| TROVIEW INTELLIGENCE | Aparthotel Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Geography · By Stay Type · By End-User Segment · By Brand Tier

The global aparthotel market reached USD 12.45 billion in 2025 at a CAGR of 10.90% per Adagio corporate strategy disclosures and Accor Investor Day 2025 data with North America as the largest regional market, Adagio pursuing a target of 200 sites by 2028 and opening the 132-unit Adagio Access Nanterre adjacent to La Defense in February 2026, Staycity Group acquiring two sites in Battersea and Oxford in 2024 to 2025 with both buildings expected to complete in 2027, Frasers Hospitality adopting AI-driven workforce training in partnership with Google Cloud in September 2025, the UN Tourism World Tourism Barometer recording 690 million international arrivals in H1 2025 a 5% increase year-on-year with Europe welcoming nearly 340 million tourists and serviced apartments across Europe demonstrating stronger operational resilience than traditional hotels per HospitalityNet August 2025, with occupancy recovery supported by longer average lengths of stay and consistent weekday demand from corporate travellers confirming the aparthotel sector's structural performance advantage over conventional hotel formats.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

MARKET SYNOPSIS

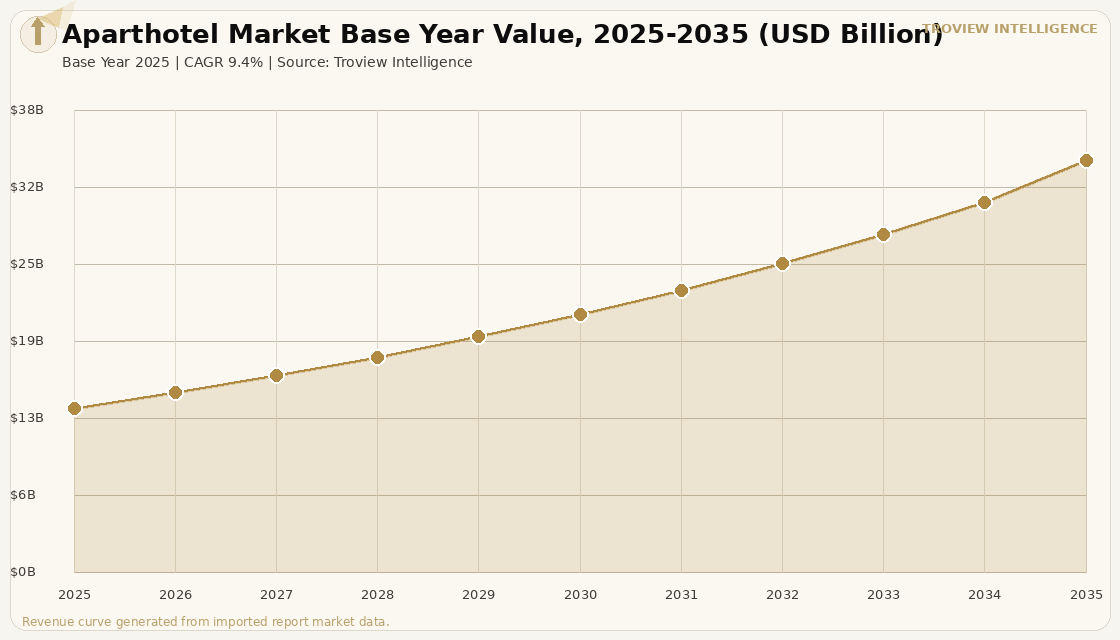

The global aparthotel market size was USD 13.62 Billion in 2025 and is expected to register a revenue CAGR of 9.4% during the forecast period, reaching USD 34.08 Billion by 2035. The market encompasses institutionally branded, hotel-operated apartment accommodation formats specifically aparthotels and apart-hotels operating under recognised operator brands that combine furnished studio, one-bedroom, and two-bedroom apartments with reception, housekeeping, and concierge services in a format that sits between a standard hotel room and a self-catered serviced apartment, targeting corporate short-stay, bleisure, and extended leisure travellers seeking greater space and kitchen facilities than a hotel room provides while retaining the operational consistency and brand guarantee of a managed hospitality product. Market revenue growth is supported by a structural shift in global travel behaviour toward longer durations, greater space, and kitchen-equipped accommodation that the UN Tourism World Tourism Barometer confirmed with 690 million international arrivals in H1 2025, a 5% increase year-on-year, with Europe welcoming nearly 340 million tourists per UN Tourism's biannual report and the European Travel Commission recording an 11% increase in seven-to-twelve-night trips in 2025 a stay duration that maps directly to the aparthotel's operational sweet spot. Serviced apartments across Europe demonstrated stronger operational resilience than traditional hotels in 2025, with occupancy recovery supported by longer average lengths of stay and consistent weekday demand from corporate travellers per HospitalityNet reporting of August 2025, translating into steady improvements in RevPAR supported by stable corporate contracts and reduced exposure to short-term leisure volatility. For instance, in February 2026, Adagio, France, the joint venture between Accor and Pierre and Vacances, opened the 132-unit Adagio Access Nanterre adjacent to La Defense in western Paris, the ninth property developed in partnership with Sergic and the latest addition to Adagio's national pipeline targeting 200 sites by 2028, with director of development Arthur Jaeger confirming three additional Ile-de-France openings planned for 2026 per Serviced Apartment News reporting of February 2026. These are some of the key factors driving revenue growth of the market.

