| TROVIEW INTELLIGENCE | Paris Extended-Stay and Serviced Apartment Market | Q2 2026 |

| TROVIEW INTELLIGENCE · CITY INTELLIGENCE REPORT |

Zone Profiles: La Defense · Central Business Districts (8e/16e/17e) · Left Bank and South · Northern Paris · Greater Paris West

Paris recorded an ADR within 2% year-on-year variance in the 2025 Global Serviced Apartment Industry Report alongside London and Amsterdam as the three most rate-stable serviced apartment markets in Europe, Adagio operates 41 aparthotels across Ile-de-France with three additional properties opening in 2026 and the brand targeting 200 sites by 2028, the Ile-de-France region accounted for 33.05% of the French hospitality market in 2025 making Paris the single most concentrated regional serviced apartment market in continental Europe, Lodgis manages over 10,000 corporate furnished apartments in Paris serving multinational corporations and relocation agencies seeking stays of one month to multiple years, corporate and business travellers account for nearly half of France market revenue with La Defense housing European headquarters of corporations generating the continent's most concentrated intra-company transfer and executive relocation demand, and the European Travel Commission's confirmation of an 11% increase in seven-to-twelve-night trips in 2025 positions Paris's leisure extended-stay segment as a structural growth complement to its corporate core.

| Standard License: USD 2,200 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

