By Facility Type - By State - By Payer - By Specialisation

City Spotlights: Sydney - Melbourne - Brisbane

Australia provided 43.6 million non-admitted patient care service events in 2024-25 per AIHW data, spent AUD 113.8 billion on hospital care in 2023-24 at AUD 4,223 per person, private hospitals admitted 3,812,478 same-day day-surgery patients in 2023-24 a 3% increase on the prior year ambulatory surgery now accounts for over 90% of Australian cataract procedures and 75% of hernia repairs, the Australian Government invested AUD 600 million in Primary Health Networks to enhance ambulatory access, and ambulatory care outpatient visits are projected to increase from 20 million in 2023 to 25 million within the forecast period.

MARKET SYNOPSIS

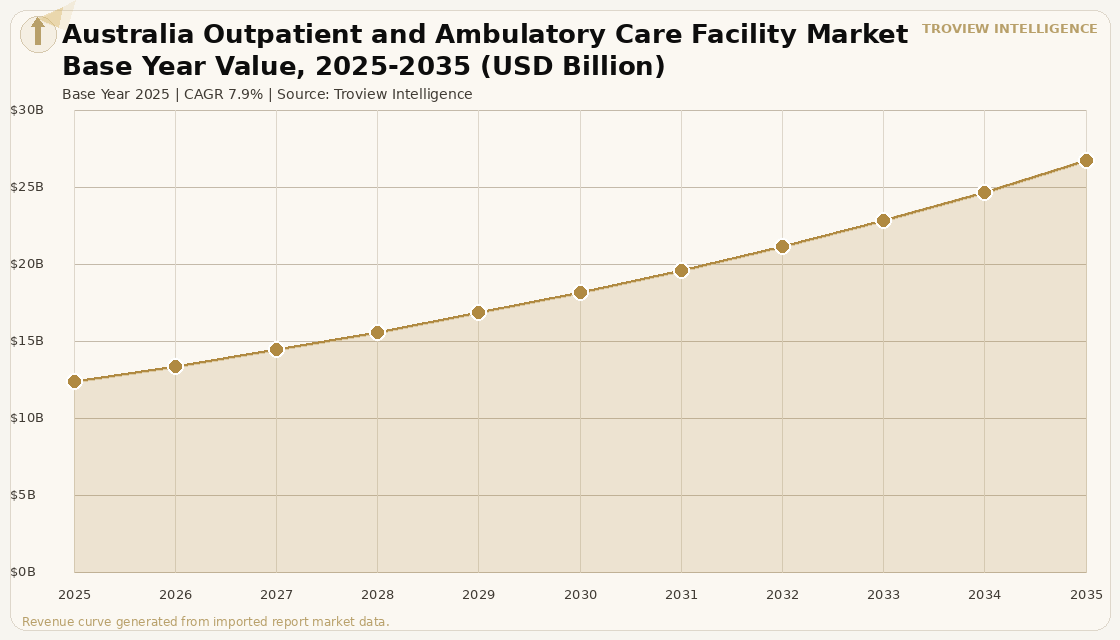

The Australia outpatient and ambulatory care facility market size was USD 12.64 Billion in 2025 and is expected to register a revenue CAGR of 7.9% during the forecast period, reaching USD 27.18 Billion by 2035. Australia's outpatient and ambulatory care market is the most mature in the Asia Pacific region, underpinned by the universal Medicare system that funds a broad range of outpatient medical services through the Medicare Benefits Schedule and by the private health insurance sector serving over 45% of the Australian population with hospital cover that finances elective outpatient procedures including day surgery. The Australian Institute of Health and Welfare confirmed that 43.6 million non-admitted patient care service events were provided for public patients in 2024-25, comprising 22.7 million allied health and clinical nurse specialist services, 14.1 million medical consultation services, and 3.6 million diagnostic services. Australia spent AUD 113.8 billion AUD 4,223 per person on hospital care in 2023-24, with AUD 270.5 billion in total health expenditure making it 42% hospital-focused per AIHW health expenditure Australia 2023-24. Private hospitals admitted 5,142,645 patients in 2023-24 a 3% increase on the prior year including 3,812,478 same-day day-surgery patients representing 74% of all private hospital admissions per Australian Private Hospitals Association verified data citing AIHW Admitted Patient Care 2023-24. For instance, in February 2026, Ramsay Health Care Limited, Australia, received ACCC approval for its acquisition of National Capital Private Hospital in Canberra from Healthscope, reinforcing Ramsay's position as Australia's largest private ambulatory care and hospital operator and confirming continued consolidation across the Australian private hospital and day-surgery sector. These are some of the key factors driving revenue growth of the market.

