By Submarket · By Occupier Sector · By Building Grade · By Developer

Monterrey ended 2025 with 120.5 million square feet of industrial inventory, 7.5% vacancy declining quarter-over-quarter, and 7.3 million square feet under construction as VYNMSA's Apodaca park, FINSA's Santa Catarina campus, and Vesta's Apodaca complex absorbed the speculative pipeline ahead of demand while 70% of new industrial activity came from the expansion of businesses already established in the market within the last three years, validating nearshoring as a sustainable operating strategy rather than a one-cycle opportunistic move.

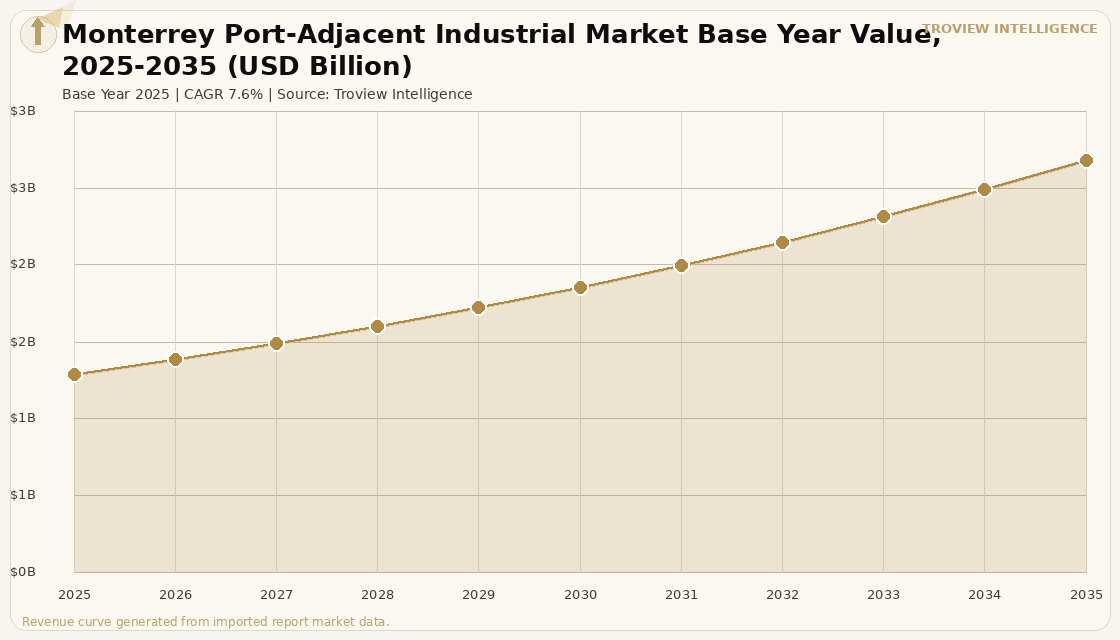

MARKET SYNOPSIS

The Monterrey port-adjacent industrial market size was USD 1.48 Billion in 2025 and is expected to register a revenue CAGR of 7.6% during the forecast period, reaching USD 3.08 Billion by 2035. Monterrey functions as the primary inland port-adjacent industrial market in Mexico, positioned 140 miles south of the Laredo-Nuevo Laredo land border crossing the highest-volume commercial vehicle port of entry in the United States by trade value. Goods produced in Monterrey's industrial parks exit Mexico through the Nuevo Laredo crossing and enter the US market directly, making Monterrey a land port-adjacent manufacturing hub equivalent in function to a coastal port industrial district. Total market inventory reached 120.5 million square feet by year-end 2025 per Newmark Q4 2025 market data, with vacancy at 7.5% declining from 7.8% in the prior quarter as market demand reactivated. Average asking rents stood at USD 6.66 per square metre per month in Q3 2025 per Fibra Mty Q3 2025 market data, 4.3% below the prior year but well above the pre-nearshoring boom level of USD 4.10 per square metre per month, confirming that the structural rent uplift from nearshoring has been retained through the normalisation cycle.

