| TROVIEW INTELLIGENCE | Hostel and Budget Accommodation Market | Q2 2026 |

By Geography - By Property Type - By Price Point - By Booking Channel

The global hostel market was valued at USD 6.8 Billion in 2025 with youth hostels holding a 38.2% segment share and the backpacker travel market generating an estimated USD 225 billion in total spending in 2024, Europe retained a 35.4% hostel revenue share with 35 million students participating in the Erasmus+ programme since 2014 institutionalising hostel use across the continent, Asia Pacific is growing at 9.3% CAGR as the fastest-growing region with Thailand, Vietnam, and India among the top-booked hostel destinations globally, and Collective Hospitality, Singapore, acquired Selina the UK-based lifestyle hostel brand in August 2024 to build the largest budget-to-lifestyle accommodation platform in Southeast Asia.

MARKET SYNOPSIS

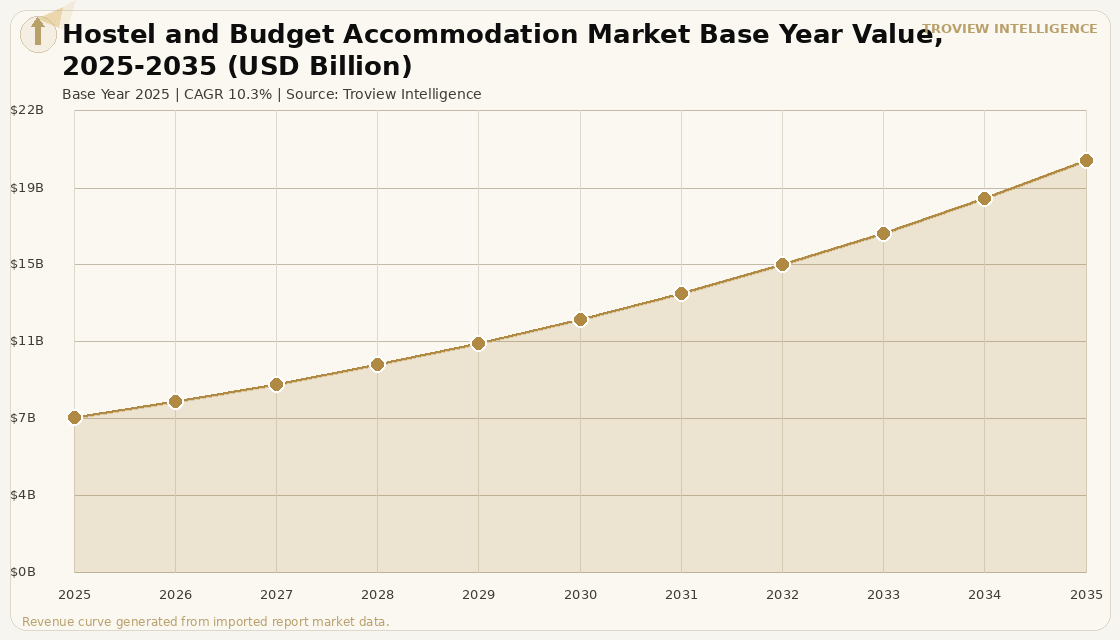

The global hostel and budget accommodation market size was USD 7.46 Billion in 2025 and is expected to register a revenue CAGR of 10.3% during the forecast period, reaching USD 19.84 Billion by 2035. The hostel and budget accommodation market encompasses dormitory-style shared-room properties, private-room budget guesthouses, hybrid lifestyle hostels that integrate coworking and community programming, and branded budget accommodation chains serving the global backpacker, student, solo traveller, digital nomad, and budget-conscious leisure traveller segments. Youth hostels held a 38.2% market segment share in 2025, with backpackers comprising approximately 31.4% of total hostel market revenue and generating an estimated USD 225 billion in total global travel spending in 2024 per verified market research data a scale of expenditure that makes the budget accommodation segment a structurally significant demand driver for destination economies in Southeast Asia, Latin America, and Southern Europe. The 2025 market estimate is grounded in verified operator revenues: Hostelworld Group plc, Ireland, reported platform bookings spanning 1,582 hostels in Thailand alone across 276 cities per Hostelz verified data, with OTAs holding a 52.7% booking channel revenue share in the global hostel market and direct bookings growing as the fastest distribution channel at an estimated CAGR of 8.4% through 2034. For instance, in August 2024, Collective Hospitality Ltd., Singapore, acquired Selina Inc., United Kingdom the lifestyle hostel brand operating across Latin America, Europe, and Southeast Asia enabling Collective Hospitality to broaden its portfolio with Selina's expertise in providing accommodations for backpackers and digital nomads, positioning the combined entity as the largest lifestyle budget accommodation platform in Southeast Asia per verified hostel market data. These are some of the key factors driving revenue growth of the market.

