| TROVIEW INTELLIGENCE | Rome Aparthotel Market | Q2 2026 |

| TROVIEW INTELLIGENCE · CITY INTELLIGENCE REPORT |

By Zone · By Stay Duration · By End-User Segment · By Operator Type

Zone Profiles: Vatican and Prati · Centro Storico · EUR and Ostiense · Nomentano and Parioli · Trastevere and South

Rome catalysed EUR 630 million of Italian hotel investment in H1 2025, approximately 37% of the national total per Il Sole 24 Ore February 2026 reporting, with the city recording an average occupancy rate of 70%, an ADR of EUR 228, and a RevPAR of EUR 158 per available room that grew 3% year-on-year in H1 2025, recording hotel investment of EUR 465 million in full-year 2024 that ranked it first among Italian cities per the EY Italy Hotel Investment Report 2024, opening Orient Express La Minerva with 93 rooms, Romeo Roma designed by Zaha Hadid Architects with 74 rooms, and The Social Hub Rome with 392 rooms in H1 2025, and being inundated with tourists throughout 2025 due to the Jubilee of the Catholic Church which occurs every 25 years and the death of Pope Francis, with Adagio operating its Rome Vatican aparthotel in the Balduina area with 119 apartments, and Mandarin Oriental, Four Seasons, and Rosewood expected to open in Rome in the near term, confirming that Rome is Italy's primary hospitality investment market and the European city with the most sustained structural demand growth for apartment-format accommodation.

| Standard License: USD 2,200 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

