By Submarket · By Asset Class · By Occupier Type · By Cooling Technology

Submarkets: Shibaura-Osaki · Inzai (Greater Tokyo) · Fuchu · Tochigi · Yokohama

Tokyo had 74 existing and 26 upcoming data centres as of June 2025, with colocation take-up forecast to accelerate as AI inference demand from six global cloud providers with dedicated Tokyo regions drives rack power density requirements above 70 kW per rack, AirTrunk is expanding its TOK1 campus toward 300 megawatts with a 40 MW addition in May 2025, and Keppel DC REIT completed the USD 530 million Tokyo Data Centre 3 acquisition in Inzai City in December 2025 on a 15-year hyperscale lease, positioning the asset as the benchmark transaction for institutional REIT investment in the Greater Tokyo data centre market.

MARKET SYNOPSIS

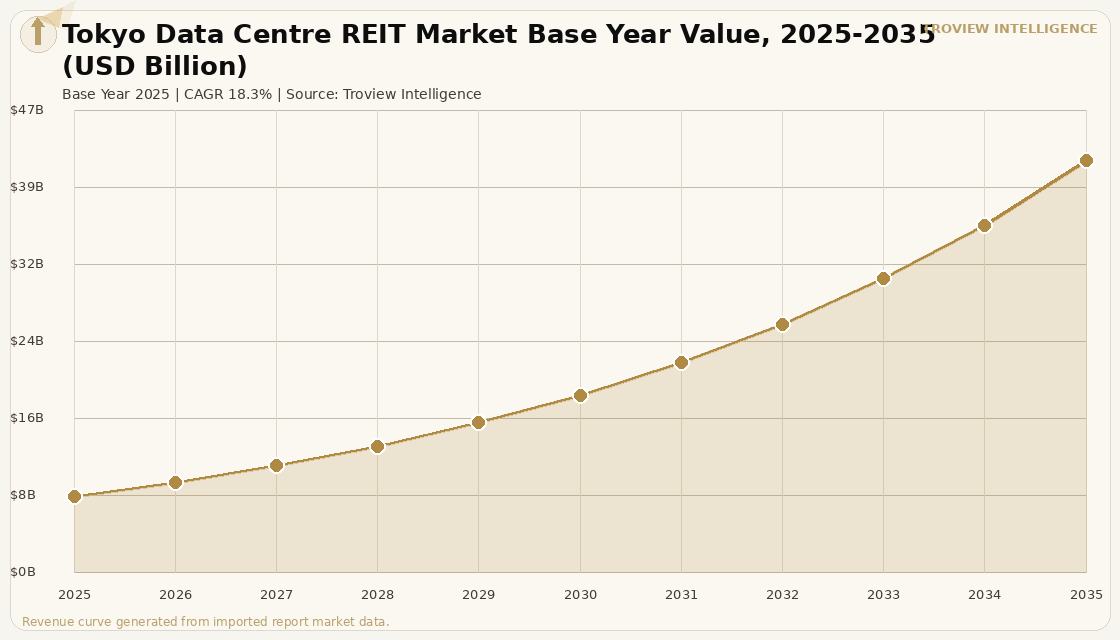

The Tokyo data centre REIT market size was USD 7.84 Billion in 2025 and is expected to register a revenue CAGR of 18.3% during the forecast period, reaching USD 42.19 Billion by 2035. Tokyo is the largest data centre market in Asia Pacific outside China, with 74 existing and 26 upcoming data centres as of June 2025 per verified operator data, hosting dedicated cloud regions for Amazon Web Services, Alibaba Cloud, Google, Microsoft, Oracle, and Tencent Cloud, all six of which require locally-deployed infrastructure to comply with Japan's data residency regulations and to serve enterprise and government workloads under the national GovCloud programme. Major co-location operators including AT TOKYO, NTT Communications, Equinix, Telehouse KDDI, and IDC Frontier alongside hyperscale operators AirTrunk and MC Digital Realty collectively anchor the Tokyo data centre investment market at above-1-gigawatt installed capacity per verified operator data. For instance, in December 2025, Keppel DC REIT, Singapore, completed the acquisition of Tokyo Data Centre 3 in Inzai City, Greater Tokyo, for JPY 82.1 billion (approximately USD 530 million), a freehold hyperscale data centre built in 2025 and fully leased to a leading global hyperscaler on a 15-year contract with annual rent escalations, with the acquisition expected to increase portfolio DPU by 2.8% immediately upon completion per Keppel DC REIT's SGX disclosure. These are some of the key factors driving revenue growth of the market.