The global apartment hotel market is projected to grow at a CAGR of 10.90% from 2023 to 2030 per Adagio and JLL extended stay market analysis, with North America holding the largest global market revenue share in 2025, underpinned by a mature corporate travel infrastructure and rising demand for extended-stay accommodation from technology, financial services, and healthcare sectors whose project-based workforce deployments generate sustained multi-week aparthotel demand across primary US metros. Frasers Hospitality Pte. Ltd., Singapore, adopted AI-driven workforce training in September 2025 in partnership with Google Cloud's AI Cloud Takeoff programme and Kyndryl, developing an AI agent application that analyses training videos to generate standard operating procedure documents and business process model notation flowcharts per verified company announcement of September 2025, illustrating the technology investment being made by leading operators to improve the operational efficiency of their global aparthotel portfolio. Staycity Group, Ireland, acquired sites in Battersea, London and Oxford in 2024 to 2025 with both aparthotel buildings expected to complete in 2027, and previously acquired a site adjacent to Nine Elms Station in London in July 2024 pursuing GBP 70 million of development financing under an operating leaseback structure per Knight Frank UK Serviced Apartment Market Review 2024, confirming active European aparthotel development pipeline investment by specialist operators. ActivumSG Capital Management, Germany, acquired nine aparthotel assets totalling 550 keys across Berlin, Bonn, Lubeck, Hamburg, Dusseldorf, Cologne, and Nuremberg with the aim of scaling the platform to a EUR 500 million-plus portfolio by the end of 2025 per market analysis, demonstrating institutional private equity appetite for European aparthotel portfolio assembly. These are some of the key factors driving revenue growth of the market.

However, the global aparthotel market faces structural constraints that limit the pace of revenue growth across the forecast period. Competition from short-term rental platforms including Airbnb and Vrbo exerts pricing pressure on aparthotel operators, particularly in leisure-oriented markets where platform supply has expanded materially since 2020 and where dynamic algorithm pricing responds to real-time demand more flexibly than institutionally managed aparthotel revenue management can match, limiting pricing power for aparthotel operators in the short-stay leisure segment. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis affecting approximately 20% of global seaborne LNG flows, create upward pressure on utility costs for aparthotel operators in LNG-dependent electricity markets, as apartment-format accommodation with kitchen appliances, laundry facilities, and individual climate control generates above-average energy consumption per unit relative to equivalent hotel rooms. Labour cost inflation particularly in high-wage markets including Western Europe, the United States, and Australia is compressing operating margins for aparthotel operators, with Savills UK Hotel Market Spotlight 2025 confirming that profit has been put under pressure from soaring energy costs in recent years and that easing inflationary pressures in 2024 to 2025 only provide partial relief. These factors substantially limit global aparthotel market growth over the forecast period.

The aparthotel is the hospitality sector's cleanest product-market fit for the modern business traveller who is not on a one-night stopover but is not relocating for six months. The management consultant on a four-week engagement in Frankfurt who wants to cook Sunday dinner in her apartment, do a load of laundry on Thursday, and have a breakfast option that is not a EUR 28 hotel buffet that guest is the aparthotel's structural demand anchor. She is not choosing the aparthotel over the hotel because it is cheaper. She is choosing it because the hotel format does not work for four weeks. The operators who understand this Adagio with 200 sites by 2028, Staycity building in Battersea and Oxford, ActivumSG assembling 550 keys across nine German cities are not competing with Airbnb any more than a Marriott Courtyard competes with a holiday home listing. They are building a managed hospitality product for a demand segment that the hotel format cannot serve and that Airbnb cannot guarantee. The pricing is between the two. The operational reliability is closer to the hotel. The space is closer to the apartment. That combination, delivered at scale with brand consistency, is the definition of a structural market opportunity." Troview Intelligence Head of Global Aparthotel Research