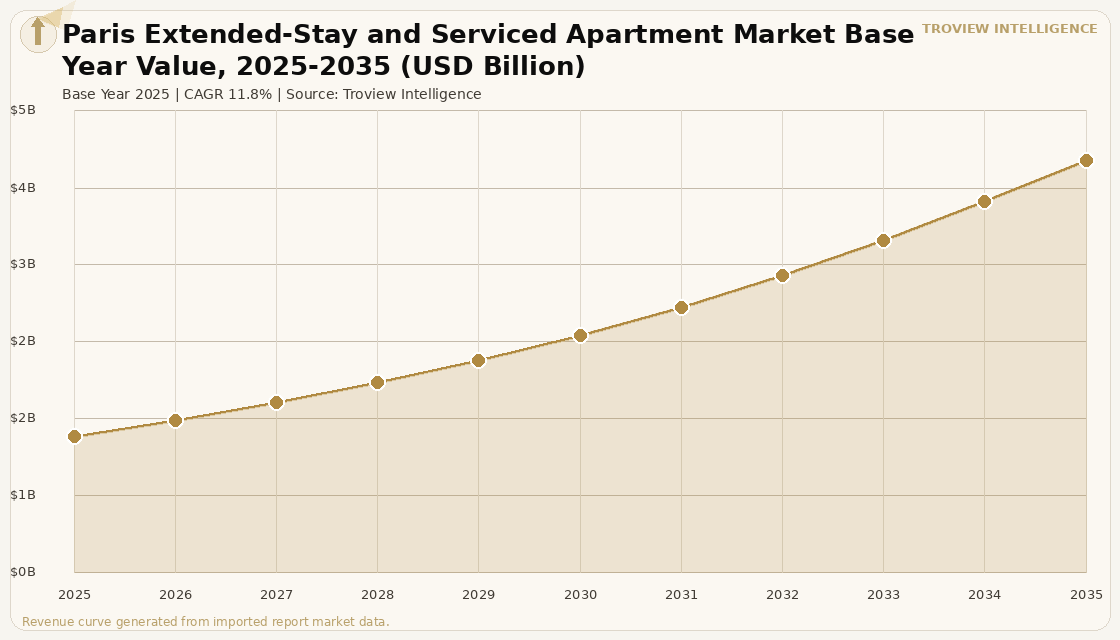

The Paris extended-stay and serviced apartment market size was USD 1.34 Billion in 2025 and is expected to register a revenue CAGR of 11.8% during the forecast period, reaching USD 4.06 Billion by 2035. The market encompasses institutionally managed, fully furnished serviced apartment properties and aparthotels operating across the Paris metropolitan area defined as inner Paris plus the La Defense-Nanterre-Issy-les-Moulineaux business corridor and the Ile-de-France suburban submarket serving corporate business travellers, expatriate professionals, diplomatic staff, international students, and leisure travellers on stays of seven nights and above. The Ile-de-France region accounted for 33.05% of the French hospitality market in 2025 per Adagio corporate investor communications and UNWTO France inbound tourism data, and serviced apartments recorded the fastest CAGR of any accommodation category in France through 2031, as brands including Adagio scale their Ile-de-France portfolio with three properties opening in 2026 across the western Paris and Greater Paris corridor. The 2025 GSAIR published by Ariosi and Travel Intelligence Network based on 1.6 million room night bookings through Habicus Group recorded that Paris, London, and Amsterdam maintained global ADR of GBP 145 with year-on-year variance below 2%, confirming Paris's position among the three most rate-stable and highest-performing serviced apartment markets in Europe. For instance, in February 2026, Adagio, France, opened the 132-unit Adagio Access Nanterre Aparthotel in La Defense, the ninth property developed in partnership with Sergic, with director of development Arthur Jaeger stating that the Nanterre opening demonstrates Adagio's commitment to strengthening its presence in the most dynamic regions and unlocking the full potential of existing sites in strategic locations close to La Defense and Greater Paris per Serviced Apartment News reporting of February 2026. These are some of the key factors driving revenue growth of the market.

Adagio operates 41 aparthotels across the Ile-de-France region comprising 21 Adagio Access and 20 Adagio Original properties, the largest branded serviced apartment portfolio in the Paris metropolitan market, with three additional Ile-de-France properties planned to open in 2026 and the brand pursuing a national target of 200 sites by 2028 per operator disclosure. Lodgis, France, manages over 10,000 corporate furnished apartments in Paris, offering the deepest single-operator corporate housing inventory in the market and serving multinational corporations, relocation agencies, and diplomatic missions whose extended-stay requirements range from one month to multiple years per Lodgis company information. La Defense, the central business district west of Paris housing European headquarters of corporations including Total, Societe Generale, LVMH, Capgemini, and dozens of international multinationals, generates the most concentrated intra-company transfer and executive relocation demand of any single business district in continental Europe, with the Adagio Access Nanterre opening in February 2026 directly adjacent to La Defense adding premium serviced apartment capacity to a submarket where existing supply has historically been undersupplied relative to corporate demand. The UN Tourism World Tourism Barometer recorded that Europe welcomed nearly 340 million international tourist arrivals in H1 2025, surpassing pre-pandemic levels, with France maintaining its position as the world's most visited country and Paris as the single most visited city, generating leisure extended-stay demand complementary to the corporate base from international visitors whose average stay duration is increasing per European Travel Commission data. These are some of the key factors driving revenue growth of the market.

However, the Paris extended-stay and serviced apartment market faces regulatory, competitive, and cost constraints that limit the pace of revenue growth and new supply development through the forecast period. The Paris municipal authority has implemented progressive restrictions on furnished short-term rental properties, including minimum stay requirements, mandatory registration obligations for furnished tourist accommodation, and restrictions on the number of nights per year that primary residences can be offered on short-term rental platforms, creating a compliance environment that, while beneficial to institutionally managed and planning-compliant serviced apartment operators, also increases planning and licensing complexity for new serviced apartment developments in arrondissements where the conversion of residential housing stock to tourist accommodation is actively resisted by the municipal planning authority. EirGrid-equivalent Paris grid capacity constraints affecting large-scale commercial real estate development in certain Ile-de-France zones limit the pace of new serviced apartment development in areas where energy capacity upgrades are required before new properties can be commissioned. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, create upward pressure on French electricity and gas prices, increasing the operating costs of full-service Paris serviced apartments whose kitchen, laundry, and climate control amenities generate above-average per-unit energy consumption relative to standard hotel rooms. The depth of professional short-term rental supply on Airbnb and Vrbo across Parisian arrondissements exerts pricing pressure on serviced apartment operators in the leisure extended-stay segment where platform algorithms respond more dynamically to real-time demand than institutionally managed serviced apartment revenue management can match. These factors substantially limit Paris extended-stay and serviced apartment market growth over the forecast period.

