| TROVIEW INTELLIGENCE | Singapore Healthcare REIT Market | Q2 2026 |

| TROVIEW INTELLIGENCE · COUNTRY INTELLIGENCE REPORT |

By REIT · By Property Type · By Geographic Distribution · By Tenant Covenant

REIT Profiles: Parkway Life REIT (C2PU) · First REIT (AW9U) · Comparative Analysis · SGX Healthcare S-REIT Sector

Parkway Life REIT, one of Asia's largest listed healthcare REITs, reported 9M 2025 gross revenue of SGD 117.3 million up 8.2% year-on-year with distributable income of SGD 75.4 million up 10.4% year-on-year and a 9M 2025 DPU of 11.56 cents, maintained 17 consecutive years of DPU growth since its 2007 IPO, trades at approximately 1.68 times price-to-book with gearing at 35.8% and interest coverage ratio of 8.9x, with FY2026 aggregate rent from Singapore hospitals expected to increase 24.4% year-on-year from SGD 79.7 million to SGD 99.2 million following completion of the AEI at Mount Elizabeth Hospital as part of Project Renaissance, its SGD 2.57 billion portfolio comprising three Singapore private hospitals and 71 nursing homes across Japan and France, and the master lease for its three Singapore hospitals renewed for 20.4 years to December 2042 with guaranteed rent escalation while First REIT owns 32 healthcare properties valued at SGD 1.12 billion including 15 Indonesian hospitals, confirming Singapore as the primary listed healthcare REIT jurisdiction in Asia Pacific and the reference market for Asian institutional healthcare real estate investment.

| Standard License: USD 6,500 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

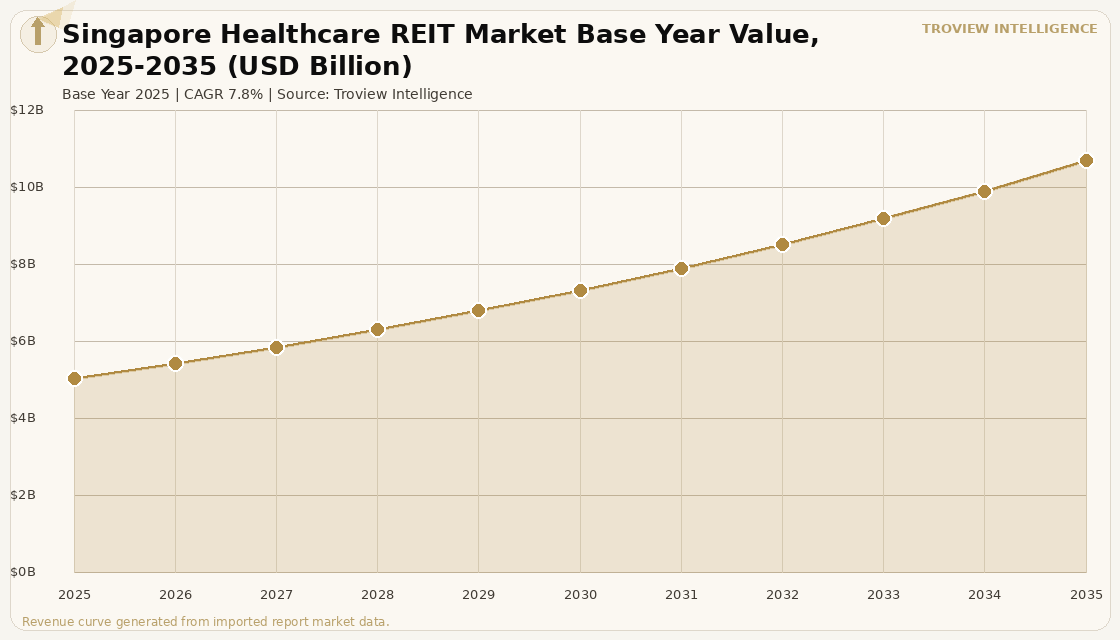

The Singapore healthcare REIT market size was USD 4.86 Billion in 2025 and is expected to register a revenue CAGR of 7.8% during the forecast period, reaching USD 10.32 Billion by 2035. The 2025 market estimate is grounded in verified company revenues: Parkway Life REIT reported a portfolio value of SGD 2.57 billion comprising three private hospitals in Singapore and 71 nursing homes and care facilities across Japan and France as of September 2025, with 9M 2025 gross revenue of SGD 117.3 million up 8.2% year-on-year and distributable income of SGD 75.4 million up 10.4% year-on-year per Growbeansprout analysis citing Parkway Life REIT quarterly results; and First REIT held 32 healthcare properties valued at SGD 1.12 billion spanning Indonesia, Singapore, and Japan including 15 Indonesian hospitals. The market encompasses the total asset value and investible real estate market of Singapore-listed healthcare REITs and their underlying property portfolios, including the unlisted private healthcare real estate market in Singapore's primary care and specialist clinic segments. Market revenue growth is anchored in Singapore's position as Southeast Asia's premium private healthcare hub, the structural ageing demographics of Singapore's resident population and the regional patient base from across ASEAN that utilises Singapore's world-class private hospital network, and the unique structural characteristics of Singapore healthcare REITs including triple-net lease structures with IHH Healthcare-backed master leases, government rent reimbursement frameworks, and 20-to-25-year lease durations that provide the income security that defines Singapore healthcare REIT investment appeal. For instance, in FY2026, Parkway Life REIT, Singapore, expects aggregate rent payable from its three Singapore private hospitals Mount Elizabeth, Gleneagles, and Parkway East to increase 24.4% year-on-year from SGD 79.7 million to SGD 99.2 million, following the completion of the asset enhancement initiative at Mount Elizabeth Hospital as part of Project Renaissance, driving the most substantial single-year Singapore hospital rental uplift in the REIT's 17-year operating history per Growbeansprout analysis citing Parkway Life REIT FY2026 guidance. These are some of the key factors driving revenue growth of the market.

