| TROVIEW INTELLIGENCE | London Airport-Adjacent Hospitality Market | Q2 2026 |

| TROVIEW INTELLIGENCE · CITY INTELLIGENCE REPORT |

By Airport Cluster · By Hotel Category · By Guest Segment · By Terminal Zone

Cluster Profiles: Heathrow Bath Road · Heathrow On-Terminal · Gatwick North Terminal · Gatwick South Terminal · Stansted and Luton

London's combined Heathrow and Gatwick airports handled approximately 123 million passengers in 2024 Heathrow approaching its pre-pandemic record of 80.9 million and Gatwick recording 43.2 million making the London airport corridor the highest-density airport hotel demand zone in the European Union, with Hilton opening a 157-room Hampton by Hilton at Heathrow in July 2024 as long-haul route searches rose 20% year-on-year by September 2025, CoStar Q2 2026 specifically identifying both Heathrow and Gatwick airport submarkets as experiencing ADR pressure from reduced Middle East airlift volumes driven by the Iran-US geopolitical conflict, PwC projecting London RevPAR of GBP 158.80 in 2026 with occupancy at 81.6%, and the Bath Road hotel cluster within five kilometres of Heathrow's terminal perimeter hosting more than 100 branded hotel properties representing every major global hospitality brand confirming London's airport-adjacent hospitality market as simultaneously the highest-volume and highest-complexity airport hotel market in Europe.

| Standard License: USD 2,200 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

