By Submarket - By Service Type - By Occupier Sector - By Certification

Submarkets: Saint-Denis - Pantin-La Courneuve - La Plaine - Saclay - Nozay-Essonne

Paris hosts more than 600 MW of installed carrier-neutral data centre capacity across 139 facilities with approximately 250,000 racks managed by 16 operators, Equinix operates ten Paris carrier-neutral campuses hosting 160-plus network providers and 100-plus cloud providers, France-IX handles over 4 Tbps of peak traffic from 270 members across Paris carrier-neutral facilities, and Mistral AI deployed 18,000 NVIDIA Grace Blackwell Superchips in a 40 MW carrier-neutral Essonne facility following a EUR 1.7 billion funding round, establishing Paris as Europe's primary carrier-neutral hub for sovereign AI infrastructure.

MARKET SYNOPSIS

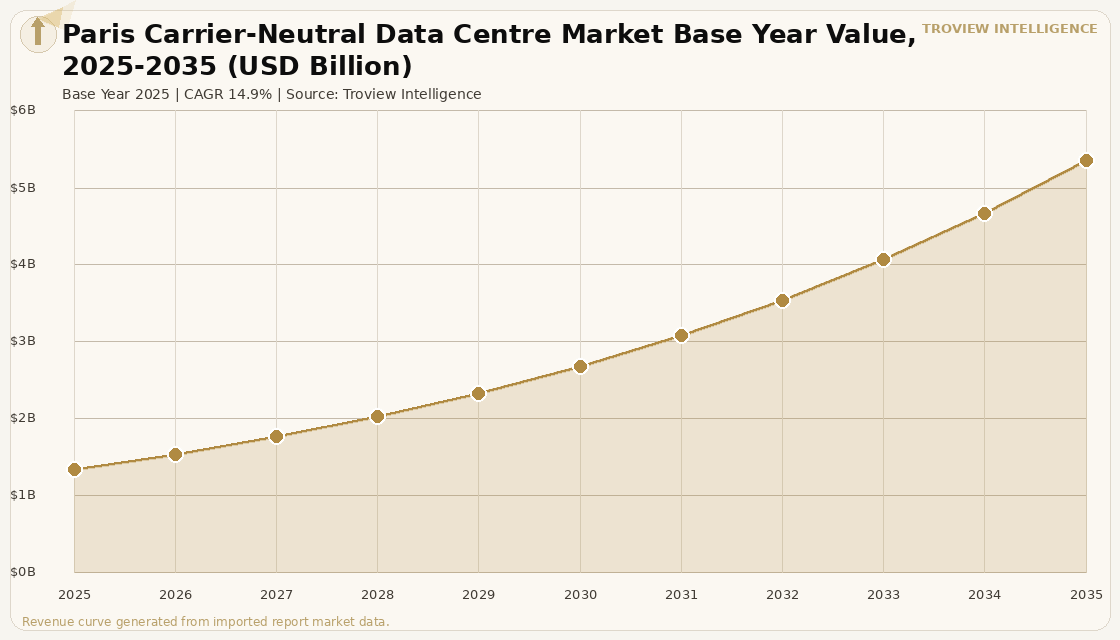

The Paris carrier-neutral data centre market size was USD 1.42 Billion in 2025 and is expected to register a revenue CAGR of 14.9% during the forecast period, reaching USD 5.68 Billion by 2035. Paris is France's primary carrier-neutral data centre market and Europe's fourth-largest carrier-neutral co-location hub, hosting more than 600 megawatts of installed capacity across 139 data centre facilities with approximately 250,000 racks managed by 16 major operators, with a rack density profile among the highest in continental Europe per October 2025 portfolio analysis. The Paris carrier-neutral ecosystem provides enterprises with access to France-IX, the primary French internet exchange with 270 members and over 4 terabits per second of peak traffic, alongside Equinix's Paris Internet Exchange that constitutes one of the leading traffic exchange points in France per verified operator data. Paris benefits from proximity to Normandy's subsea cable landing stations that connect the city to North American and African carrier-neutral ecosystems with lower latency than any other continental European hub. For instance, in February 2025, Equinix, United States, opened a new Paris facility adding 20 megawatts of IT load, the company's tenth Paris data centre, extending carrier-neutral interconnection across the metropolitan area with access to 160-plus network service providers and over 100 cloud service providers, per Equinix product disclosure and verified market data. These are some of the key factors driving revenue growth of the market.

The Paris carrier-neutral data centre investment market in 2025 is being reshaped by the convergence of France's EUR 109 billion AI infrastructure pledges with the physical constraints of the Ile-de-France metropolitan area, where land availability and EDF grid connection timelines in the established Saint-Denis and Pantin carrier-neutral clusters are causing new large-format development to migrate to Nozay, Essonne, and greater Paris peripheral sites while existing campuses pursue vertical expansion and density enhancement. Mistral AI's deployment of 18,000 NVIDIA Grace Blackwell Superchips in a 40 megawatt carrier-neutral facility in Essonne following its EUR 1.7 billion funding round with ASML as the largest shareholder established the operational template for sovereign AI carrier-neutral hosting in France and created a replicable infrastructure model that Eclairion, Scaleway, and other French HPC providers are now deploying across Paris carrier-neutral campuses. Data4 Group's PAR3 campus at Nozay in Essonne planned across 22 hectares of the former Nokia French headquarters with eight data centre buildings and EUR 1 billion in investment by 2030 represents the largest single-site carrier-neutral development in the Paris metropolitan area and will add 120 megawatts of capacity to the southern Ile-de-France corridor upon full build-out.

