| TROVIEW INTELLIGENCE | Airport-Adjacent Hospitality Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Geography · By Hotel Category · By Guest Segment · By Airport Tier

The global airport hotel market reached USD 22.4 Billion in 2025 with the International Air Transport Association projecting global passenger numbers exceeding 4.7 billion by 2026, RevPAR at airport-positioned business hotels growing approximately 8.4% year-on-year in 2025 as Marriott International reported a 5.2% rise in global RevPAR in Q1 2025 with international RevPAR above 5%, Hilton Worldwide system-wide RevPAR growing 2.5% year-on-year in Q1 2025 with group travel leading at above 6%, Marriott ending 2025 with a record pipeline of approximately 610,000 rooms with 265,000 under construction a 15% year-on-year increase and Hilton opening a 157-room Hampton by Hilton at London Heathrow in July 2024 to capture transit and airport-adjacent demand as flight searches rose 14% year-on-year overall and 20% for long-haul routes in September 2025, confirming the structural connection between air passenger growth and airport-adjacent hospitality demand that makes the sector one of the most consistently performing real estate sub-classes within the global hospitality investment universe.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

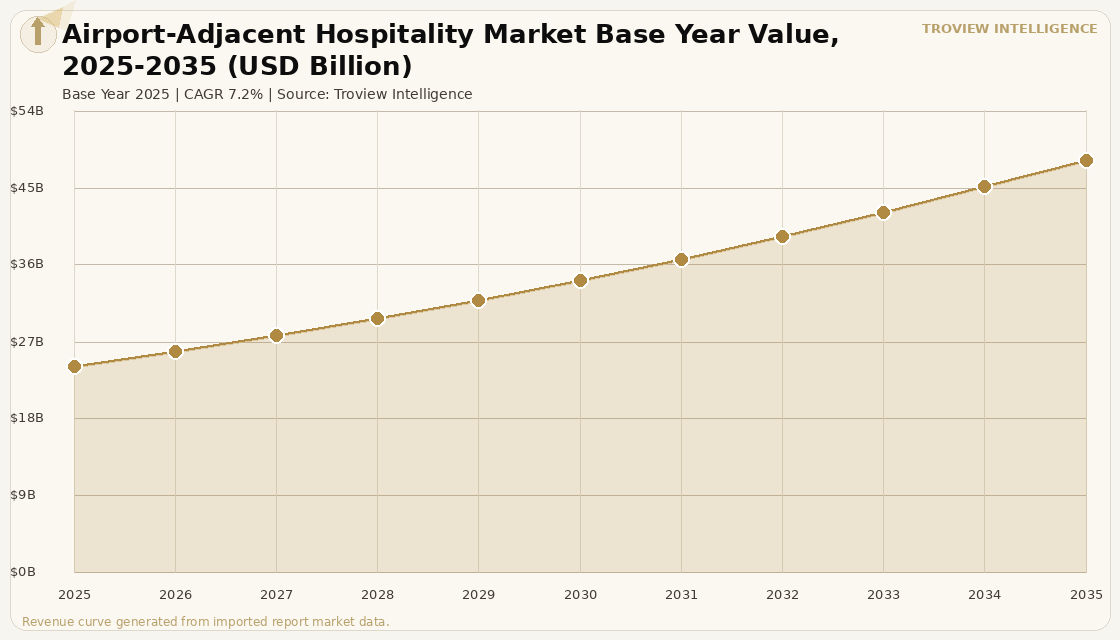

MARKET SYNOPSIS

The global airport-adjacent hospitality market size was USD 24.17 Billion in 2025 and is expected to register a revenue CAGR of 7.2% during the forecast period, reaching USD 48.26 Billion by 2035. The market encompasses branded hotel properties within direct walking distance or short shuttle connection of commercial airport terminals, including connected on-terminal hotels, airside-accessible facilities, and landside properties within approximately three kilometres of the terminal perimeter, together with their associated conference, food and beverage, and meeting venue revenue that serves the transit passenger, business traveller, crew layover, and airport-adjacent corporate demand base. Market revenue growth is supported by the direct structural linkage between air passenger volumes and airport hotel demand: the International Air Transport Association projects that global passenger numbers will exceed 4.7 billion by 2026, building on the recovery that saw global air passenger traffic surpass pre-COVID levels in 2024, with each incremental passenger generating demand for accommodation across the transit, early departure, delayed arrival, and extended layover occasions that airport hotels uniquely serve. RevPAR at airport-positioned business hotels grew approximately 8.4% year-on-year in 2025, driven by the resurgence in corporate travel spending as Fortune 500 companies, multinational consultancies, and government agencies increasingly routed business meetings through airport hotel conference facilities to minimise travel time for multi-city executives per marketintelo.com airport hotel market analysis of May 2026. Marriott International, United States, reported global RevPAR growth of 5.2% in Q1 2025, with international RevPAR above 5%, and ended 2025 with a record pipeline of approximately 610,000 rooms with 265,000 under construction a 15% year-on-year increase as the company signed approximately 1,200 deals covering 163,000 rooms in 2025 per Marriott Q4 2025 earnings disclosures. For instance, in July 2024, Hilton Worldwide Holdings, United States, opened a 157-room Hampton by Hilton at London Heathrow Airport specifically targeting transit and airport-adjacent demand as flight searches rose 14% year-on-year overall and 20% for long-haul routes in September 2025, positioning the property to capture international arrivals and crew layovers at Europe's busiest international airport per JLL UK Hospitality and Leisure Market Outlook 2025 and IATA 2025 air traffic data. These are some of the key factors driving revenue growth of the market.