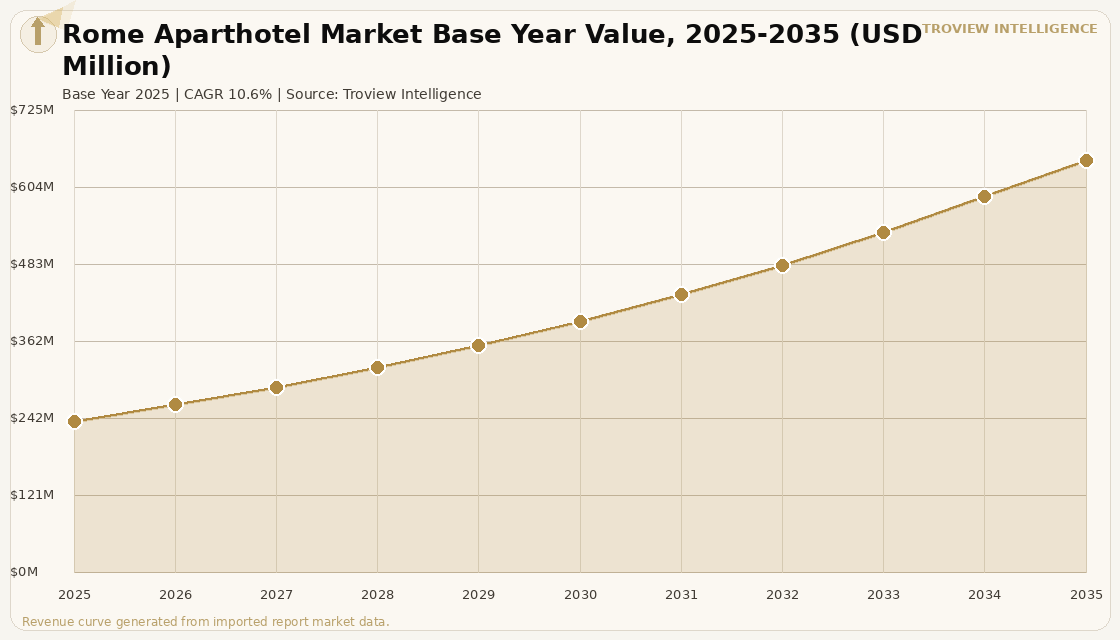

The Rome aparthotel market size was USD 238.4 Million in 2025 and is expected to register a revenue CAGR of 10.6% during the forecast period, reaching USD 647.2 Million by 2035. The market encompasses branded and operator-managed aparthotel properties across the Rome metropolitan area, including the Vatican, Prati, Centro Storico, Trastevere, EUR, Nomentano, and Parioli zones, serving international leisure and pilgrimage visitors, corporate travellers attending Rome's growing MICE sector, diplomatic and government guests, and long-stay academic and cultural research visitors. Rome's hotel investment environment delivered EUR 465 million in 2024 ranking first among Italian cities and EUR 630 million in H1 2025 alone, approximately 37% of the Italian national total per Il Sole 24 Ore reporting of February 2026, confirming the city's status as Italy's primary hospitality capital investment destination. The city's average occupancy rate of 70% with an ADR of EUR 228 and a RevPAR of EUR 158 per available room in H1 2025, growing 3% year-on-year per Cushman and Wakefield Hotel Market Beat Italy H1 2025, establishes the demand foundation that justifies premium aparthotel positioning in Rome's most sought-after zones. Rome was inundated with tourists throughout 2025 due to the Catholic Church's Jubilee Year which occurs every 25 years and draws tens of millions of pilgrims and cultural visitors to the city and the additional demand generated by the death of Pope Francis, creating accommodation pressure that conventional hotel inventory alone was unable to absorb and generating sustained demand for aparthotel formats that can serve families, pilgrimage groups, and extended-stay visitors more flexibly than standard hotel rooms. For instance, in 2025, Adagio, France, operates the Adagio Access Rome Vatican aparthotel in the Balduina area near the Vatican, with 119 apartments ranging from studios for two to two-room units for four, each equipped with kitchen, living area, Wi-Fi, and air conditioning, a seasonal outdoor pool, laundry facilities, and private parking, serving as the primary branded international aparthotel reference point for the Vatican and pilgrimage demand zone in Rome per Adagio company information. These are some of the key factors driving revenue growth of the market.

The Rome hotel market attracted notable property investment transactions in H1 2025 including the EUR 170 million acquisition of the Mandarin Oriental at Villini Sallustiani, and saw significant new openings including Orient Express La Minerva with 93 rooms, Romeo Roma designed by Zaha Hadid Architects with 74 rooms in the Navona district, and The Social Hub Rome with 392 rooms the latter an innovative hybrid accommodation format combining hotel rooms, long-stay accommodation, and co-working space that directly targets the extended-stay and student demographic that overlaps with the aparthotel format's core market per Cushman and Wakefield Hotel Market Beat Italy H1 2025. Further luxury hotel openings planned for the near term include Mandarin Oriental's forthcoming property, Four Seasons Roma, and Rosewood Rome, all of which will add premium accommodation capacity to a Rome hospitality market that remains a seller's market even at the Jubilee-elevated demand levels of 2025 per Italian Hotel Investment Conference analysis. The broader Italian hotel sector performed well in H1 2025 with RevPAR up 3% year-on-year at the national level, and Rome specifically benefited from the Jubilee tourism wave that CoStar confirmed in September 2025 inundated the city, generating above-average demand across all accommodation categories and allowing aparthotel operators to maintain occupancy above the city's 70% average. These are some of the key factors driving revenue growth of the market.

However, the Rome aparthotel market faces regulatory, competitive, and operational constraints that temper revenue growth through the forecast period. Rome's planning environment for new tourist accommodation in the historic centre and traditional residential quartieri is complex, with the Comune di Roma Capitale maintaining planning restrictions on the conversion of residential housing stock to tourist accommodation that limit the pipeline of new aparthotel supply in the most central and high-demand zones, and the Italian national government's short-term rental registration requirements adding compliance layers for operators developing new apartment-format hospitality properties. The pipeline of luxury hotel openings in Rome Mandarin Oriental, Four Seasons, Rosewood, and others planned for the near term creates new competitive pressure in the upper-upscale and luxury segment that overlaps with premium aparthotel positioning, as international luxury travellers choosing between a Four Seasons room and a luxury aparthotel unit will weigh the brand recognition and full-service amenity of the luxury hotel against the greater space and kitchen access of the aparthotel. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, create upward pressure on Italian electricity and gas costs, increasing the operating expense of Rome's full-service aparthotels whose kitchen, laundry, and climate control amenities for Mediterranean summer tourists generate above-average energy consumption per unit from April through October. These factors substantially limit Rome aparthotel market growth over the forecast period.