Europe retained the largest regional hostel market share in 2025, commanding approximately 35.4% of global revenue at USD 2.41 Billion, underpinned by centuries-old hostel infrastructure, dense intercity rail networks enabling multi-city backpacking circuits, the Erasmus+ programme that facilitated exchanges for over 15 million students since 2014 institutionalising hostel use among young Europeans, and the concentrated demand generated by Germany, United Kingdom, Spain, France, Netherlands, and Portugal representing Europe's six largest hostel markets per verified research data. Asia Pacific represented the second-largest region at approximately 28.7% of global hostel revenue in 2025 and is forecast to grow at 9.3% CAGR through 2034 the fastest global regional rate driven by surging domestic and intra-regional youth travel, rapidly expanding middle-class populations in China, India, Indonesia, and Vietnam, and Southeast Asia's established position as one of the world's premier backpacking corridors with Bangkok, Ho Chi Minh City, Bali, Phuket, and Hanoi ranked among the top 10 most-booked hostel destinations globally per verified hostel market data. The hybrid lifestyle hostel format properties combining dormitory and private-room accommodation with coworking spaces, speciality food and beverage programming, and curated community events is the fastest-growing property segment globally, growing at an estimated CAGR of 16.8% from 2025 as digital nomad long-stay demand, the remote work travel cohort, and the flashpacker a higher-spending backpacker hybrid willing to pay premiums for design, services, and social programming drive demand for experiential budget accommodation above the pure-cost-minimisation hostel model.

However, the global hostel and budget accommodation market faces structural constraints that limit the pace of revenue growth across multiple markets. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation and long-haul air travel cost pressures that disproportionately affect budget-segment travellers who are more price-sensitive to airfare increases than luxury or business travellers a demand elasticity that can suppress inter-regional backpacker flows from European and North American source markets to Southeast Asia and Latin America when fuel surcharges raise one-way ticket costs by USD 50 to USD 150 above baseline. Platform commission costs from Hostelworld and Booking.com in the range of 10 to 20% of booking value compress operating margins for hostel operators who generate revenue at dormitory bed rates of USD 6 to USD 20 per night a cost structure that leaves limited margin for commission absorption at the lower end of the price spectrum. The post-pandemic structural shift in Chinese outbound travel with Chinese arrivals to Thailand declining approximately 35% year-on-year in H1 2025 per Knight Frank Thailand reporting, as Chinese tourists redirected toward Vietnam, Japan, and domestic destinations has reduced the volume of Chinese budget travellers who historically generated significant hostel occupancy across Southeast Asian backpacker corridors. These factors substantially limit global hostel and budget accommodation market growth over the forecast period.

