| TROVIEW INTELLIGENCE | Italy Aparthotel Market | Q2 2026 |

| TROVIEW INTELLIGENCE · COUNTRY INTELLIGENCE REPORT |

By City · By Stay Duration · By End-User Segment · By Brand Tier

Italy ranked third in Europe and fifth globally with 64.5 million tourists in 2024 per the World Population Review, Italian hotel investment reached EUR 2.1 billion in 2024 the second highest volume on record and 30% above the decade-long average per the EY Italy Hotel Investment Report 2024 Italian hotel investment for H1 2025 alone nearly doubled year-on-year to EUR 1.7 billion with Rome and Venice generating EUR 780 million or 47% of national volume, RevPAR across Italy's hospitality sector grew 3% in H1 2025 with ADR up 2% and Rome RevPAR growing 3% while Milan outperformed at 5%, Starhotels Group president Elisabetta Fabri confirmed at the 2025 Italian Hotel Investment Conference that her company's serviced apartment properties in Milan and Florence receive significant market attention, and Rome was inundated with tourists in 2025 due to the Jubilee of the Catholic Church which occurs every 25 years and the death of Pope Francis, confirming Italy as the European aparthotel market with the most concentrated tourism-driven demand growth and the highest institutional investor appetite of any European hospitality market in 2025.

| Standard License: USD 6,500 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

