By Emirate - By Specialty - By Regulatory Zone - By Ownership

Emirate Spotlights: Dubai - Abu Dhabi - Sharjah

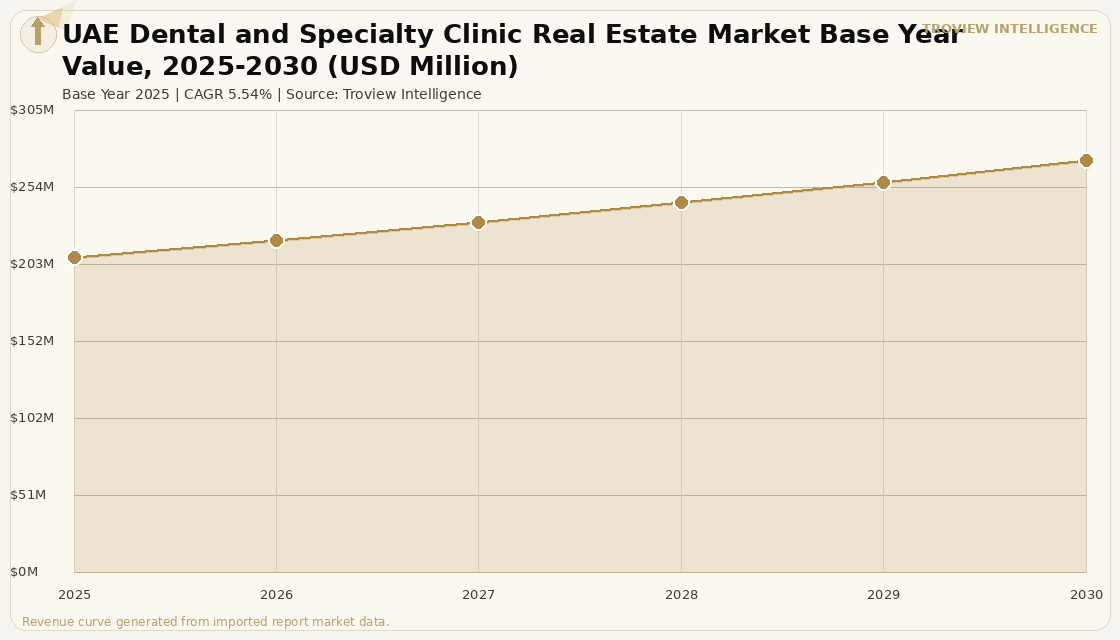

The UAE dental clinic industry was valued at USD 207.71 Million in 2025 growing at a 5.54% CAGR, the UAE private healthcare sector exceeded AED 75 Billion in 2024 projected to grow at 7% annually through 2030, the Dubai Health Authority confirmed a 45% growth in private healthcare facilities in five years to reach 4,482 facilities in 2022, over 70% of UAE residents express interest in cosmetic dental procedures per verified industry data, and UAE cosmetic dentistry is valued at approximately AED 1.8 Billion per Ken Research verified UAE dental service organisation market data.

MARKET SYNOPSIS

The UAE dental and specialty clinic real estate market size was USD 207.71 Million in 2025 and is expected to register a revenue CAGR of 5.54% during the forecast period, reaching USD 271.98 Million by 2030. The UAE dental clinic industry is a moderately concentrated market with a few large branded networks alongside numerous smaller independent clinics, with Dubai and Abu Dhabi dominating as the primary market hubs due to their higher population density, greater concentration of affluent individuals, and robust healthcare infrastructure that includes both DHA-regulated mainland clinics and Dubai Healthcare City free zone facilities. The UAE private healthcare sector exceeded AED 75 Billion in 2024 and is projected to grow at 7% annually through 2030 per Dubai Economy and Tourism verified data, with private healthcare investment driven by the UAE's growing population, expanding expatriate resident base, and government strategy to position the country as a hub for medical tourism, wellness innovation, and digital healthcare excellence. According to Dubai Health Authority statistics, the UAE experienced a 45% growth in private sector healthcare facilities in the five years preceding 2022, reaching 4,482 private sector medical facilities that collectively comprise the licensed outpatient clinic estate in which dental practices constitute a significant and growing segment. The UAE cosmetic dentistry market is valued at approximately AED 1.8 Billion per Ken Research UAE dental service organisation market data, with over 70% of UAE residents expressing interest in cosmetic dental procedures a penetration rate that reflects the combination of high disposable incomes, social media influence on appearance consciousness, and the availability of international-standard cosmetic dental services across Dubai and Abu Dhabi's well-developed private clinic networks. For instance, the Dubai Health Authority's Regulation of Dental Services Provision in the Emirate of Dubai 2021 set detailed requirements on infection prevention, sterilisation, facility design, staff qualifications, and ongoing compliance audits for all Dubai-licensed dental clinics, establishing a quality regulatory framework that has elevated the clinical standard of UAE dental clinic facilities and increased the investment required for compliant clinic setup. These are some of the key factors driving revenue growth of the market.

