| TROVIEW INTELLIGENCE | Dental and Specialty Clinic Real Estate Market | Q2 2026 |

By Geography - By Specialty - By Ownership Model - By Facility Size

The global dental services market was valued at USD 472.24 Billion in 2025 with dental clinics accounting for approximately 69% of total end-use market share, approximately 3.5 billion people are affected by oral diseases globally per WHO data, North America led the market with approximately 47% revenue share and the United States dental services market alone valued at USD 174.91 Billion in 2025, Asia Pacific is growing at a 7.2% CAGR as the fastest-growing region and is projected to reach USD 202.75 Billion by 2035, cosmetic dentistry is growing at the fastest CAGR of 7.8% within the dental services market per verified research data, and the UAE private healthcare sector exceeded AED 75 Billion in 2024 and is projected to grow at 7% annually through 2030 per Dubai Economy and Tourism verified data.

MARKET SYNOPSIS

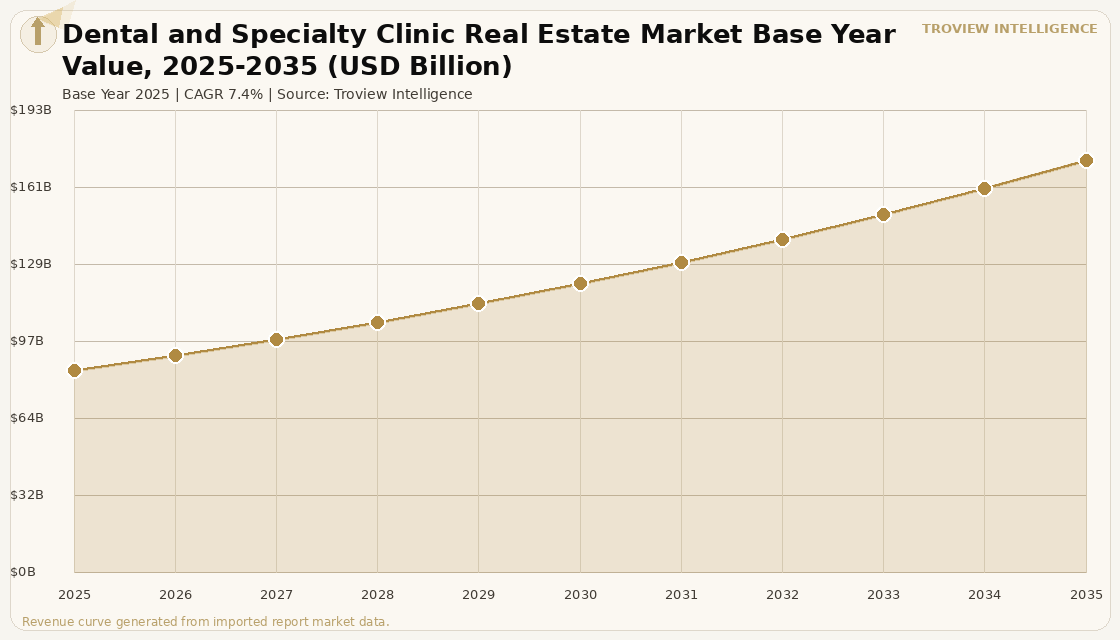

The global dental and specialty clinic real estate market size was USD 84.62 Billion in 2025 and is expected to register a revenue CAGR of 7.4% during the forecast period, reaching USD 172.38 Billion by 2035. The dental and specialty clinic real estate market encompasses the physical clinic infrastructure, leasehold and freehold properties, purpose-built medical facility developments, and healthcare real estate investment trust assets that house outpatient dental practices, orthodontic and cosmetic dental centres, multi-specialty dental hospitals, dermatology and aesthetics clinics, ophthalmology centres, physiotherapy and rehabilitation facilities, and specialist medical consulting suites across all global geographies. Dental clinics accounted for approximately 69% of the broader dental services market end-use revenue in 2024 per verified global proptech market data, serving the global population across general dentistry, implantology, orthodontics, and cosmetic dental procedures. The 2025 market estimate is grounded in verified service and facility revenues: the global dental services market was valued at USD 472.24 Billion in 2025 per Acumen Research and Consulting verified data, with approximately 3.5 billion people affected by oral diseases globally per WHO data, dental implants representing 22% of total dental services market share in 2025, and cosmetic dentistry growing at 7.8% CAGR as the fastest-growing service segment per Toward Healthcare verified market data. The global dental clinic market by clinic-specific revenue segment was valued at USD 377.8 Billion by end-user clinic revenue in 2025 per verified market research data. For instance, in June 2025, Inamdar Multispeciality Hospital in Pune, India opened a 24/7 Dental and Face Surgery Clinic offering emergency trauma care, advanced dental implantology, and oral-maxillofacial surgery, confirming the trend of multi-specialty hospital operators integrating dental facilities as anchor outpatient services within comprehensive healthcare campuses. These are some of the key factors driving revenue growth of the market.

North America dominated the global dental and specialty clinic real estate market in 2025, holding approximately 47% of total dental services market revenue, with the United States dental services market valued at USD 174.91 Billion and the US generating approximately 3 million dental implant patients annually per verified market data. The United States dental services market alone is projected to grow from USD 174.91 Billion in 2025 to USD 270.57 Billion by 2034 at a CAGR of 5.09% per verified global proptech market data. The US market is further distinguished by the rapid growth of dental service organisations chain-affiliated dental practice groups that provide non-clinical business support to dentist-owned practices with Heartland Dental, Aspen