Hilton Worldwide Holdings Inc., United States, reported system-wide RevPAR growth of 2.5% year-on-year in Q1 2025, with group travel leading at above 6% year-on-year, business transient RevPAR rising 2% year-on-year, and the company reaffirming its full-year 2025 system-wide RevPAR guidance of flat to up 2% per Hilton Q1 2025 earnings disclosures. Marriott International's Q4 2025 results showed EMEA RevPAR growth of approximately 7% in Q4, demonstrating the strength of demand recovery in the European airport hospitality market which hosts many of the world's busiest connecting hubs including London Heathrow, Amsterdam Schiphol, Frankfurt, Paris Charles de Gaulle, and Dubai International. North America led the global airport hotel market in 2025, commanding a 33.5% revenue share per marketintelo.com analysis, with the United States hosting over 30 major international airports each surrounded by dense clusters of branded hotel properties operated by global chains including Marriott's Courtyard and Renaissance brands, Hilton's DoubleTree and Embassy Suites brands, and IHG's Crowne Plaza brand. The American Hotel and Lodging Association's 2024 report documented 439 million sold room nights in 2023 in the US hotel industry, with business travel recovery generating product demand for hotels in downtown areas and near airports as the primary recovery vector for the upper-midscale and upscale segments per the Association's analysis. These are some of the key factors driving revenue growth of the market.

However, the global airport-adjacent hospitality market faces structural constraints that temper revenue growth across the forecast period. Iran-US geopolitical tensions and resulting disruption to Middle East airlift routes confirmed by CoStar Q2 2026 Global Hotel Market Forecast to be influencing ADR declines in the Heathrow and Gatwick airport submarkets as the drop in Middle East travellers and changes in airlift have limited pricing power illustrate the direct exposure of airport hotel RevPAR to geopolitical events that alter air passenger routing through major hub airports. Labour cost inflation, particularly in high-wage markets including Western Europe, the United States, and Australia, is compressing operating margins across the airport hotel sector with wage pressures averaging 6% to 9% annually in 2024 and 2025 per marketintelo.com analysis, while in the UK specifically Savills's 2025 UK Hotel Market Spotlight documented that GOPPAR declined 4.2% year-to-date driven by a 4.1% increase in labour costs from wage inflation, National Insurance contribution changes, and hiring challenges, with profit margins falling to 34.5% nationwide. The increasing dominance of online travel agency platforms and their commission structures of typically 15% to 25% of room revenue poses a sustained margin threat for airport hotels whose transient passenger customer base relies heavily on OTA discovery rather than direct brand loyalty channels. These factors substantially limit global airport-adjacent hospitality market growth over the forecast period.

Airport hotels have a guest mix that no city centre property can replicate: the transit passenger who has a five-hour connection and needs a bed, the crew member on a fourteen-hour layover who has no choice of location, the early departure guest whose 5am flight makes the airport hotel the only rational option, and the corporate executive who flew in from three time zones and is meeting the European team before flying out the same evening. These four guests are not price-elastic in the same way as a leisure tourist choosing between two hotels in central Paris. The transit passenger and the crew member have essentially zero elasticity: the product has no substitute at 2am in the terminal corridor. The corporate executive is booked on a company card and prioritises meeting room quality over rack rate. The early departure guest calculated the taxi fare to the city centre and concluded the airport room is cheaper. Airport hotels are not selling accommodation. They are selling proximity to infrastructure that their guests are already committed to using. That structural demand characteristic is why airport hotel RevPAR consistently outperforms urban hotel markets during periods of broader hospitality stress, and why the Marriott, Hilton, and IHG brands have each built systematic airport hotel portfolios rather than treating the segment as incidental to their urban strategies." Troview Intelligence Head of Global Airport-Adjacent Hospitality Research