Monterrey's industrial ecosystem has evolved from a regional manufacturing base into Mexico's most mature institutional real estate market. Between 2019 and 2024 the market achieved compound annual growth of 18.9%, with total net absorption of nearly 94 million square feet across 659 leasing transactions per Prodensa proprietary market data. Average deal size grew 72.5% to 187,000 square feet by 2024, reflecting the shift from small-format supplier commitments to large OEM and Tier 1 anchor transactions. The automotive sector accounts for 25% of leased space and manufacturing overall for 52%, reflecting the depth of the supply chain ecosystem that has developed around the city's automotive, electronics, and aerospace base. Kia, BMW suppliers, and industrial conglomerates anchoring the Pesquería corridor operate at a scale that requires the institutional park infrastructure only VYNMSA, FINSA, Prologis, and Vesta provide. Seventy percent of new industrial activity in 2025 came from the expansion of businesses already established in Monterrey within the past three years per Prodensa analysis, confirming the compounding effect of an established manufacturing ecosystem. For instance, in Q4 2025, Dana Incorporated, United States, signed a 221,700 square foot lease in the Apodaca submarket, one of the two largest Q4 transactions in Monterrey, per Newmark Q4 2025 market data, reflecting continued Tier 1 automotive supplier commitment to Monterrey's industrial base despite the broader market normalisation. These are some of the key factors driving revenue growth of the market.

However, the Monterrey port-adjacent industrial market faces structural constraints. Vacancy rose from historic lows near 2.5% in 2022 to 7.5% at year-end 2025 as speculative supply substantially exceeded demand during the trade policy-uncertainty period of 2024 to 2025, with Monterrey delivering over 600,000 square metres of new space in Q3 2025 alone per Solili data a pace of supply addition that requires sustained demand reactivation to prevent further vacancy widening. Energy availability is the market's most cited operational constraint, with electric grid capacity insufficient to support the simultaneous commissioning of new manufacturing plants that require high-voltage power, creating connection wait times of 12 to 24 months in some industrial parks that deter time-sensitive occupiers. The Santa Catarina corridor had been anticipated as the location for Tesla's planned gigafactory before that project did not advance, a reminder that large-format manufacturing announcements do not always translate to physical leasing and that market expectations built on high-profile announcements can create supply surplus when those commitments do not materialise. Average rents declined 4.3% year-over-year to USD 6.66 per square metre per month in Q3 2025, signalling continued near-term pricing pressure as available inventory competes for a constrained pool of committed occupiers. These factors substantially limit Monterrey port-adjacent industrial market growth over the forecast period.

Monterrey is the most institutionally mature industrial market in Latin America. Ninety-six and a half percent Class A product, average deal sizes above 185,000 square feet, and 70% of new activity coming from existing tenants expanding their footprint these are the characteristics of a market where nearshoring has graduated from opportunistic to operational. The vacancy increase from 2.5% to 7.5% is real, but it is the natural consequence of developers who built ahead of demand during a period of genuine structural conviction. The question is not whether Monterrey recovers. It is how quickly the decision delays tied to US tariff policy resolve and whether the energy grid can be expanded fast enough to serve the backlog of companies with signed LOIs waiting for power connection." Troview Intelligence Head of Monterrey Industrial Real Estate Research

SEGMENT INSIGHTS

By Submarket

The Apodaca submarket is expected to account for a significantly large revenue share in the Monterrey industrial market during the forecast period.