Rome's aparthotel market in 2025 is being defined by an event that happens once every 25 years and that no Italian hotel or aparthotel operator planned for at the scale at which it arrived. The Catholic Jubilee draws tens of millions of pilgrims over its duration, and those pilgrims are not the same as the leisure tourist who books eight months ahead on Booking.com. The pilgrim is often part of a parish group from Brazil or the Philippines or Germany. The group needs five rooms that are near the Vatican, are available for ten nights, have somewhere to prepare breakfast, and are not going to charge EUR 228 per room. The Adagio Rome Vatican aparthotel in the Balduina area, with 119 apartments from studios to two-room units, exists at the intersection of every one of those requirements. The problem is that there is only one of it, and it has 119 apartments. Rome needs more of them, and the investment case for building or converting an aparthotel in the Prati neighbourhood or the Balduina-Vatican corridor has never been stronger than it is in 2025. The city is drawing tens of millions of visitors, hotels cannot build their way to 70% of a Four Seasons in the time it takes to read this report, and the most flexible accommodation format for groups, families, and extended stays is the one that is most undersupplied." Troview Intelligence Head of Rome Aparthotel Research

SEGMENT INSIGHTS

| 03 | ZONE ANALYSIS |

Five Zones Defining Rome's Aparthotel Geography

| Primary Demand | Adagio Rome Vatican | Catchment | Key Features |

| Catholic Jubilee pilgrims, Vatican museum visitors, faith groups | 119 apartments, Balduina area, studios to 2-room units | Walking distance Vatican City, Sistine Chapel, St Peter's | Full kitchen, seasonal pool, laundry, private parking |

The Vatican and Prati zone is the primary aparthotel demand generator in Rome, anchored by the Catholic Church's extraordinary draw on international visitors which in Jubilee 2025 reached extraordinary proportions as tens of millions of pilgrims travelled to Rome from across the globe and by the residential character of the Prati and Balduina neighbourhoods immediately adjacent to Vatican City that make them the most sought-after locations for multi-night stays combining Vatican access with a residential neighbourhood experience rather than a tourist centre hotel environment. Adagio operates the Adagio Access Rome Vatican aparthotel in the Balduina area, the only branded international aparthotel operator with a dedicated Rome Vatican-zone property, with 119 apartments ranging from studios for two to two-room units for four, each equipped with kitchen, living area, Wi-Fi, and air conditioning, a seasonal outdoor pool, laundry facilities, and private parking per Adagio company information. The Jubilee 2025 demand surge and the death of Pope Francis which added to the extraordinary global Catholic attention on Rome throughout the year created occupancy conditions at the Adagio Rome Vatican that illustrate the structural demand case for additional branded aparthotel supply in this zone, as the combination of multi-night stays, family and group compositions, and cost-consciousness that characterises the pilgrim traveller maps directly onto the aparthotel format's operational strengths relative to the comparable hotel room.

| ADR Range | Key Opening 2025 | Investment Pipeline | Aparthotel Challenge |

| EUR 228+ average; premium historic centre properties higher | Romeo Roma (74 rooms, Zaha Hadid, Navona district) | Mandarin Oriental, Four Seasons, Rosewood openings pending | Heritage planning restrictions limit new supply conversion |

The Centro Storico and Navona district constitute Rome's highest-demand and highest-ADR zone, encompassing the Pantheon, Campo de' Fiori, Piazza Navona, and the medieval and Renaissance streetscape that defines the archetypal Rome experience for international leisure visitors, with the zone recording premium ADR levels above the city's EUR 228 average as the scarcity of accommodation supply within walking distance of these sites commands a location premium from visitors unwilling to travel more than fifteen minutes on foot to Rome's most celebrated streets. The H1 2025 opening of Romeo Roma 74 rooms designed by Zaha Hadid Architects in the Navona district and the pending openings of Mandarin Oriental, Four Seasons Roma, and Rosewood Rome confirm that the Centro Storico zone is attracting the most ambitious luxury hotel developments in Italy, creating a competitive environment that the aparthotel format must differentiate against through space advantage, kitchen provision, and local neighbourhood authenticity rather than brand luxury. Heritage planning restrictions on new tourist accommodation construction in the historic centre limit the pipeline of new branded aparthotel supply, making converted palace and civic building projects the primary development pathway for aparthotel operators who want a Centro Storico address.

| Key Infrastructure | Corporate Demand | Transport | Apartment Stock |

| EUR Convention Centre, Palazzo dei Congressi, FAO HQ | Government ministries, UN agencies, corporate MICE | Metro B (EUR Palasport, EUR Fermi), Fiumicino 25 min | Largest purpose-built corporate apartment corridor in Rome |

