By District - By Specialty - By Regulatory Zone - By Patient Demographics

Districts: Dubai Healthcare City - Jumeirah - Business Bay - Al Barsha - Dubai Marina

Dubai's private healthcare sector is growing at 7% annually through 2030, established dental clinics generate returns of 10 to 20% annually with cosmetic-focused clinics breaking even within 10 months, clinic real estate costs range from AED 100 to 300 per square foot annually depending on district, specialty clinic setup requires AED 800,000 to AED 2 million or above for well-equipped dental centres, 80% of UAE patient searches occur on smartphones and DHA licensing is mandatory for all Dubai clinic operations, and Dubai Healthcare City provides a purpose-built free zone with 100% foreign ownership for internationally-branded dental and specialty clinic operators.

MARKET SYNOPSIS

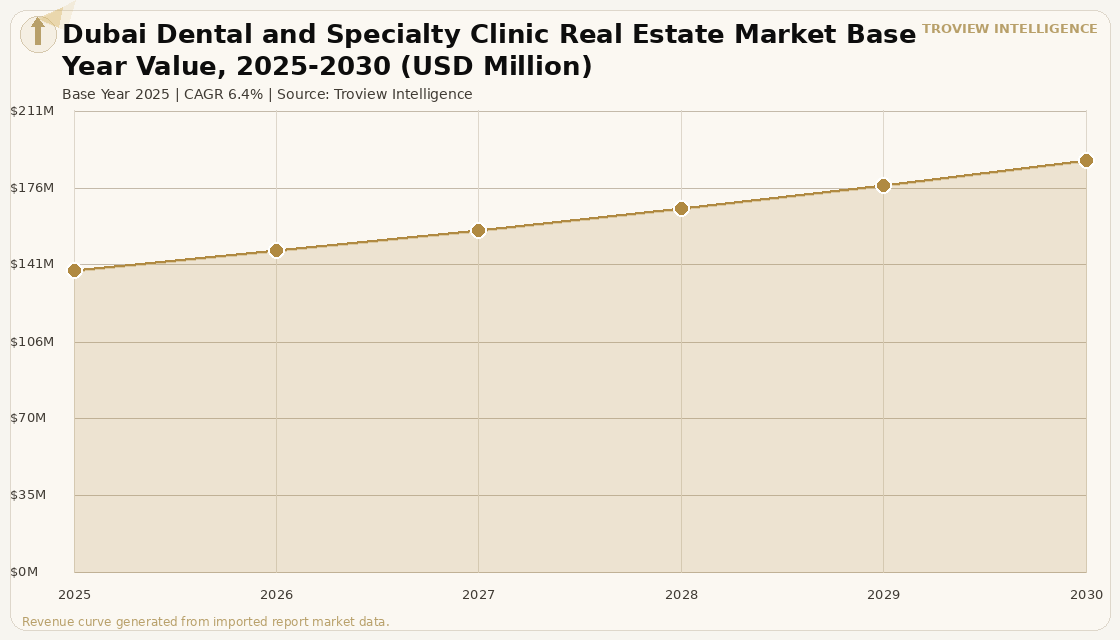

The Dubai dental and specialty clinic real estate market size was USD 138.46 Million in 2025 and is expected to register a revenue CAGR of 6.4% during the forecast period, reaching USD 188.72 Million by 2030. Dubai is the UAE's dominant dental and specialty clinic market, hosting the largest concentration of private dental clinics, aesthetic medicine centres, dermatology practices, and multi-specialty outpatient facilities in the country, serving a patient population of approximately 3.6 million permanent residents the majority of whom are expatriates from high-income source countries including India, the United Kingdom, the United States, Australia, and Western Europe alongside significant volumes of medical and dental tourism visitors who arrive specifically for cosmetic dental, orthodontic, and aesthetic medical procedures at international-standard quality and at price points that compare favourably to their home markets for self-funded procedures. Dubai's dental clinic market is characterised by a cosmetic dental premium: over 70% of UAE residents express interest in cosmetic dental procedures per verified market data, with a high-income European expatriate dental clinic in Downtown Dubai that focuses on cosmetic dentistry and orthodontics demonstrating a breakeven within 10 months and 65% of revenue from aesthetic dentistry packages per Aviaan verified feasibility case study. For instance, in 2025, Dubai's private dental clinic ecosystem continued to grow with new clinic openings across Dubai Healthcare City, Jumeirah, Business Bay, and JLT, driven by DHA's streamlined licensing framework that coordinated correctly across facility licensing and professional licensing tracks can be completed in 3 to 4 months for well-prepared operators per DIAC verified Dubai clinic license process guide. These are some of the key factors driving revenue growth of the market.