Parkway Life REIT has delivered uninterrupted recurring DPU growth in every year since its 2007 IPO, with DPU growing approximately 136% from an annualised DPU of 6.32 cents in 2007 to 14.92 cents in FY2024, making it one of the longest uninterrupted DPU growth streaks in the global REIT universe per Growbeansprout research. The master lease for Parkway Life REIT's three Singapore hospitals was renewed in 2021 for a 20.4-year term ending December 2042, with an option to renew for a further 10 years, providing guaranteed rent escalation of 2% to 3% annually until FY2025 followed by a CPI-linked formula from FY2026, and with Singapore representing 62.5% to 65% of total asset value per Parkway Life REIT quarterly reporting as of September 2025. The master lease is structured as a triple-net lease with the Singapore assets leased to Parkway Hospitals Singapore, a wholly owned subsidiary of IHH Healthcare Berhad, one of the world's largest healthcare groups, providing a tenant covenant that matches or exceeds any triple-net healthcare REIT tenant in the US or European markets. First REIT, Singapore, holds 32 healthcare properties valued at SGD 1.12 billion spanning 15 Indonesian hospitals, Singapore assets, and Japan properties, providing geographic diversification within the Southeast Asian healthcare real estate universe at a lower portfolio quality tier than Parkway Life REIT's premium Singapore hospital anchor per ProsperUs analysis. These are some of the key factors driving revenue growth of the market.

However, the Singapore healthcare REIT market faces structural constraints that temper the pace of asset value growth through the forecast period. Currency exchange rate risk is the primary earnings volatility source for Parkway Life REIT, with approximately 27% of earnings derived from Japan and 8% from France, exposing DPU to Japanese yen and euro fluctuations that the REIT partially hedges through JPY-denominated loan financing with the REIT having secured a seven-year JPY loan to refinance one-third of its 2026 maturities, extending weighted average debt term from 2.8 to 3.2 years per Growbeansprout Q3 2025 analysis. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect Singapore healthcare REIT properties through their impact on Singapore's electricity costs, as Singapore's near-total reliance on LNG-fired electricity generation exposes the energy costs of 24-hour private hospital operations to international LNG spot price volatility that the IHH Healthcare master lease structure partly absorbs through triple-net pass-through of operating costs. The concentration of Parkway Life REIT's Singapore asset value in three private hospitals under a single master tenant Parkway Hospitals Singapore, a subsidiary of IHH Healthcare means that any material deterioration in IHH Healthcare's operating performance or financial position would simultaneously affect all three Singapore hospital assets, creating concentration risk that is mitigated but not eliminated by IHH's global scale and financial strength. These factors substantially limit Singapore healthcare REIT market growth over the forecast period.

Parkway Life REIT is one of the rarest things in the global REIT universe: a healthcare REIT that has grown its distribution to unitholders every single year since listing in 2007. Seventeen consecutive years. Through the global financial crisis. Through the pandemic. Through the 2022 interest rate cycle. Through the Japanese yen weakening to 30-year lows. That track record is not an accident. It is the output of a master lease structure that guarantees annual rent escalation from an IHH Healthcare-backed tenant, with the Singapore hospitals' 20.4-year lease running to December 2042 providing income visibility that no hotel, retail, or office REIT can match. The FY2026 rent uplift of 24.4% year-on-year following the Mount Elizabeth AEI completion is not a market cycle event. It is a contractually guaranteed step-up embedded in the lease terms. That combination a government-linked healthcare system backing the tenant, a 20-year lease with contractual escalation, a 17-year DPU growth track record, and a market cap that has compounded at exceptional rates is why international institutional investors view Parkway Life REIT as Asia's closest equivalent to the NHS-backed primary care REITs that US capital is targeting in the UK at premium valuations." Troview Intelligence Head of Singapore Healthcare REIT Research

SEGMENT INSIGHTS

| 03 | REIT PROFILE ANALYSIS |

Two REITs Defining Singapore's Healthcare Real Estate Investment Market

PARKWAY LIFE REIT (SGX: C2PU) ASIA'S PREMIER HEALTHCARE REIT 17 CONSECUTIVE YEARS DPU GROWTH

| Portfolio Value | 9M 2025 Distributable Income | 9M 2025 Gross Revenue | FY2026 Singapore Rent Uplift |

| SGD 2.57 Billion (Sep 2025) | SGD 75.4M (+10.4% YoY) | SGD 117.3M (+8.2% YoY) | +24.4% YoY SGD 79.7M to SGD 99.2M (AEI completion) |