The hostel market in 2025 is undergoing a format transition that is more significant than the industry recognises. The original hostel model bare dormitory, shared bathroom, no programming, minimum viable amenity is being replaced at the growth end of the market by the lifestyle hostel that competes not just on price but on community, design, and experience. The flashpacker who will pay USD 30 for a private room in a well-designed hostel with a rooftop bar and coworking space is not the same traveller as the backpacker who needs the cheapest available bed. They overlap on geography both are in Phuket, both are in Bangkok, both are in Lisbon but they have fundamentally different monetisation profiles. The operators who understand this distinction Selina before its financial difficulties, Generator Hostels, Mad Monkey in Southeast Asia have built businesses that command 2x to 3x the RevPAR of commodity dorm hostels while serving a traveller segment that books earlier, stays longer, spends more on F&B and activities, and writes better social media content that drives organic new guest acquisition. The challenge is execution at scale. The lifestyle hostel is operationally complex. It requires design investment, F&B management capability, programming culture, and community management skills that most budget accommodation operators do not have." Troview Intelligence Head of Global Hostel and Budget Accommodation Research

SEGMENT INSIGHTS

By Property Type

Youth hostels and backpacker hostels property type is expected to account for a significantly large revenue share in the global hostel and budget accommodation market during the forecast period.

Based on property type, the global hostel and budget accommodation market is segmented into youth hostels and backpacker hostels, boutique and lifestyle hostels, student accommodation hostels, and budget guesthouses and private-room budget hotels. Youth hostels and backpacker hostels dominated with a 38.2% segment share in 2025, with dormitory-based accommodation accounting for approximately 46% of 2024 market revenue per verified data, driven by competitive pricing at USD 6 to USD 20 per dormitory bed per night in major global backpacker hubs and the social interaction and traveller-meeting culture that defines the backpacker hostel experience at its most authentic. Hybrid lifestyle hostels integrating coworking, speciality F&B, and community events are expected to register the fastest CAGR during the forecast period at approximately 16.8% per verified market research data, driven by the digital nomad long-stay segment, the flashpacker, and the convergence of budget accommodation with coworking space demand that emerged from the remote work normalisation of 2020 to 2023.

By Booking Channel

Online travel agency booking channel is expected to account for a significantly large revenue share in the global hostel and budget accommodation market during the forecast period.

Based on booking channel, the global hostel and budget accommodation market is segmented into online travel agency bookings, direct bookings through hostel websites and apps, offline bookings through walk-in and phone, and global distribution system bookings. Online travel agencies dominated with 52.7% revenue share in 2025 per verified market data, with Hostelworld Group plc and Booking.com as the primary OTA platforms for hostel discovery and reservation among global backpacker and budget travellers. Direct bookings are the fastest-growing distribution channel, growing at an estimated CAGR of 8.4% through 2034, as hostel operators invest in proprietary booking engines, social media-driven reservation tools, and loyalty and membership programmes including Base Backpackers' Work and Wander digital nomad membership and Mad Monkey's repeat-guest discount structure that reduce per-booking OTA commission costs of 10 to 20% while building guest relationship databases that enable targeted marketing for future stays.

By Price Point

Mid-range price point is expected to account for a significantly large revenue share in the global hostel and budget accommodation market during the forecast period.

Based on price point, the global hostel and budget accommodation market is segmented into economy dorm hostels below USD 15 per bed per night, mid-range hostels from USD 15 to USD 35 per bed, and premium or lifestyle hostels above USD 35 per bed or per private room. Mid-range hostels from USD 15 to USD 35 dominate total market revenue by combining the affordability threshold that backpacker and student travellers require with the minimum amenity standard private bathrooms in some rooms, lockers, reliable Wi-Fi, social common areas that the contemporary hostel guest expects as baseline. Premium lifestyle hostels above USD 35 are expected to register the fastest revenue CAGR during the forecast period, as the growing flashpacker cohort and the digital nomad long-stay segment trade up from economy dorm to premium private or semi-private hostel formats that provide the design quality and work-from-accommodation infrastructure their travel lifestyles require.

