| TROVIEW INTELLIGENCE | Senior Care and Assisted Living Market | Q2 2026 |

By Geography - By Facility Type - By Service - By Ownership Model

The global assisted living market was valued at USD 180.02 Billion in 2025, North America led with a 35.28% share at USD 63.51 Billion, the United States operates over 30,600 assisted living communities with 1,197,600 licensed units and a median annual cost of USD 54,000, the WHO reported in October 2025 that 1 in 6 people globally will be 60 or older by 2030 rising from 1 billion in 2020 to 1.4 billion and doubling to 2.1 billion by 2050, dementia affected approximately 57 million people in 2021 with nearly 10 million new cases diagnosed each year per WHO March 2025 update, and Inspiren secured USD 35 Million in funding in March 2025 to expand AI technology across senior living facilities confirming private capital's accelerating deployment into care technology.

MARKET SYNOPSIS

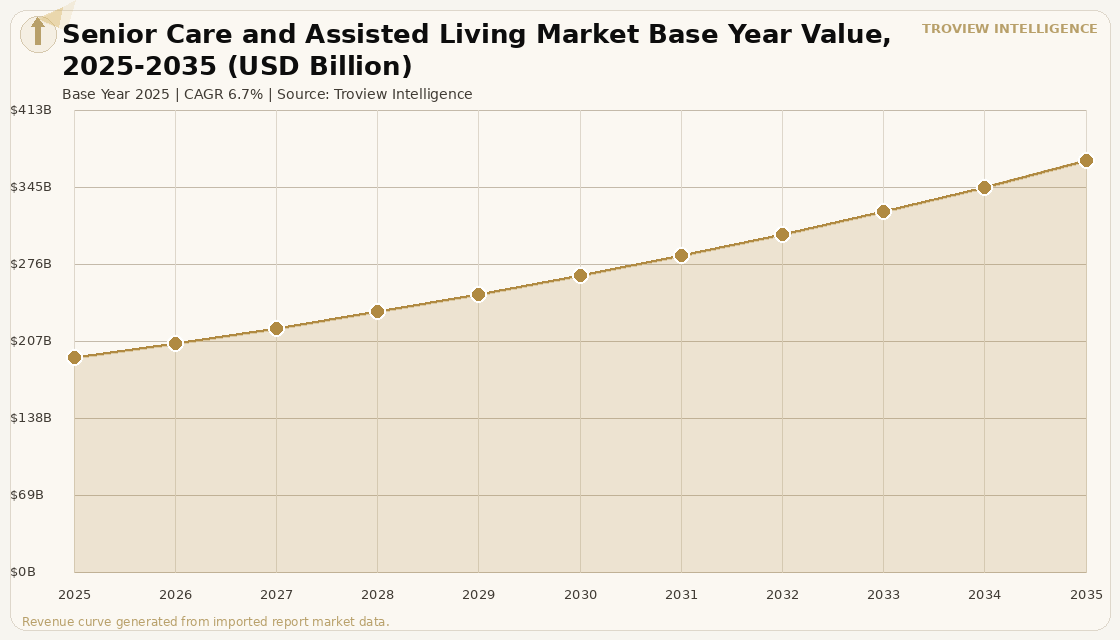

The global senior care and assisted living market size was USD 192.46 Billion in 2025 and is expected to register a revenue CAGR of 6.7% during the forecast period, reaching USD 369.14 Billion by 2035. The senior care and assisted living market encompasses independent living communities for active seniors, assisted living facilities providing support with activities of daily living, memory care units for residents with dementia and Alzheimer's disease, continuing care retirement communities offering a full spectrum from independent to nursing home care, and home-based senior care services that deliver medical and personal care to seniors aging in place. The United States operates over 30,600 assisted living communities with 1,197,600 licensed units in 2024 per American Health Care Association and National Center for Assisted Living verified data, with median annual assisted living cost of USD 54,000 significantly below the USD 61,776 median for home health aide and USD 94,896 for nursing home semi-private care per ACHA and NCAL data, confirming the cost-competitiveness of assisted living relative to alternative care formats. The 2025 market estimate is grounded in verified operator revenues: Brookdale Senior Living, United States, operates the largest standalone senior care and assisted living platform in the country with over 300,000 seniors served; Genesis HealthCare partnered with Senior Lifestyle in May 2024 to expand assisted living options; and Inspiren, United States, secured USD 35 Million in Series A funding in March 2025 led by Avenir to expand AI-powered motion analysis and fall-risk detection technology across senior living facilities per verified assisted living market data. These are some of the key factors driving revenue growth of the market.

