By Component · By Facility Size · By Tier Standard · By City

City Spotlights: London · Manchester · Birmingham · Edinburgh

Equinix committed GBP 3.9 billion to a 250 megawatt Hertfordshire campus in October 2025, Telehouse International broke ground on a GBP 275 million West Two facility in London's Docklands, the UK edge data centre market is projected to grow from USD 628.69 million in 2025 to USD 3.12 billion by 2035 at a CAGR of 17.22%, and UK electricity costs averaging 42 cents per kilowatt hour more than double the US rate of 16 cents represent the primary operational cost headwind for a market whose grid connection constraints are simultaneously creating a seven to ten year delay pipeline in Greater London and surrounding counties.

MARKET SYNOPSIS

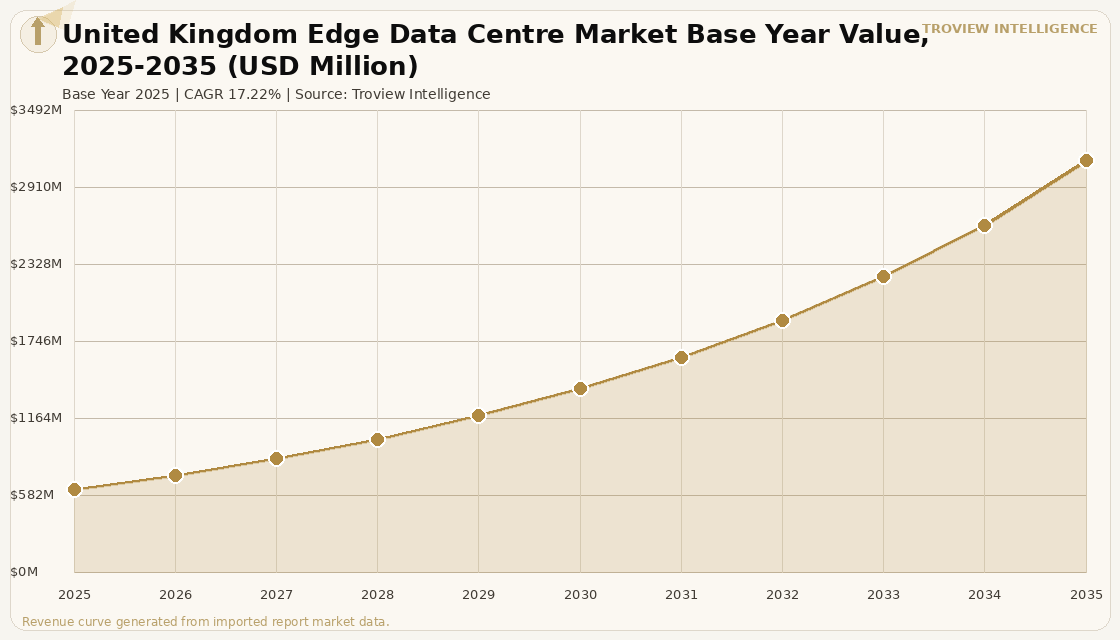

The United Kingdom edge data centre market size was USD 628.69 Million in 2025 and is expected to register a revenue CAGR of 17.22% during the forecast period, reaching USD 3,117.57 Million by 2035. The UK edge data centre ecosystem has emerged as the leading edge infrastructure market in Europe following the government's 2024 classification of data centres as Critical National Infrastructure and the January 2025 AI Opportunities Action Plan, which provided planning certainty for large-format facilities and directly preceded the approval of Equinix's 250 megawatt Hertfordshire campus application. The South-East commanded approximately 65% of 2025 UK data centre investment per verified industry data, anchored by London's 2.45 gigawatts of installed data centre capacity as confirmed by industry capacity tracking, with 274 data centre facilities across 110 operators in the London market and 24 facilities under construction at mid-2025. For instance, in October 2025, Equinix, United States, announced a GBP 3.9 billion investment in the DC01UK Hertfordshire campus, a 250 megawatt facility across 85 acres designed for AI and high-density compute workloads with operations targeted to commence in 2029 to 2030, representing the single largest committed data centre investment in UK history per The Register reporting of October 2025. These are some of the key factors driving revenue growth of the market.

VIRTUS Data Centres is the largest operator in the United Kingdom, followed by Equinix and Digital Realty, with VIRTUS London5 constituting the largest single UK data centre facility at approximately 50,000 square metres and around 90 megawatts per verified operator data. The Planning and Infrastructure Act 2025, which took effect in November 2025, reclassified sites above 50 megawatts as Nationally Significant Infrastructure Projects, reducing approval timelines that previously required full planning authority determination and enabling faster delivery of large-format edge and hyperscale facilities in regions where local planning friction had constrained supply. Manchester captured approximately 15% of new UK data centre build value in 2025, anchored by BT-AWS Wavelength Zones that embed edge compute directly into 5G radio access networks and by Kao Data's 30 megawatt campus that demonstrated mid-scale institutional appetite in secondary UK markets. The upcoming UK data centre pipeline is expected to reach 4 gigawatts across 21.5 million square feet, more than doubling existing capacity, driven by cloud and technology company demand concentrated in London, Manchester, and Birmingham per verified industry data.