The Tokyo data centre investment market in 2025 is being shaped by the convergence of AI inference demand which is pushing rack power density requirements beyond 70 kilowatts per rack and requiring immersion and direct-to-chip liquid cooling infrastructure with the physical and grid constraints of a dense urban market where land availability and power connection timelines in central Tokyo are causing operators to expand into Greater Tokyo submarkets including Inzai, Fuchu, Sagamihara, and Tochigi. AirTrunk's TOK1 campus added approximately 40 megawatts in May 2025 and is scaling toward 300 megawatts total, establishing one of the largest hyperscale campus footprints in the Greater Tokyo market, while Gaw Capital Partners and GDS are developing a 40 megawatt carrier-neutral campus in Fuchu Intelligent Park targeting end-2026 operations, both transactions demonstrating that foreign institutional capital is committing to Greater Tokyo hyperscale capacity at a pace that exceeds the volume of REIT-structured acquisitions. Equinix operates the TY series in Tokyo TY1, TY2, TY3, and TY4 as the dominant carrier-neutral co-location provider in the city, drawing cross-connect and cloud-on-ramp demand from financial institutions, trading firms, and enterprise customers requiring sub-millisecond connectivity to Tokyo's securities exchanges and market data infrastructure.

However, the Tokyo data centre REIT market faces structural constraints that limit supply delivery timelines and raise operational costs. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating electricity cost inflation for TEPCO, Tokyo's primary data centre utility provider, as Japan imports the majority of its LNG for electricity generation and has limited domestic alternatives at the scale required to serve multi-hundred-megawatt data centre campuses. Rising rack power density requirements for AI workloads above 70 kilowatts per rack are making existing air-cooled co-location inventory in central Tokyo submarkets structurally insufficient for the highest-demand tenant categories, requiring either expensive retrofit of existing facilities with liquid cooling infrastructure or migration of AI-workload demand to new-build campuses in Greater Tokyo that can accommodate the structural and power specifications of immersion and direct-to-chip cooling at design stage. The concentration of REIT-structured data centre investment in Greater Tokyo raises geographic concentration risk for portfolio investors in Keppel DC REIT and Digital Core REIT, with limited diversification available within a single city's data centre market. These factors substantially limit Tokyo data centre REIT market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "Keppel DC REIT's USD 530 million Tokyo Data Centre 3 acquisition at a 4% net property income yield on a 15-year hyperscale lease is not just a transaction it is a price-setting event for institutional REIT investment in the Tokyo data centre market. Every subsequent acquisition in Greater Tokyo will be benchmarked against it. What is significant about the Inzai City location is what it tells you about the geography of Tokyo's next data centre cycle: the central co-location campuses of Shibaura and Osaki are essentially full for large-format new supply due to grid and land constraints, and the growth is migrating to the arc of Greater Tokyo submarkets Inzai, Fuchu, Tochigi, Sagamihara where land is available, TEPCO connections are faster, and build-to-suit hyperscale campus development at 100+ megawatt scale is physically possible. REITs that established land positions in these submarkets in 2023 and 2024 are in a structurally advantaged position relative to those that will be competing for the next generation of assets at the pricing benchmarks that Keppel DC REIT just established." Troview Intelligence Senior Analyst, Tokyo Data Centre REIT Markets

