By Corridor · By Occupier Sector · By Building Grade · By Border Crossing

Prologis completed its acquisition of Terrafina's 41 million square foot Mexico portfolio in 2025, bringing its national total to approximately 90 million square feet and 8.1% market share, as the nationwide industrial inventory closed Q3 2025 at 109 million square metres with annual growth of 5% and Monterrey the largest market at 203 million square feet entered 2025 with over 20 million square feet available, a temporary supply surplus that developers including VYNMSA, FINSA, and Vesta continued to build through despite the normalization, citing the long-term nearshoring structural case.

MARKET SYNOPSIS

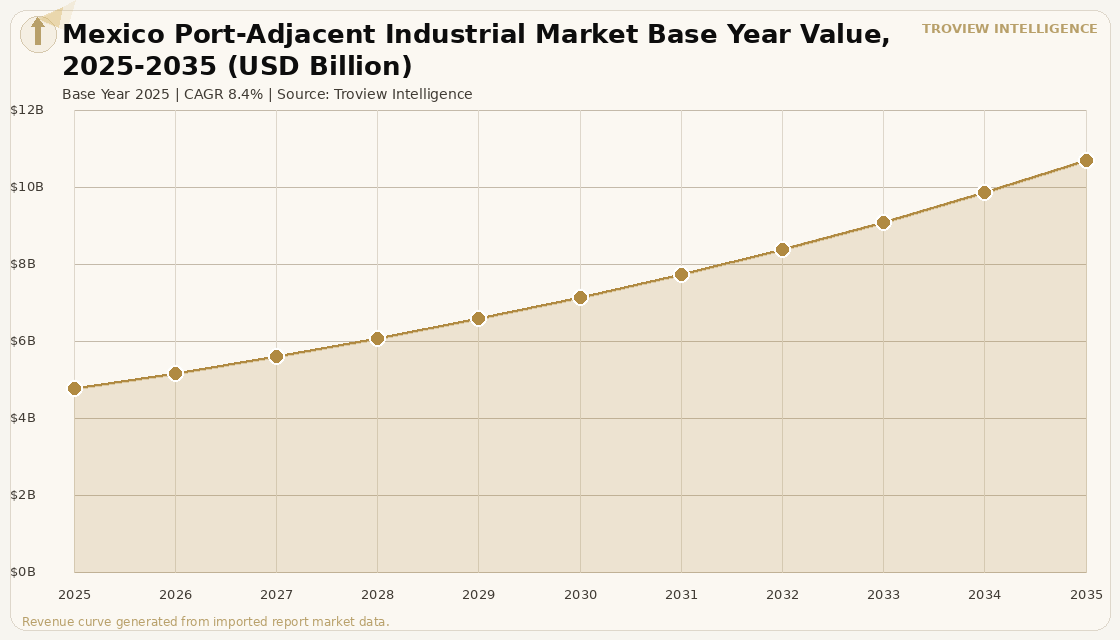

The Mexico port-adjacent industrial market size was USD 4.82 Billion in 2025 and is expected to register a revenue CAGR of 8.4% during the forecast period, reaching USD 10.80 Billion by 2035. Mexico's port-adjacent industrial market encompasses the industrial corridors concentrated near the country's land ports of entry with the United States primarily the Laredo-Nuevo Laredo, El Paso-Ciudad Juárez, Otay Mesa-Tijuana, and McAllen-Reynosa crossings as well as the seaport-adjacent industrial zones at Manzanillo, Veracruz, and Lázaro Cárdenas that serve as the primary entry points for Asian imports into the Mexican and North American markets. Mexico's nationwide industrial inventory reached 109 million square metres in Q3 2025, representing 5% annual growth, per Solili industrial data. The nationwide vacancy rate closed Q3 2025 at 4.4% with 4.8 million square metres of vacated space, reflecting a supply normalization cycle after the speculative construction surge of 2022 to 2024 that anticipated nearshoring demand at a pace that did not fully materialise in the near term. Lease rents surged approximately 50% over five years across Mexico's top industrial markets per industry analysis, driven by nearshoring demand and a strong Mexican peso that increased USD-denominated rent values.

Mexico's industrial real estate market entered a normalisation phase in 2025, with the nearly 50% decline in H1 2025 absorption versus the prior year reflecting decision delays from US trade policy uncertainty rather than a structural retreat from nearshoring. Monterrey and Mexico City remained the market leaders, each recording approximately 300,000 square metres of leasing in Q3 2025 per Solili data, while border markets including Tijuana and Reynosa saw negative net absorption as new vacant inventory and tenant move-outs in the period outpaced new commitments. The industrial market is demonstrating increasing sophistication, with 96.5% of Monterrey's market consisting of Class A properties per Prodensa market analysis, and occupiers showing a stronger focus on energy availability, park infrastructure quality, and environmental certifications when making site decisions. Prologis consolidated its Mexico market position through its acquisition of Terrafina's 41 million square foot portfolio, bringing its national total to approximately 90 million square feet and 8.1% of total market share per industry reporting. For instance, in Q4 2025, Monterrey's industrial market recorded significant lease transactions in Ciénega de Flores and Apodaca, including a 241,100 square foot lease by Ulsee and a 221,700 square foot lease by Dana, with the overall market inventory reaching 120.5 million square feet by year-end and space under construction at 7.3 million square feet, per Newmark Q4 2025 Monterrey market data. These are some of the key factors driving revenue growth of the market.