Parkway Life REIT, listed on the Singapore Exchange under the ticker C2PU, is one of Asia's largest listed healthcare REITs by asset size with a SGD 2.57 billion portfolio comprising three Singapore private hospitals and 71 nursing homes and care facilities across Japan and France as of September 2025. The REIT's Singapore portfolio Mount Elizabeth Hospital, Gleneagles Hospital, and Parkway East Hospital is leased under a 20.4-year master lease to Parkway Hospitals Singapore, a wholly owned subsidiary of IHH Healthcare Berhad, with the lease terms guaranteeing annual rent escalation of 2% to 3% until FY2025 and transitioning to a CPI-linked formula from FY2026, with Singapore representing 62.5% to 65% of total asset value per Q3 2025 reporting. In FY2026, aggregate rent from the Singapore hospitals is expected to increase 24.4% year-on-year from SGD 79.7 million to SGD 99.2 million following completion of the AEI at Mount Elizabeth Hospital as part of Project Renaissance, representing the most significant single-year Singapore hospital rental uplift in the REIT's history per Growbeansprout research. The REIT maintains a strong balance sheet with gearing at 35.8% and an interest coverage ratio of 8.9x, has secured a seven-year JPY loan to refinance one-third of 2026 maturities extending weighted average debt term from 2.8 to 3.2 years, and has no refinancing needs until October 2026 with 86% of interest rate exposure hedged. From 2007 to 2024, Parkway Life REIT's DPU grew approximately 136% from an annualised 6.32 cents to 14.92 cents in FY2024, maintaining 17 consecutive years of uninterrupted DPU growth.

FIRST REIT (SGX: AW9U) SOUTHEAST ASIAN DIVERSIFIED HEALTHCARE REIT

| Portfolio Value | Geographic Spread | Strategy | Yield Profile |

| SGD 1.12 Billion, 32 properties | 15 Indonesian hospitals, Singapore, Japan | Indonesia restructuring review + Japan nursing home expansion | Higher yield than Parkway Life; higher risk profile |

First REIT, listed on the Singapore Exchange under the ticker AW9U, owns 32 healthcare properties valued at SGD 1.12 billion spanning Indonesia, Singapore, and Japan, with 15 hospitals in Indonesia constituting the largest component of its portfolio by number and representing the primary source of geographic risk in the First REIT portfolio relative to the Singapore-anchored Parkway Life REIT model. Indonesia's private hospital real estate market, while presenting significant long-term healthcare demand growth driven by the country's 280 million population and expanding middle-income healthcare spending, carries regulatory, currency, and operational risk profiles that the IHH Healthcare triple-net lease structure at Parkway Life REIT's Singapore hospitals does not. First REIT's strategic focus on diversifying into Japan nursing homes a market with deep structural ageing demographics, high-quality regulatory oversight, and the JPY lease income that supplements the IDR-denominated Indonesian hospital income mirrors Parkway Life REIT's Japan nursing home growth strategy at a smaller scale. First REIT's higher distribution yield relative to Parkway Life REIT reflects the market's pricing of the Indonesian hospital and regulatory risk premium that distinguishes the two Singapore-listed healthcare REITs within the same asset class per ProsperUs analysis.

| Master Tenant | Lease Term | Rent Escalation | Occupancy |

| Parkway Hospitals Singapore (IHH Healthcare subsidiary) | 20.4 years renewed 2021 to December 2042 | 2-3% annual until FY2025; CPI-linked from FY2026 | 100% committed REIT bears no property tax or insurance |

The three Singapore private hospitals owned by Parkway Life REIT Mount Elizabeth Hospital at Orchard, Gleneagles Hospital at Napier Road, and Parkway East Hospital at Marine Parade constitute the highest-quality healthcare real estate in Southeast Asia, collectively serving as the primary private hospital destinations for Singapore's domestic private healthcare patients, medical tourists from across ASEAN, and international patients from the Middle East and South Asia who travel to Singapore specifically for the quality and specialisation of IHH Healthcare's clinical programmes. All three hospitals enjoy 100% occupancy with Parkway Life REIT not bearing property tax or insurance costs due to the triple-net lease structure, creating a net income profile that is closest in character to the NHS-backed triple-net primary care REITs in the UK per lease structure comparison. The FY2026 rent uplift of 24.4% year-on-year from SGD 79.7 million to SGD 99.2 million following completion of the Mount Elizabeth AEI Project Renaissance expanding the hospital's diagnostic and treatment capacity demonstrates the direct linkage between Singapore private hospital capital investment and rental income growth that the REIT's master lease structure translates into DPU growth for unitholders.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from Parkway Life REIT and First REIT investor disclosures, DBS Vickers analysis, Growbeansprout research, and verified trade press.