Dubai's dental clinic real estate investment market is among the most transparent and commercially documented of any emerging market dental cluster globally, with clinic real estate costs, licensing requirements, setup cost ranges, and revenue benchmarks all well-documented through DHA public regulation, real estate agent listings, and the healthcare business brokerage sector. Established dental clinics are priced from AED 700,000 to AED 5 Million on acquisition depending on specialty, patient volume, equipment, and DHA licensing type per Mokza Healthcare Consultancy verified data, with dental clinics consistently among the most profitable healthcare real estate investment categories in Dubai alongside cosmetic and aesthetic clinics. The Dubai dental clinic market exhibits clear geographic segmentation by patient wealth and service offering: premium cosmetic dental clinics concentrate in Jumeirah, Downtown Dubai, and DIFC where high-net-worth international residents and tourists access veneers, implants, and orthodontic treatment at above-average procedure prices; mid-range general and family dental clinics serve the working professional expatriate populations in Al Barsha, Tecom, JVC, and JLT; and affordable dental care for the lower-income expatriate workforce is accessed through clinics in Al Qusais, Deira, and the older Bur Dubai commercial areas. Each dental clinic geographic tier carries different real estate costs, patient acquisition costs, and procedure value averages, creating distinct investment theses for different clinic categories within the same city.

However, the Dubai dental and specialty clinic real estate market faces structural constraints that limit the pace of new clinic supply growth and operating margin sustainability. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation and dental consumable supply chain cost increases that affect Dubai dental clinic operators whose dental materials including titanium implant components, ceramic crown blanks, and clear aligner material are subject to global logistics cost pass-through at a time when DHA regulatory compliance costs already represent a significant proportion of new clinic operating budgets. Dubai's dental specialist shortage where high demand for DHA-licensed implantologists, orthodontists, and cosmetic dentists exceeds the licensed supply across all market segments creates a talent competition that drives specialist dentist salaries to levels that compress operator EBITDA margins even as procedure revenue grows, with overseas dental specialist recruitment through primary source verification, DHA eligibility examination, and visa processing adding 3 to 6 months to the hiring timeline for new clinic operators. The strong competition from the 4,482 private healthcare facilities in the UAE market of which dental clinics represent a significant component creates patient acquisition cost pressure as established clinics with strong Google review profiles and patient databases hold significant advantages over newer entrants who must invest AED 80 to 200 per qualified dental patient inquiry in digital marketing to establish a patient base. These factors substantially limit Dubai dental and specialty clinic real estate market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "Dubai's dental clinic market in 2025 has a geographic clarity that makes investment decision-making unusually straightforward compared to most healthcare real estate markets. You can identify the patient demographic, the procedure mix, the average procedure value, and the competitive density within a 3 to 5 kilometre catchment of any proposed clinic location with a reasonable level of certainty. A cosmetic dental and orthodontic clinic in Jumeirah serves the European and American expatriate demographic who self-fund veneers and clear aligners at above-average procedure values and refer their friends through social networks with high patient lifetime values. A family dental clinic in Al Barsha serves the South Asian professional demographic who prioritises value, accessibility, and comprehensive family care at moderate price points. A clinic in Deira serves the South Asian and Arab blue-collar demographic who needs basic restorative care at the lowest price points. These are fundamentally different businesses with fundamentally different real estate requirements. The investor who understands this geographic stratification and matches their clinic concept and capital investment level to the right catchment generates the 10 to 20% annual returns that Dubai dental clinic investment is documented to produce. The investor who puts a premium clinic in the wrong location generates write-offs." Troview Intelligence Senior Analyst, Dubai Healthcare Real Estate

SEGMENT INSIGHTS

District Deep-Dives

| Free Zone Advantage | Anchor Hospital | Clinic Rent (Mid-Range) | Primary Tenant Profile |

| 100% foreign ownership, DHCR licensing | Mediclinic City Hospital | AED 150-200/sqft annually | International dental and specialty groups |