However, the Mexico port-adjacent industrial market faces structural constraints. Energy availability remains the single most significant operational barrier to nearshoring investment, with over 25,000 megawatts of private-sector power projects stalled due to regulatory bottlenecks and insufficient grid capacity in key industrial markets including Monterrey and the Bajío region. Security concerns at border crossings and along freight corridors, including periodic freight disruptions tied to organised crime activity, increase operational costs for manufacturers and logistics operators dependent on predictable cross-border transit times. US tariff uncertainty has extended corporate decision timelines, with companies that had planned to commit to new Mexico manufacturing facilities in 2024 and early 2025 adopting a wait-and-see posture that delayed absorption. Mexican peso volatility and the 2025 US-Mexico trade friction created by tariff threats have introduced USD/MXN exposure risk for companies structuring long-term peso-denominated lease commitments against US dollar revenues. These factors substantially limit Mexico port-adjacent industrial market growth over the forecast period.

Mexico's industrial market in 2025 is a story of two timelines. The near-term story is normalisation supply ran ahead of demand, vacancy rose from historic lows, and tariff uncertainty put large decisions on hold. The long-term story has not changed: Mexico is the only country that combines a 2,000-mile land border with the United States, a workforce of 55 million manufacturing-age workers, and a trade regime that makes Mexican production structurally cheaper than Chinese production for US market access. The 50% rent increase over five years is not reversing. Developers building speculatively in Monterrey and Pesquería are making a statement that the structural demand case remains intact and that the normalisation is temporary. The evidence from history supports them." Troview Intelligence Head of Mexico Industrial Real Estate Research

SEGMENT INSIGHTS

By Corridor

The Monterrey-Laredo land port corridor is expected to account for a significantly large revenue share in the Mexico port-adjacent industrial market during the forecast period.

Based on corridor, the Mexico port-adjacent industrial market is segmented by the primary border crossing and logistics axis. The Monterrey-Laredo corridor dominates, with the Laredo-Nuevo Laredo crossing processing the largest commercial vehicle volumes of any US land border port of entry and Monterrey's 203 million square foot industrial inventory serving as the manufacturing base that feeds that crossing. The Tijuana-Otay Mesa corridor serves the US-Pacific trade axis, with Tijuana's 102 million square foot inventory including significant electronics, medical device, and aerospace manufacturing in CODEX, FINSA, and American Industries parks. Ciudad Juárez-El Paso is the third primary corridor, serving automotive supply chains for US auto assembly in Texas and the broader southwest, with General Motors, Foxconn, and medical device manufacturers anchoring the Juárez industrial base. The Seaport corridor Manzanillo, Veracruz, Lázaro Cárdenas serves Asian import distribution into Mexico and is the primary entry point for automotive and electronics components manufactured in Asia for Mexican assembly plants.

By Occupier Sector

Automotive and aerospace manufacturing occupiers are expected to account for a significantly large revenue share in the Mexico port-adjacent industrial market during the forecast period.

Based on occupier sector, the Mexico port-adjacent industrial market is segmented into automotive manufacturing and supply chain, aerospace and defence manufacturing, electronics and medical devices, third-party logistics, FMCG and consumer goods distribution, and e-commerce. Automotive manufacturing dominated Monterrey's leasing with 25% of leased space historically per industry data, with Tier 1 and Tier 2 suppliers including Dana, Aptiv, and ZF Friedrichshafen establishing production facilities adjacent to their OEM customers. Automotive and electronics manufacturing together account for 52% of leased industrial space in the Monterrey region, reflecting the depth of the production ecosystem that has developed around the city's multi-decade manufacturing heritage. E-commerce is a fast-growing segment in Mexico City, where Mercado Libre's fulfilment network expansion and the entry of international e-commerce operators have driven logistics-oriented leasing separate from the manufacturing focus of the border corridors.

By Building Grade

Class A institutionally developed industrial parks are expected to account for a significantly large revenue share in the Mexico port-adjacent industrial market during the forecast period.

Based on building grade, the Mexico port-adjacent industrial market is segmented into Class A institutional parks, Class B functional industrial, and Class C informal and owner-built industrial. Class A facilities now account for 96.5% of Monterrey's market per Prodensa market analysis, the highest Class A concentration in Mexico and a reflection of the institutional developer activity of VYNMSA, FINSA, Vesta, Prologis, and American Industries over the nearshoring investment cycle. Class A concentration is lowest in Mexico City, where the market tightness at 1.8% vacancy pushes occupiers into functional Class B stock due to limited Class A availability. Average deal sizes in Monterrey increased 72.5% between 2019 and 2024 to 187,000 square feet per Prodensa data, reflecting the shift from small-format supplier commitments toward large-format OEM and Tier 1 anchors that require the specification standards that only Class A institutional parks can deliver.