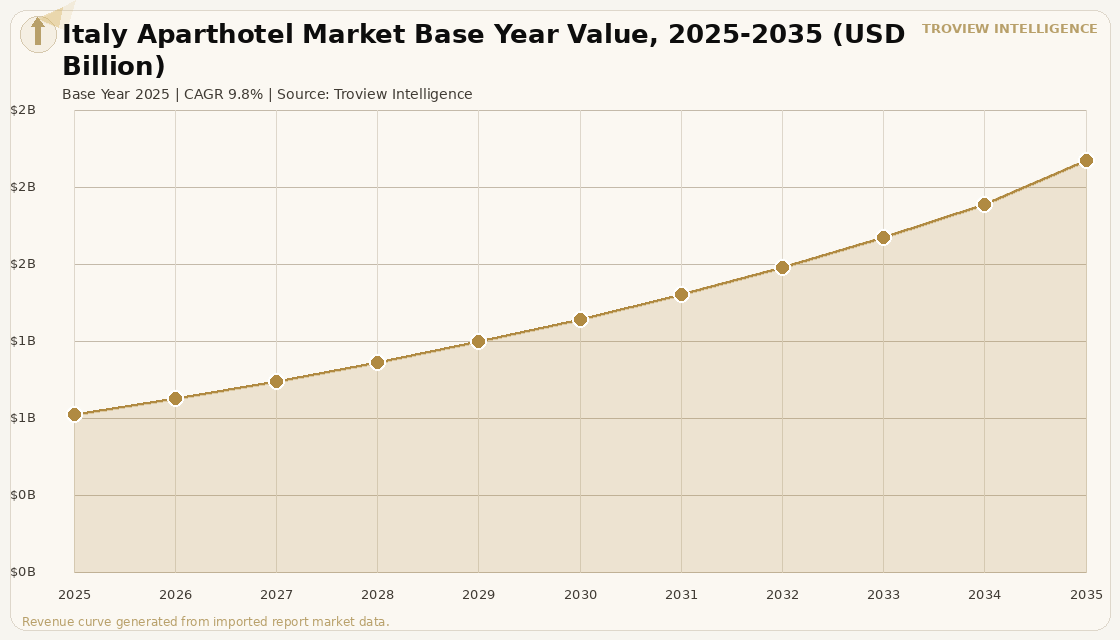

The Italy aparthotel market size was USD 824.6 Million in 2025 and is expected to register a revenue CAGR of 9.8% during the forecast period, reaching USD 2.14 Billion by 2035. Market revenue growth is supported by Italy's structural position as one of Europe's most visited countries ranking third in Europe and fifth globally with 64.5 million tourists in 2024 per the World Population Review and by an investment environment in its hospitality sector that has dramatically outperformed broader European markets, with Italian hotel investment reaching EUR 2.1 billion in 2024, the second highest volume on record and 30% above the decade-long average of EUR 1.65 billion per the EY Italy Hotel Investment Report 2024. The Italy serviced apartment market has specifically benefited from the return of international business travel alongside a rebound in long-stay leisure demand in major commercial and tourism hubs including Rome, Milan, Florence, and Venice, with the sector demonstrating stronger operational resilience than traditional hotels per HospitalityNet data of August 2025 and Accor Investor Day 2025 European operational disclosures. Italy's hospitality sector performed well in H1 2025 with RevPAR up 3% year-on-year, driven by a 2% ADR increase and a 1% rise in occupancy, with Rome's RevPAR growing 3% in H1 2025 and Milan outperforming with a 5% RevPAR increase per Cushman and Wakefield and Colliers Hotel Market Beat Italy H1 2025. For instance, in 2025, Starhotels Group, Italy, confirmed at the Italian Hotel Investment Conference that the company's two serviced apartment properties in Milan and Florence receive significant market attention, with Starhotels president and CEO Elisabetta Fabri stating that this property type demonstrates growing demand for apartment-format hospitality among the international business and leisure travellers choosing Italy as their destination, confirming institutional Italian hospitality operator recognition of the aparthotel format's demand depth per CoStar reporting of September 2025. These are some of the key factors driving revenue growth of the market.

Italian hotel investment in H1 2025 reached nearly EUR 1.7 billion, more than double the H1 2024 volume, with Rome and Venice generating EUR 780 million combined approximately 47% of national volume and notable individual transactions including the EUR 170 million acquisition of the Mandarin Oriental in Rome at the Villini Sallustiani per Cushman and Wakefield Hotel Market Beat Italy H1 2025 reporting. Italy's hospitality real estate assets were valued at approximately EUR 160 billion in 2024, an 11% increase from 2023, with hotel assets comprising EUR 133 billion of that total per Tourism Review analysis of July 2025, and the forecast for 2025 indicating a 9% increase in real estate turnover to EUR 3.7 billion, surpassing pre-2019 levels. ADR growth in Italy of 4% in 2024 ranked among the highest in Europe per EY and hospitality market analysis, with medium and high-end hotels in cities including Bologna, Florence, Milan, Rome, and Venice achieving occupancy rates above 75% in 2024 and Bologna and Milan approaching 80% in 2025, confirming the depth of demand supporting premium apartment-hotel formats in Italy's most active hotel investment cities. The 2025 Jubilee Year of the Catholic Church, which occurs every 25 years, generated extraordinary demand for accommodation in Rome from Catholic pilgrims, international tourists, and faith-based group travellers in volumes that the city's conventional hotel inventory was challenged to absorb, creating overflow demand for aparthotel and serviced apartment alternatives that could accommodate families, groups, and extended-stay pilgrims more flexibly than standard hotel rooms. These are some of the key factors driving revenue growth of the market.

However, the Italy aparthotel market faces structural constraints that temper the pace of revenue growth and new supply development through the forecast period. Italy's hospitality property market is characterised by fragmented individual ownership, with many of the highest-quality historic properties held by family estates, religious orders, and heritage foundations whose decision-making timelines and return requirements are incompatible with the speed of conversion and repositioning that international aparthotel operators require to deploy capital efficiently, creating a structural constraint on the quality and volume of new aparthotel supply in Italy's most in-demand urban markets. Rome in particular faces the risk of market oversaturation in the conventional hotel segment as multiple high-end hotel projects including Mandarin Oriental, Four Seasons, and Rosewood are expected to open in the near term, creating competitive pressure that could spill over into the premium aparthotel segment as a growing branded hotel supply competes for the same high-value international traveller. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, create upward pressure on Italian electricity and gas prices, increasing operating costs for Italy's aparthotel operators whose full kitchen, laundry, and climate control amenities generate above-average per-unit energy consumption. Regulatory complexity for licensed tourist accommodation in Italy's major historic centres including Rome's short-term rental caps, Florence's restrictions on new tourist accommodation in the historic centre, and Venice's day-visitor fees increases compliance costs for aparthotel operators and may constrain the expansion of apartment-format hospitality in the city centres where tourism demand is highest. These factors substantially limit Italy aparthotel market growth over the forecast period.