Dental, and Dental365 representing the three largest DSO platforms expanding through new clinic openings and practice affiliations. Oxford Finance LLC, a specialty finance firm, closed a USD 107 Million senior credit facility to Specialty Dental Brands in 2025 for orthodontics, pediatric dentistry, and oral surgery expansion, confirming institutional capital's sustained appetite for dental clinic real estate and practice finance. Asia Pacific generated approximately 22% of total dental services market revenue in 2025 at USD 103.89 Billion per Acumen Research data and is projected to reach USD 202.75 Billion by 2035 at a 7.2% CAGR the fastest global regional growth rate driven by rapidly expanding middle-class populations in China, India, and Southeast Asia and by increasing awareness of preventive and cosmetic dental care.

However, the global dental and specialty clinic real estate market faces structural constraints that limit sustainable revenue growth across multiple markets. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation and dental materials supply chain cost pressures including titanium implant components, orthodontic clear aligner materials, and ceramic crown blanks that are subject to global logistics and energy cost pass-through that increase operating costs for dental clinic operators who cannot easily pass through input cost increases to patients on fixed insurance reimbursement schedules. Regulatory compliance costs for dental clinic licensing and certification including DHA licensing in Dubai at AED 10,000 to 15,000 per practitioner, NABIDH electronic medical record system compliance, and infection control certification requirements represent significant upfront and recurring expenditure that deters single-practitioner clinic openings in high-regulatory markets including the UAE while favouring well-capitalised multi-location operators. Skilled dental specialist shortages in emerging markets including the Middle East, India, and Southeast Asia limit the throughput of licensed dental clinic facilities that have the physical real estate capacity to serve higher patient volumes but cannot recruit sufficient implantologists, orthodontists, and cosmetic dentists to fill available chair time. These factors substantially limit global dental and specialty clinic real estate market growth over the forecast period.

Dental and specialty clinic real estate has become one of the most attractive healthcare real estate investment categories for institutional capital in 2025, for two structural reasons. First, dental clinics are among the stickiest commercial tenants in healthcare real estate: a fully fitted out dental clinic with installed chair units, plumbing, sterilisation room, and X-ray shielding has moving costs that effectively make the operator a captive tenant for 7 to 15 years, providing landlords with above-market lease security. Second, the demographic tail wind 3.5 billion people with oral disease globally, cosmetic dentistry growing at 7.8% CAGR, dental implant demand growing at 9.8% CAGR means procedure volume growth is not dependent on economic cycles in the same way that other retail or office real estate demand is. The DSO consolidation wave in the United States has accelerated this dynamic by creating multi-location tenants who sign institutional leases across their clinic networks. Oxford Finance's USD 107 million credit facility to Specialty Dental Brands is a signal of how the capital market has institutionalised. In Dubai, a DHA-approved dental clinic in Jumeirah produces returns of 10 to 20% annually per verified market data. That is not a coincidence. That is the product of constrained clinic real estate supply meeting growing cosmetic dental demand from one of the world's wealthiest per-capita patient populations." Troview Intelligence Head of Global Dental and Specialty Clinic Real Estate Research