Australia's outpatient and ambulatory care market is shaped by a dual-track funding structure in which the Commonwealth funds outpatient services through the Medicare Benefits Schedule with the Original Medicare Safety Net threshold set at AUD 576 (USD 380) and the Extended Medicare Safety Net threshold at AUD 2,616 (USD 1,725) for eligible outpatient care in 2025 per Commonwealth Fund Australia country profile and the state and territory governments fund public hospital outpatient departments that collectively deliver the 43.6 million non-admitted patient care events per year. Australia's 637 private hospitals of which 559 were open in 2020, reflecting the growth of 78 new facilities primarily through doctor-owned day surgery centre openings per APHA comparing 2020 and 2025 hospital lists are expanding their ambulatory and day-surgery capacity in response to growing private health insurance utilisation and aging population demand for elective procedures. The Australian Government invested AUD 600 million in the Primary Health Networks programme to enhance access to outpatient and ambulatory services, with AUD 1.6 billion allocated for health technology initiatives including telehealth, and with 118.2 million telehealth services supported through My Health Record demonstrating the country's successful integration of digital health into ambulatory care delivery. Ambulatory surgery now accounts for more than 90% of Australian cataract procedures and 75% of hernia repairs per verified Australian hospital supplies data, confirming that the country's surgical mix is among the most ambulatory-oriented of any major healthcare economy globally.

However, the Australia outpatient and ambulatory care facility market faces structural constraints that limit sustainable growth. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating medical consumable supply chain cost increases and energy cost inflation that affect ambulatory surgical centres and day-surgery facilities whose consumable costs including surgical drapes, disposable instruments, anaesthetic agents, and diagnostic reagents are subject to global freight and energy price pass-through. Workforce shortages in nursing, allied health, and specialist medicine represent a structural capacity constraint that limits throughput at well-funded ambulatory facilities, with over 50% of Australian GPs rating their local PHN's value as poor or very poor in 2025 per Commonwealth Fund data, signalling systemic primary care capacity gaps that drive unnecessary emergency department presentations for conditions manageable in ambulatory settings. The tension between private health insurers who since 2022 have recorded unprecedented profits while holding premium increases to 3% per year or less per APHA reporting and private hospitals and ambulatory facilities over reimbursement rates and prior authorisation requirements is creating revenue realisation risk for ambulatory operators who face fixed-cost infrastructure against unpredictably approved procedure volumes. These factors substantially limit Australia outpatient and ambulatory care facility market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "Australia's ambulatory care market is structurally strong but operationally stressed. The demand is unambiguous 43.6 million non-admitted patient care events in a country of 26 million people, aging demographics, 3 million new same-day private hospital admissions in a single year. The supply side is where the system is under strain. Private health insurers are making unprecedented profits while simultaneously tightening prior authorisation requirements and refusing reasonable indexation to private hospitals and day-surgery centres. The result is a market where procedure volumes are growing, but margin per procedure is under pressure for ambulatory operators who cannot adjust their fixed-cost base quickly enough to absorb insurance reimbursement compression. The consolidation of Ramsay Health Care now acquiring National Capital from Healthscope with ACCC approval reflects a rational operator response to this environment: scale reduces the impact of per-procedure margin compression and improves negotiating leverage with insurers. The structural long-term thesis is intact: Australia's ambulatory care share of total surgical and diagnostic volume will continue to grow. The near-term operating environment is being defined by the insurer-hospital-government triangle rather than by patient demand." Troview Intelligence Head of Australia Outpatient and Ambulatory Care Research