SEGMENT INSIGHTS

Submarket Deep-Dives

| Dominant Operator | Co-location Revenue Profile | Connectivity Asset | Expansion Constraint |

| AT TOKYO, Equinix TY series | Highest per-sqm yield in Tokyo | Cross-connect, cloud-on-ramp | Land and grid essentially full |

The Shibaura-Osaki submarket in central Tokyo is Japan's most established data centre co-location district, anchored by AT TOKYO's multiple Shibaura facilities and Equinix's TY1 through TY4 campus that constitutes the primary carrier-neutral interconnection point for financial services, trading firms, and cloud providers requiring proximity to the Tokyo Stock Exchange and the Japanese securities market infrastructure. AT TOKYO provides carrier-neutral interconnection across its Shibaura campuses, hosting the majority of major Tokyo Internet Exchange participants, while Equinix's TY series draws cloud-on-ramp demand from enterprises deploying hybrid cloud architectures that require physical cross-connect to Amazon Web Services, Microsoft Azure, and Google Cloud within the same facility. New large-format supply in Shibaura-Osaki is essentially exhausted due to land scarcity and grid connection constraints in the submarket, which is directing all incremental hyperscale demand to Greater Tokyo locations in Inzai, Fuchu, and Sagamihara while keeping Shibaura-Osaki co-location rack rates and cross-connect pricing at premium levels supported by the structural scarcity of carrier-neutral space.

Inzai (Greater Tokyo) KEPPEL DC REIT BENCHMARK, HYPERSCALE CAMPUS ZONE

| Benchmark Transaction | Asset Type | Lease Term | DPU Accretion |

| Keppel DC REIT Tokyo DC 3 | Hyperscale, freehold, 2025-built | 15 years, annual escalations | 2.8% immediately upon completion |

Inzai City in Greater Tokyo's Chiba Prefecture has emerged as the primary hyperscale campus location for REIT-structured investment in the Tokyo data centre market, following Keppel DC REIT's December 2025 acquisition of Tokyo Data Centre 3 a freehold hyperscale facility developed by a joint venture of Colt Data Centre Services, Fidelity Investments, and Mitsui for JPY 82.1 billion (approximately USD 530 million). The five-storey facility is fully contracted to a leading global hyperscaler on a 15-year lease with annual rent escalations, providing the contracted revenue certainty and lease length that REIT investors require for hyperscale campus acquisitions at a price that reflects the quality of the tenant, the freehold land structure, and the scarcity of similarly-specified hyperscale capacity in the Greater Tokyo market. Inzai's advantages for hyperscale development include available large land parcels, TEPCO grid connection timelines that are more predictable than in central Tokyo, and proximity to major expressways that serve the logistics and staffing requirements of large-format data centre campuses.

| Announced Development | Capacity | Target Operational | Investor Profile |

| Gaw Capital + GDS joint venture | 40 MW carrier-neutral campus | End-2026 | Foreign institutional, HK-based |

Fuchu in western Tokyo is emerging as a carrier-neutral development zone for mid-scale data centre campus investment, with Gaw Capital Partners and GDS Services announcing a 40 megawatt campus in Fuchu Intelligent Park in April 2025, targeting end-2026 operations and designed to serve enterprise and cloud provider demand from organisations requiring connectivity to central Tokyo's co-location infrastructure at a lower land and power cost basis than the constrained Shibaura-Osaki core. The Gaw Capital-GDS joint venture represents one of the first Hong Kong-based and China-headquartered institutional capital entries into the Tokyo data centre development market in a carrier-neutral format, demonstrating that Fuchu's infrastructure profile access to the Chuo Expressway corridor, TEPCO grid availability, and industrial land at costs substantially below central Tokyo is sufficiently compelling for foreign investors to commit development capital at a scale that would not be viable in Shibaura or Osaki.