SEGMENT INSIGHTS

By Specialty

General dentistry and preventive care specialty is expected to account for a significantly large revenue share in the global dental and specialty clinic real estate market during the forecast period.

Based on specialty, the global dental and specialty clinic real estate market is segmented into general dentistry and preventive care, dental implantology, orthodontics and clear aligner treatment, cosmetic and aesthetic dentistry, oral and maxillofacial surgery, and paediatric dentistry. General dentistry dominates total clinic revenue by patient volume, as routine examinations, prophylaxis, fillings, and root canal treatments generate the recurring patient visit frequency that sustains clinic occupancy and revenue throughout the year. Dental implants represented the highest revenue share of approximately 21% to 22% of total dental services market revenue in 2025, reflecting the premium per-procedure value of implant treatment that makes implantology the single highest revenue-intensity service in the dental specialty clinic market. Cosmetic dentistry is expected to register the fastest CAGR of 7.8% during the forecast period per Toward Healthcare verified data, driven by social media influence on smile aesthetics, the growing availability of minimally invasive cosmetic procedures including composite bonding and veneers, and increasing patient willingness to self-fund aesthetic procedures outside insurance coverage.

By Facility Size

Mid-sized multi-chair dental clinic facility segment is expected to account for a significantly large revenue share in the global dental and specialty clinic real estate market during the forecast period.

Based on facility size, the global dental and specialty clinic real estate market is segmented into single-chair solo practice clinics, mid-sized multi-chair group practices with 3 to 10 chairs, large multi-specialty dental centres with 10 to 30 chairs, and hospital-integrated dental departments. Mid-sized multi-chair group practices dominate total clinic real estate revenue globally, combining the patient volume capacity required for financial sustainability with the specialty breadth general dentist alongside orthodontist and implantologist that enables cross-referral within the clinic and higher capture of each patient's total lifetime dental spend. Large multi-specialty dental centres are expected to register the fastest CAGR during the forecast period, as dental service organisation expansion, private equity consolidation of fragmented dental markets, and the emergence of dental tourism destinations including Dubai Healthcare City attract investment into large-format dental facilities capable of serving multiple patient demographics simultaneously.

By Ownership Model

Private practice and dental service organisation ownership model is expected to account for a significantly large revenue share in the global dental and specialty clinic real estate market during the forecast period.

Based on ownership model, the global dental and specialty clinic real estate market is segmented into independent private practice owned by individual dentist operators, dental service organisations providing non-clinical business support to affiliated practices, multi-specialty medical group practices incorporating dental as an integrated service, hospital-owned outpatient dental departments, and investor-owned clinic real estate under professional management agreements. Dental service organisations dominated US clinic real estate expansion in 2025, with Heartland Dental, Aspen Dental Management, and Pacific Dental Services collectively adding dozens of new de novo clinic locations and affiliations annually per verified company data. The DSO segment is expected to register the fastest CAGR in global dental clinic real estate during the forecast period, as the financial structure where DSO provides capital, management systems, and marketing while the practitioner retains clinical autonomy enables faster geographic expansion than traditional single-owner practice development.