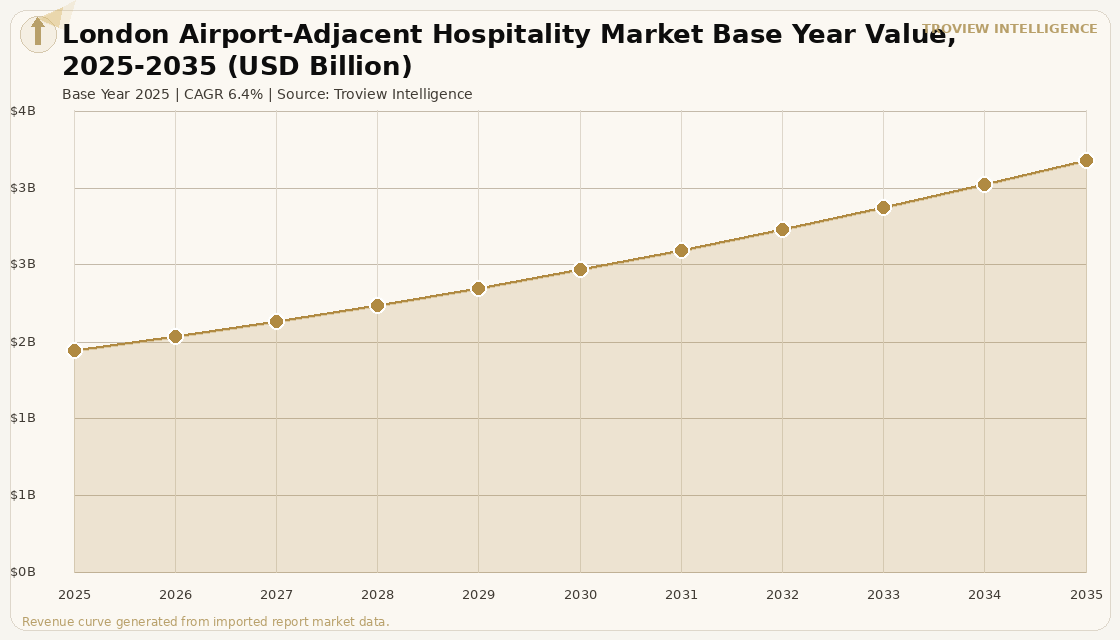

The London airport-adjacent hospitality market size was USD 1.87 Billion in 2025 and is expected to register a revenue CAGR of 6.4% during the forecast period, reaching USD 3.47 Billion by 2035. The market encompasses branded hotel properties within direct connectivity distance of London Heathrow, London Gatwick, London Stansted, and London Luton airport terminals including on-terminal and walkway-connected hotels, shuttle-served properties, and the Bath Road and Gatwick Triangle cluster developments within approximately five kilometres of terminal perimeters serving the combined passenger throughput of London's airport network that handled approximately 123 million passengers in 2024 through Heathrow and Gatwick alone. Heathrow Airport recovered toward its pre-pandemic record of 80.9 million annual passengers in 2024 as international air travel volumes surpassed pre-COVID levels globally, with the airport serving as Europe's busiest international hub and the primary connecting point for North Atlantic, Middle East, and Asia Pacific long-haul premium cabin traffic that generates the highest average daily rate demand events in the UK airport hotel market. Gatwick Airport recorded 43.2 million passengers in 2024 per Civil Aviation Authority data, maintaining its position as Europe's tenth-busiest airport, with the North and South Terminal structure generating airport hotel demand split between the premium Hilton London Gatwick, the accessible Hampton by Hilton, and the budget Premier Inn serving the airport's predominantly leisure-oriented point-to-point passenger base. PwC's November 2025 UK hospitality market outlook projected London RevPAR improving 1.8% in 2026 to GBP 158.80, with occupancy rising 1.7% to an average of 81.6%, confirming that the overall London hotel market trajectory supports revenue growth at airport-adjacent properties as international arrivals recover toward the 43.4 million projected for 2025. For instance, in July 2024, Hilton Worldwide Holdings, United States, opened a 157-room Hampton by Hilton at London Heathrow Airport targeting transit passengers, crew layover contracts, and early departure guests, positioned specifically to capture the recovery in long-haul flight demand that saw long-haul route searches rise 20% year-on-year in September 2025 per IATA 2025 global air traffic recovery data and JLL UK Hospitality and Leisure Market Outlook 2025. These are some of the key factors driving revenue growth of the market.

Savills's UK Hotel Market Spotlight 2025 confirmed that UK profit margins fell to 34.5% nationwide, driven by a 4.1% increase in labour costs from wage inflation, National Insurance contribution changes, and hiring challenges, representing a 4.2% year-to-date GOPPAR decline and illustrating the operating cost pressure that London airport hotel operators face as one of the UK's highest-wage employment markets. The Bath Road hotel cluster within five kilometres of Heathrow's terminal perimeter hosts more than 100 branded hotel properties representing every major global hospitality brand, making it the most densely branded hotel micro-market in the UK and one of the most competitive in Europe, with the Sofitel London Heathrow, Hilton London Heathrow Terminal 4 and 5, Park Hyatt Heathrow, Premier Inn Heathrow, IHG Crowne Plaza Heathrow, Marriott Courtyard Heathrow, and dozens of additional mid-range and budget branded properties collectively generating the competitive pricing environment that limits individual property pricing power in the absence of demand compression events. Marriott International, United States, ended 2025 with a record development pipeline of approximately 610,000 rooms globally with 265,000 under construction a 15% year-on-year increase demonstrating the major chain operators' continuing appetite for hotel development across their branded formats including at airport locations, although UK supply growth is expected to remain below pre-pandemic pipeline levels as construction costs stay elevated per Savills's analysis. These are some of the key factors driving revenue growth of the market.

However, the London airport-adjacent hospitality market faces specific constraints that limit revenue growth across the forecast period. CoStar's Q2 2026 Global Hotel Market Forecast directly identified both the Heathrow and Gatwick airport submarkets as experiencing ADR declines attributable to the Iran-US geopolitical conflict and its effect on Middle East traveller volumes and airlift routes through the two airports, with the report noting that while the aggregate European hotel market ADR forecast improved modestly, Heathrow and Gatwick moved to specific ADR decline projections as the premium long-haul Middle East connecting traffic which historically generates the highest rate compression events at both airports during peak Middle East travel seasons has partially displaced to alternative European hubs less directly exposed to Middle East route disruption. Labour cost inflation represents the most acute operating cost pressure at London airport hotels, as the London employment market's wage premium above UK national averages compounds the sector-wide NIC contribution increases and wage inflation that drove the nationwide 4.1% labour cost increase documented by Savills, creating above-national-average operating expense growth at Heathrow and Gatwick hotel operations that directly compresses gross operating profit per available room. Supply growth in London, while below pre-pandemic pipeline levels, is adding rooms at sufficient volume to constrain individual property rate growth during periods outside peak compression events, with PwC noting that fewer major London calendar events in 2026 relative to 2025 will limit the compression night pricing that airport hotels depend on to achieve above-trend RevPAR performance. These factors substantially limit London airport-adjacent hospitality market growth over the forecast period.