Italy's aparthotel market has a fundamental demand advantage that most European markets do not: guests who come for seven to fourteen nights because the country demands it. You cannot see Rome in three days. You cannot eat your way through Bologna in a weekend. You cannot explore Tuscany with a carry-on bag. Italy's average leisure stay duration is structurally longer than Germany or the Netherlands, and every extra night on the stay is a night that a smart traveller is asking themselves whether they want to spend it in a hotel room or in an apartment with a kitchen, a table to eat at, and a living room to read in. The aparthotel format answers that question. Adagio Rome Vatican, positioned for the Jubilee pilgrimage market, is not competing with the Hassler or the Eden. It is competing with the holiday apartment rental that the same family would otherwise book on a booking platform. At EUR 228 average daily rate for Rome hotels in H1 2025, the arithmetic of the aparthotel format looks increasingly attractive to the family spending fourteen nights in a city where every dinner out is EUR 80 and a hotel minibar is EUR 6 for a bottle of water." Troview Intelligence Head of Italy Aparthotel Research

SEGMENT INSIGHTS

| 03 | CITY PROFILE ANALYSIS |

Five City Markets Defining Italy's Aparthotel Geography

| H1 2025 Investment | RevPAR H1 2025 | Jubilee 2025 Demand | Key Openings 2025 |

| EUR 630M 37% of national volume (Il Sole 24 Ore) | EUR 158 (ADR EUR 228, occupancy 70%, +3% YoY) | Catholic Church Jubilee Year every 25 years | Orient Express La Minerva (93 rooms), Romeo Roma (74) |

Rome is Italy's primary hotel and aparthotel investment market, catalysing EUR 630 million of hotel investment in H1 2025 approximately 37% of the national total per Il Sole 24 Ore reporting of February 2026 following EUR 465 million in full-year 2024 that ranked it first among Italian cities. The average occupancy rate in Rome is 70% with an ADR of EUR 228 and a RevPAR of EUR 158, up 3% on 2024 per Il Sole 24 Ore market data, confirming that Rome's hotel performance metrics support premium aparthotel positioning for operators targeting the international leisure, Jubilee pilgrimage, and corporate conference market. Rome was inundated with tourists in 2025 due to the Jubilee of the Catholic Church and the death of Pope Francis per CoStar reporting of September 2025, generating extraordinary accommodation demand from pilgrims, religious delegations, media professionals, and tourism visitors in volumes that created overflow demand for aparthotel and serviced apartment alternatives to the city's premium hotel inventory. Notable 2025 openings in Rome including Orient Express La Minerva with 93 rooms, Romeo Roma designed by Zaha Hadid Architects with 74 rooms, and The Social Hub Rome with 392 rooms confirm the momentum of branded accommodation supply addition to the Roman market, with aparthotel formats benefiting from the same underlying demand that is attracting new branded hotel supply. Adagio operates its Rome Vatican aparthotel in the Balduina area near the Vatican with 119 apartments ranging from studios to two-room units, serving the Jubilee and leisure market that defines Rome's demand base.

| RevPAR H1 2025 | Milan Hotel Investment | Winter Olympics 2026 | Key Aparthotel |

| +5% (occupancy +3%, ADR +2%) strongest Italian city | EUR 173M in 2024 financial and corporate driver | Milan-Cortina hosting February 2026 | Starhotels serviced apartment significant market attention |