North America dominated the global senior care and assisted living market in 2025 with a 35.28% revenue share at USD 63.51 Billion per verified senior care market data, driven by the United States' advanced senior living infrastructure, rising chronic disease prevalence among the 65-plus population, and the demographic certainty of the Baby Boomer generation with all Baby Boomers aged 65 or above by 2030, representing one in five Americans creating an unprecedented demand surge that senior living operators began positioning for a decade in advance. Europe contributed approximately USD 49.39 Billion in 2025 at a 27.43% revenue share, with the United Kingdom market projected at USD 11.32 Billion by 2026 and Germany at USD 8.51 Billion by 2026, driven by 21.3% of the EU population aged 65 or above in 2023 per verified Eurostat data and rising acceptance of professional senior care among European families as nuclear family formation rates create structural gaps in informal care capacity. Asia Pacific represented USD 40.28 Billion in 2025 at a 22.38% share and is the fastest-growing region, with China operating over 387,000 elderly care institutions and 8.29 million beds in 2022 per verified government data and India's 156.7 million over-60 population in 2024 representing the world's second-largest elderly cohort growing to 346 million by 2050.

However, the global senior care and assisted living market faces structural constraints that limit the pace of capacity and revenue growth across all markets. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation and medical supply chain cost pressures that increase the operating costs of assisted living facilities where energy, food, and medical consumables represent 30 to 40% of total operating expenditure and cannot easily be reduced without affecting resident care quality or service standards. Staffing shortages and caregiver wage inflation represent the most acute structural constraint in senior care globally, with the United States projected to face a shortage of 1.2 million healthcare workers by 2030 per verified healthcare workforce data, directly limiting the number of residents that existing licensed senior care facilities can serve and driving labour cost inflation that erodes operator EBITDA margins even as occupancy and ADR grow. Nearly 60% of older adults will need some form of long-term care per Administration for Community Living verified data, but only 5% of India's elderly population and approximately 1.3% of India's elderly currently have access to institutional care, while developing markets face affordability barriers that prevent monetisation of the demographic demand wave at scale. These factors substantially limit global senior care and assisted living market growth over the forecast period.

The senior care and assisted living market is one of the most demographically certain investment theses in global real estate and healthcare. The WHO has confirmed that 1 in 6 people globally will be 60 or older by 2030, doubling to 2.1 billion by 2050. Baby Boomers in the United States will all be 65 or above by 2030. India's elderly population will double from 156.7 million today to 346 million by 2050. These are not projections that require modelling assumptions to validate. They are census arithmetic. The investment challenge is not whether senior care demand will grow it will, everywhere but whether operators can build the physical plant, recruit the workforce, and maintain the clinical quality simultaneously. In the United States, the 30,600 assisted living communities with 1.2 million licensed units are already demonstrably insufficient for the arriving demand wave. In India, the 1.3% market penetration rate against a 156.7 million elderly population represents one of the largest addressable demand gaps in global real estate. The markets that navigate workforce development and regulatory framework construction fastest will generate the strongest investor returns of the next two decades." Troview Intelligence Head of Global Senior Care and Assisted Living Research

SEGMENT INSIGHTS

By Facility Type

Active adult and independent living community facility type is expected to account for a significantly large revenue share in the global senior care and assisted living market during the forecast period.

Based on facility type, the global senior care and assisted living market is segmented into active adult and independent living communities, assisted living facilities, memory care units, continuing care retirement communities, nursing homes and skilled nursing facilities, and home care and hospice. Active adult 55-plus communities held the largest revenue share of 69.52% in 2024 per verified senior living market data, with demand driven by healthier, financially secure Baby Boomers seeking resort-style amenities, fitness facilities, cultural activities, and lifelong learning opportunities in age-restricted communities. Assisted living facilities are expected to register the fastest CAGR during the forecast period at 7.40% through 2034 per verified assisted living market data, driven by the growing number of seniors entering assisted living at more advanced ages with higher prevalence of complex health conditions including diabetes, cardiovascular disease, and Alzheimer's disease.

By Service Type

Personal care and assistance services segment is expected to account for a significantly large revenue share in the global senior care and assisted living market during the forecast period.

Based on service type, the global senior care and assisted living market is segmented into personal care and assistance, healthcare and medical services, memory care and dementia support, rehabilitation and physiotherapy, social engagement and wellness programming, and nutrition and dietary services. Personal care and assistance services held the largest share of the assisted living market in 2024, providing support with grooming, bathing, dressing, and medication management that defines the core service proposition distinguishing assisted living from independent living. Healthcare and medical services are expected to register the fastest CAGR during the forecast period, as an increasing proportion of assisted living residents enter facilities at more advanced ages with complex co-morbidities requiring visiting specialist physicians, on-call nursing, wound care, IV therapy, and diagnostic monitoring that previously was only available in skilled nursing facilities.

By Ownership Model

For-profit assisted living facility ownership model is expected to account for a significantly large revenue share in the global senior care and assisted living market during the forecast period.