However, the Paris carrier-neutral data centre market faces structural constraints that limit supply delivery and raise operational costs. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are creating energy cost uncertainty that, while partially mitigated by France's nuclear power baseload from EDF, is affecting power purchase agreement negotiations for carrier-neutral operators committing to multi-hundred-megawatt capacity additions that require five to ten year energy price certainty. EDF capacity constraints in Ile-de-France could delay planned carrier-neutral campus deliveries by 12 to 24 months, with projects above 100 megawatts on a single site requiring extraordinary grid reinforcement measures that add cost and planning complexity beyond the standard connection process. The structural shift of hyperscale cloud providers toward self-built campus infrastructure in France with Microsoft's trio of self-built northern France sites, Amazon's self-built projects, and Google's campus expansions bypassing carrier-neutral facilities entirely for core cloud region capacity is reducing the hyperscale segment of Paris carrier-neutral demand growth and increasing operator dependence on enterprise, AI, and sovereign cloud segments for incremental occupancy. These factors substantially limit Paris carrier-neutral data centre market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "Paris's carrier-neutral market is at an inflection point. The ten-facility Equinix campus, France-IX with 270 members at 4 Tbps, and the established Interxion and Data4 campuses in Saint-Denis have made Paris one of the five most important carrier-neutral interconnection ecosystems in the world. The question for the next decade is whether Paris can absorb the AI infrastructure demand wave that France's EUR 109 billion pledge total is bringing without the grid and land constraints of Ile-de-France causing the most valuable new capacity to land in Hauts-de-France or Lyon instead. Mistral AI's choice of Essonne in the southern Paris metropolitan periphery, not in central Saint-Denis for its 40 MW GPU cluster is the signal. The carrier-neutral ecosystem of the established Paris campuses is the draw. The physical footprint of those campuses is the constraint. The next phase of Paris carrier-neutral development is about density squeezing more kilowatts per square metre out of existing white floor through liquid cooling, immersion, and direct-to-chip systems rather than greenfield expansion within the M25 equivalent ring." Troview Intelligence Senior Analyst, Paris Data Centre Markets

SEGMENT INSIGHTS

Submarket Deep-Dives

| Equinix Facilities | France-IX Peak Traffic | Cloud Providers Hosted | Network Providers |

| PA2, PA3, PA10 (Saint-Denis campus) | 4+ Tbps (270 members) | 100+ cloud providers | 160+ network service providers |

Saint-Denis is the primary carrier-neutral interconnection submarket in Paris, anchored by Equinix's PA2, PA3, and PA10 campuses at the Saint-Denis campus which collectively host the majority of Equinix's Paris interconnection ecosystem including a core node of the Equinix Internet Exchange, one of the leading traffic exchanges in France. The Saint-Denis submarket houses the France Internet Exchange France-IX which serves 270 members and handles over 4 terabits per second of peak traffic, making it the most dense peering environment in France and the primary cross-connect destination for ISPs, content delivery networks, and cloud providers requiring French domestic interconnection. Equinix's PA10 facility at Saint-Denis, opened as the company's most recent Paris addition, provides access to 120-plus networks and integrates heat recovery and water recovery sustainability systems aligned with French environmental regulations, while offering cloud-on-ramp connectivity to Amazon Web Services, Microsoft Azure, and Google Cloud via the Equinix Cloud Exchange.

| Data4 PAR5 Campus | Interxion Presence | Campus Strategy | Occupier Focus |

| Modular AI-ready build | Multiple large-format facilities | Modular expansion, long-term PPAs | Enterprise, media, telecoms |

The Pantin-La Courneuve corridor constitutes Paris's second carrier-neutral co-location cluster, hosting Data4's established PAR5 campus built around modular design with long-term power purchase agreements aligned to French renewable targets, and Interxion's large-format carrier-neutral facilities that serve enterprise, media, and telecommunications occupiers requiring co-location in established carrier-neutral campuses with direct fibre connectivity to Saint-Denis's France-IX peering ecosystem. Data4's PAR5 campus incorporates cooling systems designed for AI workload thermal output, positioning it to serve the GPU-dense requirements of AI model hosting that is growing as the fastest carrier-neutral demand segment in the Paris metro area. The La Courneuve submarket benefits from lower land costs than Saint-Denis while maintaining the dark fibre connectivity to Paris's primary carrier-neutral campuses that enterprise occupiers require for latency-sensitive hybrid cloud and co-location architectures.

| Data4 PAR3 Investment | Campus Capacity | Land Area | Key Tenant / Use Case |

| EUR 1 billion by 2030 | 120 MW (8 buildings) | 22 hectares (former Nokia HQ) | Mistral AI 18,000 Blackwell chips |

The Nozay-Essonne submarket in the southern Ile-de-France corridor is Paris's fastest-growing carrier-neutral development zone, anchored by Data4's PAR3 campus on the 22-hectare former Nokia French headquarters site in Nozay, which is being developed across eight carrier-neutral data centre buildings with a total investment of EUR 1 billion by 2030 and planned capacity of 120 megawatts, with district heating connectivity integrated into the campus design . Mistral AI's decision to deploy 18,000 NVIDIA Grace Blackwell Superchips across a 40 megawatt carrier-neutral facility in nearby Essonne following its EUR 1.7 billion funding round established the southern Ile-de-France corridor as France's primary sovereign AI carrier-neutral hosting zone, creating a physical precedent for GPU-dense carrier-neutral deployments in the Paris periphery that Eclairion, Scaleway, and other HPC providers are replicating. The Nozay-Essonne submarket benefits from EDF grid connections that are more available than in Saint-Denis's established cluster, lower land costs than central Paris, and proximity to the Saclay technology and research hub that hosts major French technology institutions including Institut Polytechnique de Paris and major corporate R&D campuses.