The EUR and Ostiense zone in south-central Rome is the city's primary corporate, conference, and institutional accommodation corridor, anchored by the EUR convention district that hosts the Palazzo dei Congressi, the EUR Convention Centre, and the headquarters of multiple UN Food and Agriculture Organization agencies and Italian government ministries, generating a conference, diplomatic, and institutional demand base that is fundamentally different from the pilgrimage and leisure demand of the Vatican and Centro Storico zones. The FAO headquarters and the concentration of multilateral institution offices in the EUR district generate sustained demand from visiting international delegates and official delegations on stays of five to twenty-one nights who require the apartment-format's combination of meeting-adjacent accommodation, kitchen facilities for self-catering, and residential privacy that makes the EUR zone the most logical location for purpose-built corporate aparthotel development in Rome. The zone's modern rational street layout built during the 1930s and 1940s as Mussolini's planned urban extension provides the building floor plates and site dimensions that are architecturally difficult to find in the historic centre, making EUR the easiest location in Rome for new-build or large-scale conversion aparthotel development for operators willing to accept the ten-minute metro or taxi transfer to the central tourism sites.

| Neighbourhood Character | Appeal to Extended Stay | Demand Profile | Aparthotel Opportunity |

| Authentic Roman residential, food market culture | Artisan market, restaurants, local experience immersion | Food tourism, cultural immersion, digital nomad, US students | Growing demand, limited branded supply gap market |

Trastevere and Testaccio represent Rome's most authentic residential neighbourhood zones and the fastest-growing non-centro destinations for international extended-stay visitors who prefer to experience the city as residents rather than tourists, with Trastevere's cobblestone streets, local trattorias, and open-air evening culture and Testaccio's wholesale food market, artisan workshops, and Roman culinary heritage creating the lived-experience environment that motivates seven-to-twenty-one-night stays from US students on semester programmes, digital nomads working remotely, and food and cultural tourism travellers who are not constrained by a conference agenda. The social media-driven visibility of Trastevere and Testaccio among international millennial and Gen Z travellers who research Rome through Instagram food content and cultural neighbourhood guides rather than traditional tourism platforms creates demand for residential-feeling accommodation in these neighbourhoods that the existing conventional hotel supply, concentrated in the centro storico and near the major monuments, cannot serve. The zone represents the most significant branded aparthotel development gap in Rome, as the residential character that makes these neighbourhoods attractive to extended-stay visitors is precisely the environment that a well-designed branded aparthotel can replicate at institutional quality, with kitchen, laundry, and communal living space that allows visitors to shop at the Testaccio market and cook their own pasta rather than eating every meal at a restaurant.

NOMENTANO, PARIOLI AND NORTHERN ROME RESIDENTIAL, DIPLOMATIC AND ACADEMIC LONG-STAY ZONE

| Primary Demand | Key Infrastructure | Stay Duration | Aparthotel Appeal |

| Diplomats, embassy staff, academic visitors, medical tourism | Foreign embassies, Villa Borghese, Sapienza university | Long-stay above 21 nights dominant in this zone | Residential scale, school proximity, quiet environment |

Nomentano, Parioli, and northern Rome constitute the city's primary residential long-stay zone for diplomatic staff, embassy secondees, academic visiting professors, and medical tourism patients who require accommodation for stays of one month to multiple years rather than the week-to-three-week range of the centro storico or Vatican zones. The concentration of foreign embassies along the Villa Borghese and Parioli corridors generates sustained demand for fully furnished apartment accommodation from embassy staff on posting cycles of six to thirty-six months who require proximity to their diplomatic facilities, access to international schools, and residential accommodation that functions as a home rather than a hotel. Sapienza University of Rome, one of Europe's largest universities with approximately 105,000 students, generates demand for visiting academic accommodation in its northern campus catchment, with international professors and research fellows on sabbatical or short-term academic appointments requiring three-to-twelve-month furnished apartment access at an institutional management quality that the private furnished rental market cannot guarantee. The aparthotel format's combination of managed housekeeping, reliable maintenance, and institutional billing capability makes it particularly well-suited to this diplomatic and academic long-stay zone, where the operator's ability to provide monthly billing, contract management, and move-in and move-out flexibility is more important than Colosseum proximity.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from verified company announcements, Cushman and Wakefield Hotel Market Beat Italy reports, and verified trade press.