Dubai Healthcare City is Dubai's purpose-built healthcare free zone and the preferred location for internationally-branded dental and specialty clinic operators entering the UAE market, offering 100% foreign ownership, DHCR licensing separate from DHA mainland requirements, co-location with Mediclinic City Hospital and Moorfields Eye Hospital Dubai as anchor healthcare tenants, and an established cluster of international medical professionals that generates cross-referral opportunities for dental clinic tenants. DHCC's mid-range rental costs of AED 150 to 200 per square foot annually position it between the premium Jumeirah and Downtown market at AED 200 to 300 per square foot and the more affordable Al Barsha and JLT markets at AED 100 to 150 per square foot, making it accessible for well-capitalised international clinic operators while maintaining a premium brand environment. International dental groups including Colosseum Dental Group have established UAE operations through free zone structures that allow foreign ownership and management control, a structural advantage not available to equivalent mainland clinic investments prior to the 2021 foreign ownership liberalisation. DHCC's healthcare campus also provides dental clinic operators with organic patient referral flows from the hospital and specialist medical tenants within the campus who refer patients requiring dental clearance before cardiac surgery, organ transplant, or cancer treatment.

Jumeirah and Downtown Dubai PREMIUM COSMETIC MARKET, HIGHEST PROCEDURE VALUES, WESTERN EXPAT LED

| Clinic Rent Range | Primary Specialty | Patient Profile | Breakeven Timeline |

| AED 200-300/sqft annually | Cosmetic dentistry, veneers, implants | High-income European and American expats | 10 months (verified Aviaan case study) |

Jumeirah and Downtown Dubai constitute Dubai's premium cosmetic dental clinic district, hosting the highest concentration of specialist cosmetic dental and aesthetic medical clinics in the UAE that serve the city's high-income European, North American, and GCC resident demographic who access veneers, composite bonding, teeth whitening, clear aligner orthodontics, and implant placement at procedure values that generate the 10 to 20% annual clinic returns documented for DHA-approved dental clinics in this district. A verified feasibility case study of a high-end European group opening a cosmetic dentistry and orthodontics clinic in Downtown Dubai documented breakeven within 10 months and 65% revenue from aesthetic dentistry packages, confirming the financial viability of the premium cosmetic dental clinic model in Dubai's most affluent residential and tourist districts. Clinic real estate rental costs in Jumeirah and Downtown Dubai at AED 200 to 300 per square foot annually represent the highest in the Dubai dental clinic market, but are justified by the dental tourism premium and the ability to price cosmetic procedures at above-market rates to the premium patient demographic that accesses these districts. DHA-approved dental clinics in Jumeirah are among the most actively transacted in the Dubai healthcare business brokerage market, with established clinics selling from AED 700,000 to AED 5 million depending on patient volume, equipment quality, and specialty mix per Mokza Healthcare Consultancy data.

Al Barsha and JLT MID-RANGE MARKET, SOUTH ASIAN PROFESSIONAL BASE, HIGHEST PATIENT VOLUME

| Clinic Rent Range | Primary Specialty | Patient Profile | Key Advantage |

| AED 100-150/sqft annually | Family and general dentistry, orthodontics | Indian, Pakistani, Arab professional expats | Highest patient volume density in Dubai |

Al Barsha and Jumeirah Lakes Towers constitute Dubai's mid-range dental clinic district, hosting the highest volume of general family dental clinics that serve the South Asian professional expatriate demographic across affordable to mid-range pricing for general dentistry, paediatric care, basic orthodontics, and restorative treatments. Clinic real estate in Al Barsha and JLT at AED 100 to 150 per square foot annually represents the most accessible entry point for independent dental practitioners and small multi-location groups seeking to establish Dubai operations with lower initial real estate commitment than premium district locations. The South Asian professional expatriate patient base in Al Barsha and JLT generates the highest patient volume of any Dubai district for general dental services, driven by the large Indian and Pakistani expatriate communities in adjacent residential areas including Discovery Gardens, Sports City, and the JLT residential towers who prioritise accessible pricing, South Asian-language capability in clinic administration, and comprehensive family dental coverage across adults and children. Dental patient acquisition cost in Al Barsha at AED 80 to 200 per qualified patient inquiry via Google Ads digital marketing per healthcare marketing agency verified benchmark is consistent with the broader Dubai market, but the lower average procedure value relative to Jumeirah means patient acquisition cost management is more critical to margin sustainability in this district than in premium cosmetic-focused districts.