Heathrow is not one hotel market. The on-terminal Sofitel at Terminal 5 and the Premier Inn at the T2 shuttle bus stop are separated by a fifteen-minute drive, a GBP 150 per night room rate differential, and an entirely different customer. The Sofitel guest booked a premium transit room because their Singapore Airlines connection is sixteen hours away and they want a spa treatment and a dry-aged steak in the restaurant. The Premier Inn guest booked because their 5.45am easyJet flight to Malaga is the cheapest deal they could find and the GBP 89 Premier Inn rate looked better than a GBP 35 cab at 3am. The investors who price Heathrow airport hotels as a single micromarket are averaging two completely different operating models into one underwriting number. The correct analysis separates the on-terminal premium connected hotel business where the airline generates the demand, the guest has almost zero alternatives, and the rate follows the premium cabin load factor of the departing long-haul flight from the Bath Road cluster business, where one hundred branded hotels compete in a relatively transparent online market for cost-conscious corporate travellers who are price-comparing seven properties on their laptop the night before travel. Different cap rates. Different geopolitical sensitivity. Different operational leverage to labour costs. Same postcode." Troview Intelligence Head of London Airport-Adjacent Hospitality Research

SEGMENT INSIGHTS

| 03 | CLUSTER ANALYSIS |

Five London Airport Hotel Clusters Defining Market Geography

| Branded Hotels Within 5km | Heathrow 2024 Passengers | Hilton Hampton Opening | Corporate Corridor |

| 100+ properties, all major global brands | ~80 million (recovering toward 80.9M record) | 157 rooms, July 2024 | Bath Road, Stockley Park, Heathrow Gateway offices |

The Heathrow Bath Road cluster within five kilometres of Heathrow's terminal perimeter is the largest concentration of branded airport hotel supply in Europe, hosting more than 100 branded properties from the Sofitel and Park Hyatt at the upscale end through IHG's Holiday Inn and Crowne Plaza, Hilton's Hampton by Hilton (opened July 2024 with 157 rooms), DoubleTree, and Hilton Garden Inn, Marriott's Courtyard and Fairfield, and Premier Inn, Travelodge, and Ibis at the economy end, collectively serving the transit, crew, corporate, and early departure demand base of Europe's busiest international airport. The cluster benefits from the Bath Road and Stockley Park office corridor adjacent to the M4 motorway that generates corporate day meeting and extended-stay demand from technology, financial services, and professional services firms with Heathrow-adjacent operations a demand source that provides revenue diversification beyond pure air passenger dependency that the Gatwick cluster does not have at equivalent scale. Hilton's July 2024 opening of the Hampton by Hilton Heathrow was specifically positioned to capture the transit and crew demand as long-haul route searches rose 20% year-on-year by September 2025, adding a mid-price branded property to a cluster that had historically been weighted toward either premium connected hotels or budget economy properties without a strong mid-range branded offer.

| Sofitel Terminal 5 | Hilton Terminal 4 | Hilton Terminal 5 | Primary Demand |

| 605 rooms direct link to BA's primary terminal | 396 rooms connected walkway | Along Terminal 5 link | British Airways premium transit, long-haul crew, VIP |