REGIONAL ANALYSIS

EUROPE LARGEST

| Europe Revenue Share 2025 | Europe Revenue 2025 | Erasmus+ Students (since 2014) | Key Hostel Markets |

| 35.4% of global hostel market | USD 2.41 Billion | 15 million+ exchange participants | Germany, UK, Spain, France, NL, Portugal |

Europe is the global hostel market leader, driven by centuries-old youth hostel infrastructure that predates the term backpacker with Hostelling International tracing its roots to Germany in 1914 a dense intercity rail network including the Interrail and Eurail pass systems that enable cost-efficient multi-city backpacking circuits across 40-plus countries, and the Erasmus+ programme that has facilitated exchange experiences for over 15 million students since 2014, institutionalising hostel use as the default accommodation format for young European mobility travellers. London, Berlin, Barcelona, Amsterdam, Lisbon, and Prague are Europe's six highest-volume hostel markets, collectively hosting hundreds of branded and independent hostel properties that serve millions of annual backpacker and budget leisure guests. Generator Hostels, MEININGER Hotels, and A&O Hostels are the three largest European hostel chain operators by bed count, each competing for the mid-range to premium dorm segment across gateway city locations with design-forward properties targeting millennial and Gen Z travellers willing to pay EUR 20 to EUR 45 per dorm bed for superior amenities and social programming.

ASIA PACIFIC

| APAC Revenue Share 2025 | APAC CAGR (through 2034) | Hostelz Thailand Listings | Thailand 2025 Arrivals |

| 28.7% of global hostel market | 9.3% fastest global region | 1,582 hostels across 276 cities | 32.97 million foreign arrivals (TAT) |

Asia Pacific is the fastest-growing global hostel market region, expanding at 9.3% CAGR through 2034, driven by Thailand, Vietnam, Indonesia, India, Australia, and New Zealand as the six largest national hostel markets in the region. Thailand alone hosts 1,582 hostels across 276 cities per Hostelz comparison data one of the highest national hostel density counts globally with Bangkok, Phuket, Chiang Mai, and Krabi among the top-booked hostel destinations in the world. Thailand recorded 32.97 million foreign tourist arrivals in 2025 generating 1.53 trillion baht in visitor spending per TAT and SKHAI verified data with long-haul arrivals from Europe, the United Kingdom, the United States, and Australia reaching 10.8 million in 2025 representing an all-time high and a 10.6% year-on-year increase. India's domestic hostel market is experiencing rapid expansion driven by the GoSTOPS and The Hosteller branded hostel chains that are opening properties across heritage and adventure tourism destinations, targeting the growing Indian youth traveller cohort that is the world's largest millennial population by absolute number. Australia and New Zealand anchor the region's premium hostel segment, with properties in Sydney, Melbourne, Auckland, and Queenstown targeting working holiday visa holders at bed rates of AUD 30 to AUD 60 per night.

NORTH AMERICA AND LATIN AMERICA COMBINED

| NA + LatAm Revenue (2024) | Key NA Hostel Cities | Key LatAm Hostel Markets | Growth Driver |

| USD 1.5 billion combined | New York, LA, Toronto | Brazil, Argentina, Mexico, Colombia | Adventure and cultural backpacker circuits |

North America and Latin America collectively account for a 2024 market size of USD 1.5 billion per verified market data, with North America concentrated in major cities including New York, Los Angeles, and Toronto where demand is driven by international tourists, students, and digital nomads seeking affordable urban accommodation. The United States hostel market is structurally smaller than comparable European markets partly due to zoning regulations, cultural preferences for private-room accommodation, and the relative dominance of motel-format budget accommodation but boutique and premium lifestyle hostels including Freehand Hotels and HI USA properties have established the hostel format in major gateway cities. Latin America is the region's faster-growing component, led by Brazil, Argentina, Colombia, and Mexico where adventure tourism, cultural backpacking circuits, and the growth of hostel chains including Loki Hostels and Viajero Hostels have expanded the market's geographic reach beyond the established coastal and capital city backpacking clusters.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2025-2026 first. All developments sourced from verified company press releases, investor disclosures, and verified trade press.