SEGMENT INSIGHTS

Four Regions Defining Global Airport-Adjacent Hospitality Revenue

| North America Market Share 2025 | US International Airports | Marriott Q1 2025 US RevPAR | AHLA Sold Room Nights 2023 |

| 33.5% of global airport hotel revenue | 30+ major hubs each with branded hotel clusters | Up 0.7% full-year 2025; Q1 5.2% global | 439 million business travel recovery driver |

North America is the largest global airport-adjacent hospitality market, commanding 33.5% of global airport hotel revenue in 2025, anchored by the world's busiest domestic aviation network and by the concentration of mega-hub airports including Hartsfield-Jackson Atlanta, Dallas-Fort Worth, O'Hare International, and Los Angeles International, each surrounded by dense clusters of branded hotel properties from the major global chains. The American Hotel and Lodging Association's 2024 report confirmed that business travel recovery within the US hotel industry has begun, with 439 million sold room nights recorded in 2023 and the recovery of business travel generating the primary product demand for hotels near airports as corporate travel managers prioritise time efficiency over cost per night. Marriott International, operating the largest airport hotel portfolio in North America through its Courtyard, Renaissance, and Marriott branded properties at major US hubs, reported full-year 2025 US and Canada RevPAR growth of 0.7%, with group RevPAR increasing 2% reflecting the strength of corporate group meetings routed through airport hotel conference facilities for multi-city executive audiences.

| Marriott Q4 2025 EMEA RevPAR | CoStar Q2 2026 Finding | Gatwick 2024 Passengers | UK Hotel Revenue 2025-26 |

| ~7% growth | Heathrow/Gatwick ADR pressure from Middle East airlift drop | 43.2 million | ~GBP 27.5 Billion (Savills UK Hotel Market Spotlight 2025) |

Europe's airport-adjacent hospitality market is defined by the continent's mega-hub connecting airports London Heathrow, Amsterdam Schiphol, Frankfurt, Paris Charles de Gaulle, and Dubai acting as the primary Middle East gateway to European destinations which collectively generate the highest-density airport hotel demand zones in the Eastern Hemisphere. Marriott International reported EMEA RevPAR growth of approximately 7% in Q4 2025, demonstrating the strength of European airport hotel recovery in the fourth quarter that traditionally benefits from the peak corporate travel and conference season. CoStar's Q2 2026 Global Hotel Market Forecast documented that the Iran-US geopolitical conflict has influenced ADR declines in both the Gatwick and Heathrow airport submarkets as the drop in Middle East travellers and changes in airlift have limited pricing power at the two largest UK airport hotel clusters, illustrating the direct exposure of European airport hotel RevPAR to geopolitical events that alter the routing of premium long-haul connecting passengers. Hilton opened a 157-room Hampton by Hilton at London Heathrow in July 2024 targeting transit and airport-adjacent demand, aligning with the recovery in long-haul flight capacity where flight searches rose 20% for long-haul routes in September 2025.

| Marriott Q4 2025 APAC RevPAR | IATA 2026 Projection | Key Hubs | Pipeline Driver |

| ~9% growth | 4.7 billion global passengers | Singapore Changi, Tokyo Haneda, Dubai (gateway) | India, Southeast Asia, China airport expansion |

Asia Pacific is the fastest-growing region for airport-adjacent hospitality, with Marriott International reporting APAC RevPAR growth of approximately 9% in Q4 2025 the strongest regional performance in the company's global portfolio driven by the recovery of inbound tourism to Japan and Southeast Asia, the expansion of domestic Chinese aviation, and the continued growth of Singapore Changi and Dubai International as the premier long-haul connecting hubs for traffic between the Asia Pacific and European and North American markets. The IATA projection of global passengers exceeding 4.7 billion by 2026 is disproportionately weighted toward Asia Pacific growth, as India's aviation market is adding more than 100 new domestic routes annually, Indonesia's low-cost carrier network is expanding secondary city connectivity, and Vietnam's airport infrastructure is being upgraded to accommodate tourist arrival growth. Airport hotel supply in the Asia Pacific market is structurally undersupplied relative to passenger volumes at key hubs including New Delhi Indira Gandhi, Mumbai Chhatrapati Shivaji, and the secondary tier of Southeast Asian international airports including Kuala Lumpur, Bangkok, and Jakarta where branded hotel supply adjacent to terminals has not kept pace with passenger growth.