Based on submarket, the Monterrey industrial market is segmented into Apodaca, Santa Catarina, Pesquería, Escobedo-Ciénega de Flores, Guadalupe, Salinas Victoria, and San Nicolás. Apodaca is the dominant submarket by leasing volume and institutional development activity, anchored by the Monterrey International Airport and hosting VYNMSA Apodaca Industrial Park, Vesta Park Apodaca, and multiple Prologis facilities. Apodaca and Guadalupe command the highest asking rents alongside Pesquería among Monterrey's nine submarkets. Pesquería is the fastest-growing submarket by new large-format supply, hosting Kia's assembly plant and its supplier ecosystem, with automotive and electronics manufacturers increasingly selecting Pesquería for its relative land availability compared to constrained Apodaca. Santa Catarina hosts FINSA's largest Monterrey campus and the corridor previously associated with Tesla's gigafactory site, offering lower rents than Apodaca and airport-adjacent submarkets while maintaining connectivity to the Monterrey ring road.

By Occupier Sector

Automotive manufacturing occupiers are expected to account for a significantly large revenue share in the Monterrey industrial market during the forecast period.

Based on occupier sector, the Monterrey industrial market is segmented into automotive manufacturing and supply chain, electronics and semiconductor, aerospace and defence, industrial manufacturing, third-party logistics, and furniture and consumer goods. Automotive accounts for 25% of leased space and manufacturing broadly for 52% per industry data, with the Tier 1 and Tier 2 supplier ecosystem serving Kia, BMW, Volkswagen, and General Motors assembly operations in the broader Nuevo León and Coahuila industrial corridor. Electronics and semiconductor manufacturing are fast-growing in the Pesquería and Apodaca corridors, as global semiconductor supply chain diversification has prompted Asian and European manufacturers to evaluate Monterrey as a production location for Texas Instruments and Intel's US customer base. Aerospace and defence manufacturing, including Tier 1 suppliers to Boeing and Airbus, occupies dedicated facilities in the Monterrey and Ciénega de Flores corridors.

By Developer

VYNMSA, FINSA, and Vesta are expected to account for a significantly large revenue share in new industrial development in the Monterrey market during the forecast period.

Based on developer, the Monterrey industrial market is dominated by VYNMSA, FINSA, Vesta, Prologis, and American Industries, with VYNMSA, FINSA, and Vesta collectively accounting for over 11 million square feet of construction starts between 2022 and Q1 2025 per Datoz construction data. VYNMSA led speculative construction with 6.4 million square feet concentrated in Apodaca and Santa Catarina, FINSA contributed 2.7 million square feet in Santa Catarina and Guadalupe, and Vesta exclusively developed within Vesta Park Apodaca. Prologis, after acquiring Terrafina's Mexico portfolio, operates multiple Monterrey parks and holds the largest single institutional ownership position in the city. Build-to-suit transactions accounted for 30% of Monterrey's 2019-2024 development cycle per Prodensa analysis, with BTS-for-lease and BTS-for-sale serving OEM customers who require facility specifications exceeding standard speculative product.

Submarket Deep-Dives

| Character | Highest lease volume, airport-adjacent, premium rents | Key Parks | VYNMSA Apodaca, Vesta Park Apodaca, Prologis Apodaca, CPA Apodaca |

| Key Q4 2025 Deal | Dana Inc. 221,700 sq ft lease (Newmark Q4 2025) | Rent Level | Among highest in Monterrey, alongside Guadalupe and Pesquería |

Apodaca is Monterrey's dominant industrial submarket, combining proximity to Monterrey International Airport with the deepest concentration of institutional Grade-A park inventory in the city. The airport adjacency serves aerospace, electronics, and high-value manufacturing tenants whose supply chains require airfreight access alongside road freight connectivity to the Laredo border crossing. VYNMSA's Apodaca park is the highest-volume development in the submarket, supported by Vesta Park Apodaca, multiple Prologis facilities, and CPA Logistic parks that collectively provide the most complete institutional industrial offering in Monterrey. Dana Incorporated's 221,700 square foot Q4 2025 lease in Apodaca confirms that Tier 1 automotive suppliers continue to commit to the submarket despite the broader normalisation, and Ulsee's 241,100 square foot transaction in the adjacent Ciénega de Flores submarket confirms extended demand into the northern Monterrey corridor.