SEGMENT INSIGHTS

Three Cities Shaping Australia's Ambulatory Care Market

| Sydney Health District | Private Hospital Count (NSW) | Key Operators | NSW Health Budget 2024-25 |

| Sydney Local Health District (SLHD) | Largest private hospital state | Ramsay, Healthscope, St Vincent's | AUD 120M Mount Druitt-Blacktown expansion |

Sydney is Australia's largest outpatient and ambulatory care facility market, hosting the greatest concentration of private hospitals, specialist day-surgery centres, and diagnostic imaging facilities of any Australian city. The Sydney Local Health District encompasses Royal Prince Alfred Hospital one of Australia's largest and most complex tertiary referral hospitals with a major specialist outpatient clinic network alongside a range of specialist ambulatory clinics in cardiology, oncology, gastroenterology, and allied health that collectively manage tens of millions of non-admitted patient care events annually across NSW. New South Wales represents the largest state component of Australia's outpatient and ambulatory care market, with the AUD 120 million investment to upgrade Blacktown and Mount Druitt Hospitals announced in May 2025 adding 60 additional beds across the two facilities reflecting continuing capital investment in hospital outpatient and ambulatory capacity in western Sydney's fast-growing catchment . Ramsay Health Care operates the largest private hospital network in Australia with a significant Sydney presence, with the company's Ramsay Health Hub digital front door programme now at 39 Australian sites enabling patients to manage ambulatory outpatient referrals and pre-procedure preparation through an integrated digital platform per Ramsay Health Care FY25 full-year financial report.

| Key Health Services | Telehealth Services (National) | Peter MacCallum Role | Victorian Health Expenditure |

| Ramsay, Healthscope, St John of God | 118.2M via My Health Record (national) | Primary cancer ambulatory hub | Second-largest state health budget in Australia |

Melbourne is Australia's second-largest outpatient and ambulatory care facility market, hosting a dense network of private and public specialist outpatient services anchored by the Alfred Hospital, Peter MacCallum Cancer Centre, Royal Melbourne Hospital, and Melbourne Health's network of ambulatory care clinics. Victoria's healthcare system has been at the forefront of Australia's telehealth integration, with the national rollout of 118.2 million telehealth services through My Health Record representing a significant portion delivered through Victorian primary care and specialist outpatient infrastructure per verified Australian healthcare infrastructure data. Peter MacCallum Cancer Centre operates as Australia's primary cancer ambulatory care facility, providing outpatient oncology treatment including chemotherapy, radiation therapy, and immunotherapy to patients who can receive complex cancer care without inpatient admission through the centre's ambulatory oncology model. Melbourne's private hospital and day-surgery sector is led by Ramsay Health Care, Healthscope, and St John of God Health Care, which collectively operate the majority of private ambulatory surgical capacity serving Melbourne's 5.2 million metropolitan population.

| Queensland Health Role | Growth Driver | Key Private Operators | Infrastructure Investment |

| Royal Brisbane and Women's Hospital | SEQ population growth fastest in Australia | Ramsay, Mater Health, St John of God | QLD Health capital programme expanding |

Brisbane is the fastest-growing major Australian city for outpatient and ambulatory care facility development, driven by Southeast Queensland's population growth the fastest of any major Australian metropolitan region which is creating sustained demand for ambulatory care capacity across primary care, specialist, and surgical outpatient services that existing infrastructure cannot meet at scale. Queensland Health operates the Royal Brisbane and Women's Hospital one of Australia's largest tertiary hospitals alongside a statewide network of specialist outpatient clinics that serve the Queensland Health system's managed outpatient waiting list, with elective outpatient waiting times at public hospitals in Queensland creating demand for private ambulatory alternatives among patients with private health insurance. The private hospital sector in Brisbane is led by Ramsay Health Care, Mater Health Services, and St John of God Health Care, which collectively operate multiple day-surgery centres and private hospital ambulatory departments serving Brisbane's growing private health insurance-holding patient population that is among Australia's highest by proportion of private insurance coverage.