Based on ownership model, the global senior care and assisted living market is segmented into for-profit private facilities, non-profit and faith-based facilities, government and publicly-funded facilities, and continuing care retirement community operators offering both ownership and rental models. For-profit facilities dominated with the largest revenue share in 2024 per verified market data, as chain-affiliated operators including Brookdale Senior Living, Sunrise Senior Living, and Atria Senior Living have built national portfolios that generate economies of scale in purchasing, staffing, and technology deployment that independent operators cannot match. Chain-affiliated facilities dominate the assisted living market due to consistent care standards, branding, and consumer trust per verified market data, with chains expanding rapidly in both mature markets through acquisition and emerging markets including India through greenfield development.

REGIONAL ANALYSIS

NORTH AMERICA 35.28% SHARE, 30,600+ US COMMUNITIES, BABY BOOMER DEMAND WAVE

| NA Revenue 2025 | US Assisted Living Units | US Median Annual Cost | US Baby Boomer Impact |

| USD 63.51 Billion (35.28%) | 1,197,600 licensed units, 30,600+ communities | USD 54,000/year (median) | All Baby Boomers age 65+ by 2030 1 in 5 Americans |

North America is the global senior care and assisted living market leader, with the United States operating over 30,600 assisted living communities with 1,197,600 licensed units in 2024 per ACHA and NCAL data, hosting the world's most mature and institutionally invested senior living industry. The US market is structurally positioned at the beginning of its largest demand surge: the US Census Bureau estimates that by 2030 all Baby Boomers will be over 65, resulting in one in every five Americans being of retirement age, creating unprecedented demand for assisted living, memory care, and continuing care retirement community inventory that the current US supply base cannot meet at scale without significant new development. The median annual cost for assisted living in the United States reached USD 54,000 in 2024 per ACHA and NCAL data representing a cost structure significantly below the USD 61,776 annual median for home health aide and the USD 94,896 for nursing home semi-private care making assisted living the most cost-competitive care transition for seniors requiring support beyond home-based management. Discovery Senior Living's investment in a new clinical technology platform in March 2025 reflects the sector's broader trend toward technology-enabled care efficiency that allows operators to serve more residents per clinical staff member by leveraging AI-driven monitoring and predictive health management.

ASIA PACIFIC

| APAC Revenue 2025 | China Elderly Care Facilities | India 60+ Population 2024 | India Market Penetration |

| USD 40.28 Billion (22.38%) | 387,000 facilities / 8.29M beds (2022) | 156.7 million world's 2nd largest | 1.3% vs 6%+ in US and Australia |

Asia Pacific is the fastest-growing region in the global senior care and assisted living market, driven by rapid population aging across China, India, Japan, South Korea, and Australia. China operates over 387,000 elderly care institutions providing 8.29 million beds as of 2022 per verified Chinese government data, with the 65-plus population reaching 209.78 million and the China assisted living market projected to reach USD 14.68 billion by 2026 per verified market data. India represents the most compelling long-term market opportunity: with 156.7 million elderly persons aged 60 and above in 2024 the world's second-largest elderly cohort and a senior living market penetration rate of only 1.3% against potential demand of 1.57 million to 2.3 million households, compared to mature markets including the United States and Australia where penetration rates exceed 6%, India's addressable senior care demand gap is among the largest of any healthcare sector globally per JLL India senior living market analysis. The India senior living market was valued at USD 3.55 Billion in 2025 and is estimated to grow at a CAGR of 25.92% through 2031 per verified market data, confirming the exceptional growth potential of the sector in a market where nuclearising families, NRI parents, and rising HNWI populations create institutional-quality demand for professionally managed senior care.

EUROPE

| Europe Revenue 2025 | EU 65+ Population (2023) | UK Market 2026 Projection | Germany Market 2026 Projection |

| USD 49.39 Billion (27.43%) | 95.6 million 21.3% of EU population | USD 11.32 Billion | USD 8.51 Billion |

Europe is the second-largest global senior care and assisted living market, with 95.6 million EU residents aged 65 and above in 2023 representing 21.3% of the overall EU population per verified Eurostat data, creating sustained structural demand for assisted living and memory care services across mature Western European markets and rapidly aging Eastern European nations. Germany's senior care market is led by Clariane and Dussmann Group, which are expanding memory care and chronic condition management services, while the UK market supports higher levels of specialized care acceptance than comparable markets due to NHS-supplemented care funding frameworks. Dementia care is the fastest-growing specialty in European senior care, driven by the WHO's estimate that dementia affected 57 million people globally in 2021 with 10 million new cases per year a prevalence driven predominantly by an aging European demographic with memory care unit development accelerating across the United Kingdom, Germany, France, and the Netherlands as specialist dementia care providers respond to the gap between available memory care beds and confirmed diagnosis rates in major European cities.