Four Markets Defining Mexico's Port-Adjacent Industrial Sector

| Inventory (Monterrey, year-end 2025) | 120.5 million sq ft (Newmark Q4 2025) | Vacancy Q4 2025 | 7.5% (down from 7.8% prior quarter) |

| Leasing Q3 2025 | ~300,000 m² (Solili data, national leader alongside CDMX) | Average Asking Rent Q3 2025 | USD 6.66/m²/month (Fibra Mty/data Q3 2025) |

Monterrey is Mexico's largest industrial market and the dominant nearshoring hub for manufacturing serving the US market through the Laredo-Nuevo Laredo land port of entry, the highest-volume commercial vehicle crossing in the United States. Automotive manufacturers including Kia, KIA Motor, and their Tier 1 supplier networks anchor the Apodaca, Pesquería, and Santa Catarina corridors. Average asking rents stood at USD 6.66 per square metre per month in Q3 2025 per Fibra Mty Q3 2025 data, 4.3% below the prior year as the market absorbed the speculative supply surge that delivered over 600,000 square metres of new space in Q3 2025 alone per Solili data. VYNMSA, FINSA, and Vesta collectively account for over 11 million square feet of construction starts between 2022 and Q1 2025. Vacancy at 7.5% by year-end 2025 is expected to decline as market demand reactivates and the construction pipeline moderates to 7.3 million square feet under construction per Newmark Q4 2025 data.

| Inventory | 102 million sq ft of industrial space | Availability Rate Q3 2025 | 12.58% (elevated from speculative delivery) |

| Average Asking Rent | USD 0.80/sq ft/month (Q3 2025, industry data) | Section 321 | Key location for US cross-border e-commerce fulfillment |

Tijuana is Mexico's primary Pacific-facing industrial market and a binational production platform uniquely positioned to serve both US domestic consumption through the Otay Mesa land port and Asia-Pacific import logistics through the Port of Ensenada. The market's Section 321 de minimis threshold advantage has attracted US and Asian e-commerce operators who use Tijuana facilities to fulfil small-value cross-border shipments into the US market without paying full import duties, creating a distinct logistics use case not available in other Mexican border markets. Electronics and medical device manufacturing in CODEX, Parque Industrial Pacifico, and American Industries parks anchor the manufacturing base, with companies including Samsung, LG, and multiple medical device manufacturers operating long-term facilities. Tijuana recorded negative net absorption in Q3 2025 as new vacant inventory entered the market faster than leasing activity, creating a temporary oversupply condition that is expected to normalise as tariff policy clarity returns.

CIUDAD JUÁREZ-EL PASO AUTOMOTIVE SUPPLY CHAIN ANCHOR

| Q3 2025 Net Absorption | 116,000 m² in Class A (+25% vs Q2 2025) | Key Sectors | Automotive Tier 1, electronics, aerospace |

| Major Occupiers | General Motors supply chain, Foxconn, medical device MNCs | Infrastructure | Santa Teresa rail crossing, El Paso International Airport |

Ciudad Juárez is Mexico's most automotive-concentrated industrial market, serving the US automotive assembly base in Texas and the broader North American vehicle production network through the El Paso-Juárez crossing. The market recorded 116,000 square metres of Class A net absorption in Q3 2025, a 25% increase over Q2 2025 and a strong rebound from the negative absorption of Q3 2024, per Fibra Mty Q3 2025 market data, confirming that the market's correction was temporary and that automotive and aerospace leasing has resumed. General Motors' supply chain, Foxconn's Juárez facilities, and multiple medical device manufacturers anchor the industrial base across parks including Bermúdez, FINSA Juárez, and Intermex. The Santa Teresa intermodal rail crossing, which provides direct rail freight access between Juárez-El Paso and US inland markets, gives Ciudad Juárez a multimodal advantage over purely road-dependent border crossings.

MEXICO CITY (CDMX) TIGHTEST MARKET, E-COMMERCE DRIVEN

| Availability Rate Q3 2025 | 1.8% (tightest market nationally) | Inventory | 192 million sq ft (second largest nationally) |

| Asking Rents Q3 2025 | USD 0.95/sq ft/month (highest in Mexico) | Key Drivers | E-commerce, last-mile, FMCG, pharma logistics |

Mexico City is the tightest industrial market in Mexico by availability rate, at 1.8% in Q3 2025 per industry data, and commands the highest industrial asking rents nationally at USD 0.95 per square foot per month. The market is driven by e-commerce logistics serving Mexico's largest consumer concentration of 22 million residents, with Mercado Libre's fulfilment network expansion and DHL's CDMX logistics investment driving major lease commitments in the Vallejo, Cuautitlán, and Tlalnepantla industrial corridors. Mexico City's industrial demand is structurally different from the border markets it is logistics and distribution-oriented rather than export manufacturing-oriented, and its proximity to the Port of Veracruz via the Mexico-Veracruz highway provides a seaport-adjacent supply chain connection for imported goods entering the domestic Mexican market. Stock grew 11% in 2024 as developers attempted to serve the constrained market, but vacancy remains minimal as each new delivery is rapidly absorbed by FMCG, pharmaceutical, and e-commerce operators.