Heathrow's on-terminal connected hotel zone anchored by the Sofitel London Heathrow at Terminal 5 with 605 rooms connected directly to British Airways's primary long-haul terminal, the Hilton London Heathrow Terminal 4 with 396 rooms serving the Terminal 4 Star Alliance carrier cluster, and additional Hilton properties in the Terminal 5 complex constitutes the premium tier of the London airport hotel market where room rates are determined by the demand characteristics of the airport's premium long-haul traffic rather than by competition with the 100-plus Bath Road cluster properties. The Sofitel's Terminal 5 connection makes it the natural overnight choice for British Airways Concorde Room members, First Class and Business Class passengers on long-haul connections, and crew from the airlines based in Terminal 5, generating a revenue profile that CoStar's Q2 2026 analysis confirmed is specifically sensitive to Middle East airlift volumes, as British Airways's extensive Middle East codeshare and connecting traffic through Terminal 5 is a primary driver of the high-rate compression events that the Sofitel commands during peak Middle East travel periods. The geopolitical sensitivity documented by CoStar that Heathrow and Gatwick ADR have declined as a result of the Iran-US conflict's disruption to Middle East airlift is most acute in this on-terminal premium tier where the premium Middle East connecting passenger represents the highest revenue per available room demand source.

| Gatwick 2024 Passengers | Hilton London Gatwick | Hampton by Hilton Gatwick | CoStar Q2 2026 |

| 43.2 million (Europe's 10th busiest) | Full-service, covered bridge North Terminal | Short walkway connection, mid-range | ADR pressure Middle East airlift changes |

The Gatwick hotel cluster is defined by the North-South Terminal split with the Hilton London Gatwick connected by a covered walkway bridge to the North Terminal serving the premium transit and business travel segment, and the Hampton by Hilton Gatwick providing the accessible mid-range option and by the predominantly leisure character of Gatwick's passenger base anchored by easyJet, Jet2.com, TUI Airways, and British Airways EuroFlyer short-haul leisure charter operations that generate early departure, late arrival, and airline crew demand with significantly lower average daily rate potential than Heathrow's long-haul business and premium transit mix. CoStar's Q2 2026 analysis documented ADR pressure at Gatwick alongside Heathrow as Middle East airlift changes from the Iran-US geopolitical conflict reduced the premium connecting traffic that generates Gatwick's above-average rate events, with British Airways and Middle Eastern carrier long-haul routes from Gatwick's South Terminal providing the primary above-market rate compression that distinguishes peak periods from baseline leisure transit demand. The Premier Inn Gatwick at the North Terminal provides five minutes' walk connectivity at economy pricing and consistently achieves above-90% occupancy during peak holiday travel periods as the price-sensitive leisure segment that dominates Gatwick's traffic generates the highest room night volume at the lowest rate in the London airport hotel market.

| Stansted 2024 Passengers | Luton 2024 Passengers | Hotel Profile | Demand Character |

| ~28 million (Ryanair, EasyJet primary base) | ~17 million (Wizz Air, Ryanair primary) | Budget dominant, Hilton Garden Inn, Holiday Inn Express | Economy leisure transit, crew, early/late flights |

London Stansted and London Luton represent the economy end of the London airport hotel market, serving the predominantly leisure and price-sensitive passenger bases of Ryanair, easyJet, and Wizz Air the three largest low-cost carriers operating from each airport whose passengers and crew generate the highest room night volume at the lowest average daily rate of any London airport cluster. Stansted's hotel provision is limited primarily to the on-airport Hilton Garden Inn and Radisson Hotel connected to the terminal, plus mid-range and budget properties within the Stansted Mountfitchet and Bishop's Stortford corridor accessible by shuttle, serving an airport that handled approximately 28 million passengers in 2024 with a route network dominated by European leisure and visiting-friends-and-relatives traffic that generates crew and early departure room night demand rather than the premium transit and corporate meeting demand that characterises Heathrow. London Luton's hotel cluster, anchored by Holiday Inn Express Luton Airport, Ibis, and Premier Inn, serves the Wizz Air and Ryanair leisure bases at Europe's most constrained single-runway airport, with accommodation demand concentrated around early morning departures and late arrivals on the budget leisure schedule and crew turnaround contracts that provide baseline occupancy floor throughout the year.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from verified company announcements, CoStar STR data, PwC and Savills research publications, and verified trade press.