REGIONAL ANALYSIS

NORTH AMERICA

| US Dental Services 2025 | US Dental Implant Patients (2024) | Oxford Finance Facility (2025) | US Dental Services CAGR to 2034 |

| USD 174.91 Billion | ~3 million annually | USD 107M to Specialty Dental Brands | 5.09% |

North America is the global dental and specialty clinic real estate market leader, driven by the United States' combination of advanced dental technology adoption, strong insurance coverage for preventive and basic dental procedures, and the accelerating DSO consolidation wave that is professionalising clinic real estate management across the fragmented US dental market. Heartland Dental, the largest US DSO, continued expanding its network through 38 new de novo dental offices opened in high-growth communities and 13 affiliations in the most recent completed fiscal year per verified market data verified dental industry data, creating a tenant base of consistent quality that institutional healthcare REIT landlords actively pursue. The cosmetic dentistry segment is the fastest-growing within North America at an estimated CAGR of 7.8%, supported by approximately 3 million dental implant patients annually in the United States, the growing penetration of clear aligner orthodontic treatment across adult patients who would not have sought orthodontics at traditional braces pricing, and the expanding use of AI-powered diagnostic imaging that improves treatment planning and increases patient case acceptance rates. Oxford Finance LLC's USD 107 Million senior credit facility to Specialty Dental Brands, a DSO focused on orthodontics, paediatric dentistry, and oral surgery, confirmed the depth of institutional dental specialty finance available in the US market in 2025.

ASIA PACIFIC

| APAC Dental Services 2025 | APAC CAGR (to 2035) | WHO Global Oral Disease Burden | India AI Dental Tech (Aug 2025) |

| USD 103.89 Billion (22% share) | 7.2% fastest global CAGR | 3.5 billion people affected globally | Laxmi Dental acquired AI Dent stake |

Asia Pacific is the fastest-growing global dental and specialty clinic real estate market region, projected to grow at 7.2% CAGR from USD 103.89 Billion in 2025 to USD 202.75 Billion by 2035 per Acumen Research verified market data, driven by rapidly expanding middle-class populations in China and India who are accessing dental care at scale for the first time, increasing awareness of oral hygiene among younger demographics stimulated by social media and corporate wellness programmes, and government initiatives to expand dental coverage in national health insurance frameworks. India's dental technology sector is advancing rapidly, with Laxmi Dental Limited announcing the acquisition of a majority stake in AI Dent in August 2025 to improve its digital dentistry AI capabilities and bring AI-powered imaging and diagnostic tools to dental offices across India per verified market data dental service market data. Japan's dental market benefits from one of the world's highest elderly population concentrations that generates sustained demand for restorative dentistry, dental prosthetics, and implant procedures as the 70-plus cohort requires comprehensive tooth replacement across extended lifetimes. Southeast Asia with Thailand, Malaysia, and Singapore as established dental tourism destinations is experiencing clinic real estate investment from regional dental groups who serve both domestic patients and international dental tourism visitors seeking quality dental care at materially lower cost than their home markets.

MIDDLE EAST UAE AED

| UAE Private Healthcare 2024 | UAE Dental Clinic Market 2025 | Dubai Clinic Returns | DHA Licensed Facilities Growth |

| AED 75 Billion (+7% p.a. to 2030) | USD 207.71 Million (5.54% CAGR) | 10-20% annually for dental/cosmetic | 45% growth in 5 years 4,482 private facilities (DHA 2022) |

The Middle East is a high-growth dental and specialty clinic real estate market, led by the UAE where the private healthcare sector exceeded AED 75 Billion in 2024 and is projected to grow at 7% annually through 2030 per Dubai Economy and Tourism verified data. The UAE dental clinic industry market was valued at USD 207.71 Million in 2025 growing at a 5.54% CAGR per verified industry research, with Dubai and Abu Dhabi dominating as the primary market hubs due to their high population density, concentration of affluent multinational residents, and robust medical tourism infrastructure. According to Dubai Health Authority statistics released in 2022, the UAE had experienced a 45% growth in private healthcare facilities in the preceding five years, reaching 4,482 medical facilities across the private sector the majority of which are specialty clinic formats including dental, aesthetic, and dermatology practices. Dubai-specific dental clinic investment offers returns of 10 to 20% annually, with dental and cosmetic clinics among the most profitable healthcare real estate investment categories in the city per Mokza Healthcare Consultancy verified investment market data, driven by the combination of high-income international patient demographics, a cosmetic dental tourism inflow that generates per-procedure values materially above insurance reimbursement schedules, and a regulatory environment that supports quality clinical standards while enabling streamlined clinic setup through Dubai Healthcare City's free zone licensing framework.