PESQUERÍA AUTOMOTIVE OEM CORRIDOR, FASTEST GROWING

| Anchor Tenant | Kia Motors assembly plant and supplier cluster | Character | Large-format manufacturing, BTS-dominated, OEM-adjacent |

| Development | Speculative new supply driven by supplier follow-the-OEM strategy | Rent Level | Among highest asking rents in Monterrey market |

Pesquería has emerged as Monterrey's fastest-growing industrial submarket, anchored by Kia Motors' assembly plant that opened in Nuevo León and the supplier park ecosystem that has clustered around it following the automotive industry's standard follow-the-OEM location strategy. Tier 1 and Tier 2 Korean, European, and Mexican automotive suppliers have established facilities in Pesquería to serve Kia's production schedule with just-in-time delivery windows that require proximity to the assembly plant. Pesquería commands premium rents alongside Apodaca and Guadalupe per industry data, and its relative land availability compared to constrained Apodaca positions it to absorb additional large-format OEM-adjacent manufacturing investment. The submarket's growth has been dominated by build-to-suit transactions serving OEMs and Tier 1 suppliers who require facility specifications tailored to their production line requirements, including high-voltage power, heavy floor loads, and internal crane capacity.

| Key Developer | FINSA (2.7 million sq ft development 2022-2025) | Character | Lower rents than Apodaca, manufacturing and logistics mix |

| Former Tesla Site | Santa Catarina corridor associated with cancelled gigafactory | Connectivity | Monterrey-Saltillo highway, I-40 cross-border freight axis |

Santa Catarina is the primary FINSA development corridor in Monterrey, with FINSA Santa Catarina Industrial Park absorbing the largest single share of the developer's 2.7 million square feet of Monterrey construction starts between 2022 and Q1 2025 per Datoz data. The corridor offers lower per-square-metre rents than Apodaca and Pesquería while maintaining connectivity to the Monterrey ring road and the I-40 freight corridor connecting Monterrey to Saltillo and ultimately to the Ciudad Juárez-El Paso crossing that serves the automotive supply chains of northern Mexico. Santa Catarina became associated with Tesla's planned Nuevo León gigafactory, with the Santa Catarina site publicly identified as the leading candidate before the project did not advance, generating significant speculative development in anticipation of the supplier ecosystem that a Tesla gigafactory would have created. The corridor's broader manufacturing and logistics tenant base, independent of the Tesla association, provides stable occupancy for FINSA's institutional product.

ESCOBEDO / CIÉNEGA DE FLORES EMERGING CORRIDOR, VALUE INDUSTRIAL

| Key Q4 2025 Deal | Ulsee 241,100 sq ft lease (Newmark Q4 2025) | Character | Lower land costs, growing institutional presence, northern connectivity |

| NH-85 Access | Links Monterrey to Nuevo Laredo border crossing directly | Developer Activity | Institutional parks expanding; land more available than Apodaca |

Escobedo and Ciénega de Flores form Monterrey's northern industrial corridor, positioned directly on NH-85 the primary highway connecting Monterrey to Nuevo Laredo and the Laredo land border crossing that anchors the city's port-adjacent industrial identity. The corridor's northern position on the Monterrey-Laredo axis gives it the most direct logistical argument among all Monterrey submarkets for manufacturers whose primary market is the United States, with reduced transit time to the border versus southern Apodaca and Santa Catarina locations. Institutional developers are expanding their presence in Escobedo as Apodaca reaches land capacity and occupiers seeking competitive rents with port connectivity look north. The Ulsee 241,100 square foot Q4 2025 lease in Ciénega de Flores confirmed institutional-scale demand is active in the corridor. Land availability and lower entry rents compared to the established Apodaca and Pesquería submarkets position Escobedo-Ciénega de Flores as the most likely location for the next wave of large-format industrial development in Monterrey.