pacific REIT Market Value | USD 235.8 Billion (end 2024) | Japan J-REIT Market Cap | ~JPY 24 Trillion (March 2025) |

| Tokyo Grade A Vacancy Q3 2025 | 1.0% (18-year low) | Key Growth Markets | Japan, Singapore, Australia |

Asia Pacific is the fastest-growing office REIT region globally, underpinned by Japan's structurally tight office market, Singapore's safe-haven capital inflows, and Australia's recovering commercial property cycle. The Japan Exchange Group confirmed that 57 listed J-REITs held a combined market capitalisation of approximately JPY 24 trillion as of March 2025, making Japan the second-largest listed REIT market globally. Tokyo Grade A office vacancy fell to 1.0% in Q3 2025, the lowest level since Q3 2007, per the Ministry of Land, Infrastructure, Transport and Tourism of Japan's property market data, driving Grade A rents to JPY 39,750 per tsubo, the highest since Q1 2020. Singapore's Monetary Authority of Singapore-regulated REIT framework supports CapitaLand Integrated Commercial Trust, Keppel REIT, and Mapletree Pan Asia Commercial Trust as vehicles for institutional access to Singapore CBD Grade A assets, where vacancy compressed to 4.1% in Q1 2026. Active managers of global real estate funds increased Asia Pacific allocations in 2025 per Nareit's tracker, with Japan and Singapore receiving the largest share of reallocation from North America.