SEGMENT INSIGHTS

Four Regions Defining Global Aparthotel Revenue

| North America Market Share 2025 | US Extended-Stay RevPAR | Dominant Brands | Key Driver |

| Largest regional share (Adagio/JLL 2025) | Above pre-pandemic benchmarks (JLL 2025) | Marriott Executive Apartments, Hyatt House, Oakwood | Technology, financial services, healthcare corporate mobility |

North America is the largest global aparthotel market, holding the largest regional market share in 2025 per Adagio operational disclosures and JLL Extended Stay Market Outlook, driven by a corporate travel infrastructure that generates multi-week extended project assignment demand across major US metros including New York, San Francisco, Chicago, Dallas, and Houston. JLL's US Select-Service and Extended-Stay Hotel Outlook 2025 confirmed that extended-stay formats have outperformed traditional lodging categories in the United States, with RevPAR levels exceeding pre-pandemic benchmarks, as disciplined supply additions sustained average daily rate levels. The American Hotel and Lodging Association's 2024 data confirmed business travel recovery generating sustained demand for hotels and aparthotels in downtown and near-airport locations, with 439 million sold room nights in 2023 establishing the baseline for the recovery cycle that continued through 2025. Marriott Executive Apartments, Hyatt House, and Oakwood Worldwide are the dominant branded aparthotel operators in North America, serving the corporate client base through long-term contracted rates and direct booking relationships with corporate travel management companies.

| European Pipeline to 2030 | ActivumSG Germany Portfolio | HospitalityNet Aug 2025 | Staycity UK Acquisitions |

| ~16,500 new rooms across branded operators | 550 keys, 9 cities, EUR 500M+ target by end-2025 | Serviced apartments outperforming hotels on resilience | Battersea, Oxford (2024-25), Nine Elms (2024) |

Europe is the region with the deepest institutional operator pipeline for branded aparthotels, with the European serviced apartment pipeline expected to add approximately 16,500 rooms by 2030 per GSAIR 2025, anchored by Adagio's 200-site national target across France and European expansion, Staycity's active UK development programme, and ActivumSG's assembly of nine German assets totalling 550 keys targeting EUR 500 million-plus by the end of 2025. Serviced apartments across Europe demonstrated stronger operational resilience than traditional hotels in 2025, with occupancy recovery supported by longer average lengths of stay and consistent weekday demand from corporate travellers per HospitalityNet analysis of August 2025, with the Italy serviced apartment market specifically benefiting from the return of international business travel alongside a rebound in long-stay leisure demand in commercial and tourism hubs per Accor Investor Day 2025 disclosures and JLL European Hospitality Market Overview. The European aparthotel market benefits from the structural cross-border corporate mobility of EU multinational employers whose employee assignment and project deployment requirements generate sustained multi-week aparthotel demand across capital cities and secondary financial and industrial centres.

| APAC New Projects Share | Frasers AI Partnership | Ascott Citadines Expansion | Key Growth Markets |

| ~38% of all upcoming branded serviced apt projects | Google Cloud AICTO programme, September 2025 | 4 new properties in Indonesia and Thailand, 2024 | Singapore, Tokyo, Mumbai, Bengaluru, Bangkok |

Asia Pacific holds the largest share of upcoming branded serviced apartment and aparthotel developments under construction globally at approximately 38% of all upcoming projects, driven by corporate travel demand across the region's major technology, financial services, and manufacturing business hubs and by the expansion of Global Capability Centre infrastructure in India and Southeast Asia. Frasers Hospitality adopted AI-driven workforce training in September 2025 through a partnership with Google Cloud's AI Cloud Takeoff programme, developing an AI agent application to streamline training across its Asia Pacific-focused portfolio that spans nearly 40 cities per company announcement of September 2025. Ascott Limited launched four new Citadines-branded properties in Indonesia and Thailand in 2024, adding 3,200 units to its Asia Pacific portfolio, and announced plans to open 20 new properties globally over the following four years with Asia Pacific markets as primary targets per Ascott company announcements of 2024. The region's aparthotel market benefits from the long-haul transit demand of Singapore Changi and Hong Kong International Airports, where branded aparthotel stays serve connecting passengers and short-assignment corporate visitors who require more space than a hotel room for stays of five to fourteen nights.