The UAE dental and specialty clinic real estate market is structured through a dual licensing framework: Dubai Health Authority-regulated mainland clinics that can serve patients across all residential and commercial areas of Dubai without geographic restriction, and Dubai Healthcare City Authority-regulated free zone clinics within the purpose-built DHCC healthcare district. Since 2021, 100% foreign ownership is available for most healthcare activities on the UAE mainland, removing a structural barrier to international dental group investment in Emirates other than Dubai's established free zones. Clinic real estate costs in Dubai are highly location-sensitive: premium areas including Business Bay, Jumeirah, and Downtown Dubai command AED 200 to 300 per square foot annually in clinic lease costs, mid-range areas including Al Barsha and Dubai Healthcare City command AED 150 to 200 per square foot, and more affordable zones including Al Qusais and Dubai Silicon Oasis range from AED 100 to 150 per square foot per verified industry cost analysis. DHA-approved specialty clinics including dental and dermatology generate established clinic investment returns of 10 to 20% annually per Mokza Healthcare Consultancy verified investment market data, with dental and cosmetic aesthetic clinics consistently among the most profitable healthcare real estate investment categories in Dubai given the combination of high average procedure values, low capital intensity relative to surgical specialties, and the sustained demand from Dubai's internationally diverse, high-income resident and visitor population.

However, the UAE dental and specialty clinic real estate market faces structural constraints that limit the pace of new clinic supply growth. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation and dental material supply chain cost pressures that increase operating costs for UAE dental clinics whose consumable costs including imported titanium implant components, ceramic crowns, orthodontic brackets, and clear aligner materials are subject to global freight cost pass-through. UAE dental clinic regulatory compliance costs are substantial: DHA professional licensing costs AED 10,000 to 15,000 per practitioner, the DHA approvals and eligibility test fees add AED 5,000 to 7,000, and specialty clinic setup costs including fit-out, equipment, and licensing range from AED 800,000 to AED 2,000,000 or more for well-equipped dental specialty centres per Arnifi verified UAE dental clinic cost analysis. These upfront investment requirements favour well-capitalised multi-location operators and private equity-backed dental networks over individual practitioner startups, concentrating market growth in the branded dental group segment. These factors substantially limit UAE dental and specialty clinic real estate market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "The UAE dental clinic market in 2025 is one of the most analytically interesting in global healthcare real estate. You have a country of approximately 10 million people 90% expatriate by population with one of the world's highest per-capita incomes, an overwhelming preference for private healthcare, and over 70% of the population expressing interest in cosmetic dental procedures. The cosmetic dentistry penetration potential alone AED 1.8 billion market at current pricing, growing with every new expatriate arrival from high-income source countries makes UAE dental clinic real estate structurally attractive for institutional investors. The DHA regulatory framework has done something most healthcare regulators fail to do: it has raised clinical quality standards high enough to protect patients and establish UAE dental care as internationally competitive, while streamlining the licensing process enough to allow qualified international operators to set up efficiently. The result is a market where a DHA-approved dental clinic in Jumeirah produces 10 to 20% annual returns on a proven 10-month breakeven model. That is a compelling healthcare real estate investment case at any interest rate environment." Troview Intelligence Head of UAE Dental and Specialty Clinic Real Estate Research

SEGMENT INSIGHTS

Three Emirates Shaping UAE Dental Clinic Real Estate

| Private Healthcare Sector | DHA Private Facilities (2022) | Dental Clinic Setup Cost | Clinic Investment Returns |

| AED 75bn+ (7% p.a. to 2030) | 4,482 private facilities (+45% in 5 yrs) | AED 800K - AED 2M+ (specialty) | 10-20% annually for dental/cosmetic |