However, the United Kingdom edge data centre market faces structural constraints that limit the pace of supply delivery. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation in the UK, where electricity already averages 42 cents per kilowatt hour substantially exceeding the 16 cents in the United States and 8 cents in China creating operational expense disadvantages that threaten the UK's ability to compete for edge infrastructure investment relative to continental European locations with lower energy costs. National Grid ESO's pause on new 132 kV connection offers in parts of Greater London and surrounding counties has created seven to ten year connection delays for developers unable to fund bespoke upstream reinforcement, with project budgets rising by approximately GBP 150 million for a 100 megawatt campus under self-funded reinforcement arrangements. Water utility constraints and planning headwinds in Slough and Docklands have caused developers to evaluate Manchester, Scotland, and the West Midlands as alternative locations, dispersing capital from the primary London market and extending delivery timelines for projects in constrained geographies. These factors substantially limit United Kingdom edge data centre market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "The UK edge data centre market is in a genuine supply crisis relative to demand. Equinix has committed GBP 3.9 billion. Telehouse is spending GBP 275 million in Docklands. The government has classified the sector as Critical National Infrastructure. And yet the primary constraint on delivery is not capital or demand it is the electricity grid. A seven to ten year connection queue in Greater London means that facilities announced today will not be operational until the early 2030s in the best case. The operators who secured grid connections before the pause are in a structurally advantaged position. The ones who did not face either waiting, moving to Manchester or Scotland where SP Energy Networks still offers three-year energisation slots, or funding bespoke reinforcement at a cost premium that fundamentally changes the economics of the project." Troview Intelligence Head of UK Infrastructure Research

SEGMENT INSIGHTS

Four Cities Shaping the UK Edge Data Centre Market

| Installed Capacity 2025 | Facilities in Market | Under Construction | Colocation Take-Up Forecast 2025 |

| 2.45 GW (verified industry data) | 274 across 110 operators | 24 facilities | 183 MW (+58% from 2024) |

London is the largest data centre market in the United Kingdom and the second-largest in EMEA, with 2.45 gigawatts of installed capacity in 2025 projected to grow to 5.16 gigawatts by 2031 at a CAGR of 13.21% . Equinix operates 16 facilities across London and is the most interconnected operator in the market, drawing cloud-on-ramp demand from financial services, media, and enterprise customers requiring proximity to the London Internet Exchange hosted at Telehouse's Docklands campus. Telehouse's West Two groundbreaking in October 2025, adding 33 megawatts at a cost of GBP 275 million in the Docklands, expands a campus that already provides 530 carriers and service providers with sub-5 millisecond metro round-trip connectivity via an on-site 132 kV substation. Digital Realty's July 2024 Slough acquisition advanced its metro footprint to 14 facilities, while Ark Data Centres' Union Park site remains the largest single London facility at 63 megawatts per verified operator data.

| Share of UK New Build 2025 | Key Edge Anchor | Grid Connection Outlook | Key Development |

| ~15% of new build value | BT-AWS Wavelength Zones | SP Energy 3yr energisation | Kao Data 30MW campus |

Manchester captured approximately 15% of new UK data centre build value in 2025, anchored by AI Growth Zone grants that accelerated planning approvals and by SP Energy Networks' three-year grid connection offers that provide a structurally faster energisation pathway than the constrained London market. BT-AWS Wavelength Zones in Manchester embed Amazon Web Services edge compute directly into BT's 5G radio access network, creating a carrier-native edge compute deployment that serves sub-10 millisecond latency requirements for enterprise 5G private network customers across Greater Manchester's manufacturing, logistics, and financial services sectors. Kao Data's 30 megawatt Manchester campus, announced with a GBP 350 million investment commitment, will become operational in 2026 and represents the largest institutional investment in Manchester data centre capacity in the post-pandemic period, demonstrating that secondary UK markets can attract data centre capital when grid connectivity and planning conditions are more favourable than London.

| Industrial Edge Driver | Proximity to London | 5G Use Case | Market Profile |

| Advanced manufacturing | Rail: 82 min, M40 corridor | Thames Freeport private 5G | Emerging sub-10ms industrial |

Birmingham and the West Midlands are gaining traction as edge data centre locations on the strength of the region's advanced manufacturing base, including automotive assembly for Jaguar Land Rover and multiple Tier 1 aerospace suppliers, that requires sub-5 millisecond machine vision and robotic control plane latency at scale. The Thames Freeport private 5G initiative in the East Midlands corridor demonstrates the industrial edge use case that is driving data centre investment outside Greater London, with the freeport's manufacturing tenants requiring latency performance that the centralised cloud infrastructure serving London cannot provide across a 100-kilometre fibre route. Equinix and Digital Realty both include Birmingham in their UK regional expansion strategies, and the Planning and Infrastructure Act 2025's Nationally Significant Infrastructure Project pathway provides accelerated approvals for facilities above 50 megawatts in Midlands greenfield locations where grid constraints are less severe than in the South-East.

| Scottish Policy Driver | DataVita Expansion Plan | SSE Grid Outlook | Renewable Energy Profile |

| DataVita 500 MW 5yr target | GBP 500M across central belt | SSE competitive 3yr offers | Wind surplus, green PPA availability |

Edinburgh and Scotland's central belt are emerging as a credible alternative to the constrained South-East for large-format edge and hyperscale data centre investment, with DataVita announcing plans to double its capacity to 40 megawatts as an intermediate step toward a 500 megawatt target across central Scotland, representing a total investment of approximately GBP 500 million over five years per company announcement. SSE Networks continues to offer competitive three-year energisation slots for Scottish data centre developments, a structural advantage over the National Grid ESO pause affecting the South-East, while Scotland's renewable energy surplus from onshore and offshore wind provides operators with green power purchase agreement access at tariffs below the UK average electricity cost of 42 cents per kilowatt hour. Scotland's universities Edinburgh, Heriot-Watt, and Strathclyde provide AI and data science talent pipelines that increasingly attract hyperscaler-adjacent workloads requiring skilled operations staff in proximity to research institutions.