Paris has the rarest combination in real estate: a demand base that is simultaneously corporate and leisurec at genuine scale, in a single city, where both segments require accommodation above the standard hotel format. The corporate segment at La Defense is deterministic it grows every time a multinational moves its European headquarters west of the Seine, which has been happening continuously since the 1960s. The leisure segment is structural Paris is the most visited city on earth, and the visitors staying seven to twelve nights are not staying in hotels. They are staying in apartments, and the ones who choose branded, institutionally managed serviced apartments over Airbnb are making a deliberate choice about reliability, service, and accountability that Airbnb cannot replicate. Adagio understands this. Their 41 Ile-de-France properties are not competing with the Ritz. They are building the middle ground between the anonymous hotel room and the unpredictable short-term rental for a guest who needs to be in Paris for three weeks and wants their kitchen, their gym, their laundry, and their building concierge to work every day. That middle ground is structurally undersupplied in Paris and will remain so for the next decade." Troview Intelligence Head of Paris Extended-Stay and Serviced Apartment Research

SEGMENT INSIGHTS

| 03 | ZONE ANALYSIS |

Five Zones Defining Paris Extended-Stay and Serviced Apartment Geography

| Adagio Access Nanterre | Major Corporate Tenants | Transport | Demand Profile |

| 132 units opened Feb 2026, Sergic partnership | Total, Societe Generale, LVMH, Capgemini, Airbus | RER A, Metro Line 1, A86/A14 motorway access | Intra-company transfer, executive relocation, project deployment |

La Defense and the adjacent Nanterre corridor constitute Paris's primary corporate extended-stay and serviced apartment zone, hosting the European headquarters of France's largest corporations and dozens of international multinationals whose intra-company transfer, executive relocation, and project deployment programmes generate the continent's most concentrated corporate housing demand in a single business district. The February 2026 opening of Adagio Access Nanterre 132 units with family apartments, accessible units, 24/7 gym, self-service laundry, and bar directly adjacent to the La Defense financial and business tower district adds capacity to a submarket that has historically been supply-constrained relative to corporate demand per Adagio's own development rationale. La Defense hosts the headquarters of Total Energies, Societe Generale, LVMH, Capgemini, Airbus France, and dozens of international banks and professional services firms whose global mobility programmes generate sustained demand for serviced apartments at a quality level above standard hotel accommodation and at a cost efficiency for stays above fourteen nights that makes the corporate housing model financially rational for the employer as well as comfortable for the employee. The RER A line, Metro Line 1 Grande Arche terminus, and motorway access via the A86 and A14 make La Defense accessible from all Paris arrondissements and from Charles de Gaulle Airport within approximately 45 minutes, reducing the geographic constraint on serviced apartment site selection for employees based in the business district.

CENTRAL PARIS BUSINESS DISTRICTS (8e, 16e, 17e) PREMIUM CORPORATE AND DIPLOMATIC ZONE

| Operator Presence | Key Demand | Premium Premium | Lodgis Portfolio |

| Frasers (Fraser Suites Paris), Ascott (Citadines), Adagio | Financial services, luxury, diplomatic, OECD/UNESCO | Highest per-night rates in Paris serviced apartment market | 10,000+ corporate apartments across all Paris arrondissements |