Dubai is the UAE's dominant dental and specialty clinic real estate market, hosting the majority of the country's private dental clinic estate across both DHA-regulated mainland locations and the Dubai Healthcare City free zone, with demand driven by the city's 3.6 million permanent residents of whom approximately 90% are expatriates with cultural backgrounds that place high value on dental aesthetics and preventive oral care. Dubai's dental clinic real estate market is characterised by strong location-dependent returns: a DHA-approved dental clinic focused on cosmetic dentistry and orthodontics in Downtown Dubai or Jumeirah can break even within 10 months and generate 10 to 20% annual returns per Mokza Healthcare Consultancy verified data, with 65% of revenue coming from aesthetic dentistry packages at AED 80 to 200 per qualified patient inquiry cost via Google Ads benchmarks per healthcare marketing industry data. Dubai Healthcare City is the preferred location for internationally-branded dental groups seeking free zone benefits: 100% foreign ownership, DHCR licensing framework, proximity to Mediclinic City Hospital and the broader DHCC healthcare campus, and an established international patient population within the free zone. The standard dental clinic setup cost in Dubai ranges from AED 300,000 to AED 700,000 for a basic clinic to AED 800,000 to AED 2,000,000 or more for specialty dental centres with advanced digital dentistry equipment, implant surgery suites, and orthodontic treatment rooms per Arnifi and Felix Happich verified UAE dental clinic cost analyses.

| Regulatory Authority | Public Dental Programme | Key Operators | Growth Driver |

| HAAD and DOH (Dept of Health) | Free dental services for Emiratis and GCC elderly (Aug 2022 EHS) | Al Bustan (3 clinics), Thumbay, LLH | Government infrastructure investment and growing expat base |

Abu Dhabi is the UAE's second-largest dental and specialty clinic real estate market, regulated by the Department of Health and the former Health Authority Abu Dhabi, with significant government investment in public healthcare infrastructure that complements a growing private dental clinic sector serving the emirate's multinational resident base and increasing medical tourism visitors. Emirates Health Services launched free dental services through primary health centres for Emiratis and GCC elderly citizens in August 2022 per verified UAE dental care market data, expanding public access to preventive dental care while simultaneously highlighting the private clinic opportunity for premium cosmetic, implant, and specialist dental procedures not covered by public programmes. The Abu Dhabi dental clinic market is growing through a combination of established multi-clinic operators including Al Bustan Dental Clinics which holds three Abu Dhabi clinics and was identified alongside TDS as a platform well-positioned for M&A expansion in complementary UAE catchment areas per Insights10 UAE dental care market analysis and international dental groups attracted by Abu Dhabi's government investment in healthcare infrastructure and its concentration of government employees, oil sector professionals, and diplomatic community residents with premium dental care expectations.

| Market Character | Patient Demographics | Real Estate Cost Advantage | Regulatory Authority |

| Price-competitive, family-focused dental | Middle-income Indian, Pakistani, Arab expats | Materially below Dubai and Abu Dhabi | Respective emirate health authority (non-DHA) |

Sharjah is the UAE's emerging third dental clinic real estate market, serving a large middle-income expatriate population with disposable incomes positioned below Dubai's luxury dental market and above the unaffordable price point of premium cosmetic dental centres, generating demand for quality general and restorative dental care at competitive price points that mid-range family dental clinics are well-positioned to serve. Sharjah's lower real estate costs relative to Dubai and Abu Dhabi with clinic rental rates materially below Dubai's AED 150 to 300 per square foot range make it an attractive entry market for dental clinic operators seeking to establish an initial UAE presence before expanding into more expensive Dubai locations. A healthcare investor feasibility study for a mid-range family dental clinic in a Sharjah residential area targeting locals and middle-income expatriates demonstrated viable business economics per Aviaan verified case study data, confirming that Sharjah's patient demographic primarily Indian, Pakistani, and Arab expatriate families represents a sustainable base for general and paediatric dental practice. Sharjah is notable in the UAE regulatory context for its alcohol prohibition, which does not affect dental clinic economics but does affect the character of its patient demographics relative to the more cosmopolitan resident base of Dubai and Abu Dhabi.