Milan is Italy's strongest performing hotel and aparthotel market by RevPAR growth trajectory, with H1 2025 RevPAR increasing 5% year-on-year driven by both occupancy growth of 3% and ADR growth of 2% the strongest performance of any major Italian city per Cushman and Wakefield Hotel Market Beat Italy H1 2025. The city's role as Italy's financial capital and fashion industry hub generates year-round corporate demand from financial services, consulting, luxury goods, and technology sectors whose visiting executives and project teams require premium accommodation for stays of five to twenty-one nights. Milan hosted the 2026 Winter Olympics in partnership with Cortina d'Ampezzo, with the February 2026 Games generating significant incremental accommodation demand and media and official delegation requirements that benefit the city's aparthotel operators who can accommodate group and family bookings more flexibly than hotel rooms. Starhotels Group's serviced apartment property in Milan was confirmed to receive significant market attention per CEO Elisabetta Fabri's comments at the Italian Hotel Investment Conference in September 2025, establishing the credibility of the apartment-format hospitality model among institutional Italian operators who have historically focused on conventional hotel formats.

| RevPAR H1 2025 | Florence Investment | Notable Opening H1 2025 | Key Demand Driver |

| EUR 180 (normalising phase per Il Sole 24 Ore) | EUR 353M in 2024 second to Rome nationally | Auberge Collection Alle Querce (83 rooms), The Hoxton (161) | Academic, arts, cultural tourism, MICE |

Florence is Italy's second-highest hotel investment destination in 2024 with EUR 353 million invested per EY Italy Hotel Investment Report 2024, and the city's RevPAR of EUR 180 in H1 2025 per Il Sole 24 Ore described as being in a normalising phase following the post-pandemic rate surge still represents one of the highest RevPAR levels of any Italian city and provides the income support for aparthotel operators willing to navigate Florence's historic centre planning restrictions. The city's combination of Renaissance art heritage, international academic community anchored by the Uffizi Gallery and its research programmes, fashion and artisanal craft industry, and MICE infrastructure at the Fortezza da Basso conference centre generates the diverse and balanced demand base that sustains aparthotel occupancy outside the summer leisure peak. Starhotels Group's serviced apartment property in Florence was cited alongside its Milan property as receiving significant market attention per Elisabetta Fabri's 2025 ITHIC comments, with Florence's international visitor profile particularly high-value North American and East Asian cultural tourists whose average stay duration exceeds the European average making it a strong market for apartment-format hospitality operators who can offer three to seven-night stays with kitchen access for a demographic that combines gallery visits with restaurant research.

| Venice RevPAR | Venice Investment | Bologna Occupancy 2025 | Bologna Driver |

| EUR 284 leads Italy nationally (Il Sole 24 Ore H1 2025) | EUR 353M in 2024, EUR 780M combined Rome+Venice H1 2025 | Close to 80% (medium-to-high end properties) | Italy's food capital, motor valley, university, MICE |

Venice leads Italy and one of the highest-performing European hospitality markets with a RevPAR of EUR 284 in H1 2025 per Il Sole 24 Ore, the highest of any Italian city, driven by the scarcity of quality hotel and aparthotel supply within the historic island city and the premium pricing that the unique urban environment commands from international leisure visitors seeking longer culturally immersive stays. Venice combined with Rome generated EUR 780 million of hotel investment in H1 2025 47% of the national total confirming that institutional capital is concentrating in markets with structural supply constraints that support premium long-term pricing. Bologna approaches 80% occupancy at medium-to-high end properties in 2025 per market analysis, emerging as Italy's fastest-growing secondary hotel and aparthotel market driven by the city's position as Italy's food capital, the Motor Valley's Ferrari and Lamborghini museum tourism, the University of Bologna's large international student community, and the Fiera di Bologna's active trade fair calendar that generates the most consistent year-round MICE demand of any Italian city outside Milan and Rome.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from verified company announcements, EY Italy Hotel Investment Reports, Cushman and Wakefield Hotel Market Beat Italy reports, and verified trade press.