The central Paris business districts of the 8th, 16th, and 17th arrondissements constitute the premium corporate and diplomatic extended-stay zone, hosting the primary Parisian addresses of international financial institutions, luxury goods corporations, law firms, and diplomatic missions whose executives and professional staff require the most premium serviced apartment product in the market at rates above the GBP 145 global average documented in the 2025 GSAIR. Frasers Hospitality's Fraser Suites Paris and Ascott's Citadines Paris properties in central arrondissements target the executive corporate and diplomatic segment requiring full hotel-grade services concierge, daily housekeeping, room service access combined with the privacy and space of a serviced apartment, at price points that compete with five-star hotel suite rates for stays above seven nights. The OECD and UNESCO headquarters in the 16th arrondissement generate sustained demand for serviced apartments from diplomatic staff, visiting delegations, and international organisation officials on six-month to two-year postings who require proximity to these institutional addresses. Lodgis's 10,000-plus corporate apartment portfolio spans all Paris arrondissements including the 8th, 16th, and 17th, providing corporate clients and relocation agencies with access to apartment-style accommodation in premium central locations that branded aparthotels cannot serve at equivalent apartment size and residential character.

LEFT BANK AND SOUTHERN PARIS (5e, 6e, 13e, 14e, 15e) ACADEMIC, STUDENT AND BLEISURE EXTENDED-STAY ZONE

| Key Demand Drivers | Adagio Presence | Bleisure Appeal | Average Stay Profile |

| Universities, HEI institutions, international students | Multiple Access and Original properties across 15e | Seine riverfront, Luxembourg Gardens, Latin Quarter | Longer academic and research institution stays 3-12 months |

The Left Bank and southern Paris arrondissements from the 5th to the 15th constitute Paris's academic and bleisure extended-stay zone, anchored by the Sorbonne university cluster, Sciences Po, Ecole Normale Superieure, and the concentration of research institutions and grandes ecoles whose international academic staff, visiting scholars, and enrolled postgraduate students generate demand for extended-stay accommodation across stay durations of three to twelve months. International students at Paris universities represent the fastest-growing extended-stay demand cohort in this zone, with France's government target to attract 500,000 international students annually by 2027 a policy set by the Choose France initiative directly driving demand for professionally managed furnished accommodation that provides the security, internet connectivity, and support services that incoming international students require. The Left Bank's cultural and leisure appeal the Luxembourg Gardens, the Latin Quarter, the Seine riverfront, and the concentration of cultural institutions makes the 5th and 6th arrondissements attractive for bleisure extended-stay guests combining professional Paris visits with longer leisure residence, generating above-average stay durations relative to the La Defense corporate zone.

NORTHERN PARIS AND GREATER PARIS EAST (18e, 19e, 20e, Saint-Denis) EMERGING AFFORDABLE EXTENDED-STAY AND OLYMPIC LEGACY ZONE

| Paris 2024 Olympics Legacy | Opportunity Profile | Target Tenant | Development Theme |

| Infrastructure investment, regeneration of Saint-Denis | Lower land cost, Metro extensions, emerging demand | International students, young professionals, project workers | New supply where inner Paris arrondissements are saturated |

Northern Paris and the Greater Paris East corridor including Saint-Denis, Saint-Ouen, and the 18th, 19th, and 20th arrondissements represent the emerging affordable extended-stay and serviced apartment development zone, energised by the infrastructure legacy of the Paris 2024 Olympic Games that upgraded transport links, public spaces, and commercial real estate quality across the northern Paris periphery. The Paris 2024 Olympic village in Saint-Denis, converted to residential and institutional use post-Games, brought new residential and hospitality real estate stock to an area that had historically attracted limited institutional accommodation investment, creating a development opportunity for extended-stay operators targeting cost-conscious corporate travellers, international students, and project-based workers who require Paris connectivity but cannot afford central arrondissement rates. Metro line extensions under the Grand Paris Express programme connecting northern Paris to La Defense, Charles de Gaulle Airport, and the southern business districts are reducing the transit time premium of northern Paris locations relative to inner central arrondissements, making serviced apartment developments in the 18th, 19th, and 20th arrondissements commercially viable for operators serving cost-sensitive corporate extended-stay demand.