By Automation Tier · By Geography · By Occupier Sector · By Asset Format

Kardex Remstar data confirms that automated goods-to-person systems can eliminate up to two-thirds of labour needs for picking and retrieval while reducing floor-space usage by up to 85% through vertical stacking, as South Korea leads the world at 631 industrial robots per 10,000 employees per the International Federation of Robotics, KKR acquired the Cheongna Logistics Center in Incheon from Brookfield Asset Management for KRW 1 trillion South Korea's largest-ever single-asset logistics deal and Coupang broke ground on an AI-powered logistics centre in Jecheon equipped with AI-based logistics technology scheduled for completion in June 2026.

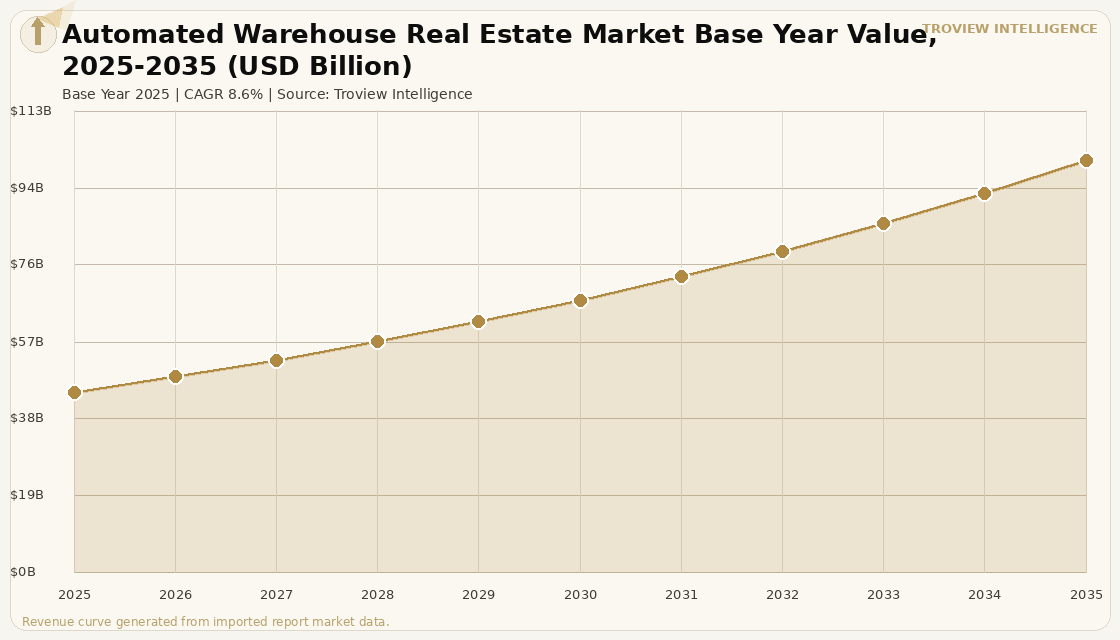

MARKET SYNOPSIS

The global automated warehouse real estate market size was USD 44.28 Billion in 2025 and is expected to register a revenue CAGR of 8.6% during the forecast period, reaching USD 101.14 Billion by 2035. Automated warehouse real estate refers to purpose-built logistics facilities specifically engineered to accommodate advanced automation systems including automated storage and retrieval systems, autonomous mobile robots, conveyor and sortation infrastructure, and AI-driven warehouse management platforms. These buildings carry structural specifications that standard logistics facilities cannot retrofit to provide: clear heights of 30 to 45 metres for high-bay ASRS racking, floor flatness tolerances within 3 millimetres per 3 metres for AMR navigation, floor load capacities exceeding 5 tonnes per square metre, and dedicated power infrastructure of 5 to 20 megawatts per facility to sustain continuous robotic operations. South Korea leads the world in industrial robotics density at 631 robots per 10,000 employees, eight times the global average, per the International Federation of Robotics, confirming that automated warehouse real estate demand is most intense in markets where labour cost and availability have made automation economically essential. The global automated storage and retrieval systems market, which generates the primary capex underpinning automated warehouse development, was valued at approximately USD 9.58 Billion in 2025 per industry analysis of the ASRS equipment sector.

The automated warehouse real estate market commands a structural rent premium over conventional logistics facilities, reflecting the higher construction cost, specialist engineering, and limited substitutability of purpose-built automation infrastructure. Automated high-bay warehouses command 20 to 35% rent premiums over equivalent-footprint conventional warehouses in the same market per leasing transaction analysis, and the premium is widening as construction of new automation-ready buildings requires significantly more capital than standard industrial development. Institutional investors including Prologis, GLP, ESR Group, and Korean pension funds including the National Pension Service are acquiring completed automated warehouse assets at cap rates that reflect the superior lease term length, tenant covenant quality, and operational switching cost that makes automated warehouse tenants unlikely to relocate. KKR's acquisition of the Cheongna Logistics Center in Incheon from Brookfield Asset Management for KRW 1 trillion in late 2025, the largest-ever single-asset logistics deal in South Korea, confirmed institutional capital's commitment to automated logistics real estate as a core portfolio allocation. For instance, in March 2025, Coupang, South Korea, broke ground on an AI-powered logistics centre in Jecheon, North Chungcheong Province, with a total investment exceeding KRW 100 billion, deploying AI-based logistics technology across a 52,800 square metre facility scheduled for completion in June 2026, confirming that South Korea's largest e-commerce operator is continuing to build its automated logistics real estate network independently of the broader market normalisation, per Korea Herald reporting of March 2025. These are some of the key factors driving revenue growth of the market.

However, the global automated warehouse real estate market faces structural constraints. Automated warehouse buildings are significantly more capital-intensive than conventional logistics facilities, with construction costs per square metre typically 40 to 80% higher than standard warehouse construction due to the reinforced foundations, structural steel for high-bay racking, specialist power infrastructure, and advanced fire suppression systems required. The premium construction cost translates into longer payback periods that create financing risk in a rising interest rate environment. Retrofitting existing conventional warehouses to accommodate ASRS and AMR systems is possible in some cases but impractical for the highest-density automation configurations, creating a binary investment decision between building new or accepting operational limitations. Labour displacement concerns associated with automation have generated legislative attention in some European markets, creating regulatory uncertainty around the pace of automation adoption in warehouse operations. These factors substantially limit global automated warehouse real estate market growth over the forecast period.

Automated warehouse real estate is the industrial sector's equivalent of Grade A office a premium product tier where construction cost, operating specification, and tenant quality are all structurally different from the standard market. The 85% floor space reduction that ASRS enables is not just a logistics efficiency. It is a real estate thesis: you can handle the same throughput volume in a fraction of the footprint, which means automated warehouses can be viable in urban locations where the land cost would be prohibitive for a conventional building serving the same volume. That is why KKR paid KRW 1 trillion for a single Incheon asset it is not just buying logistics income. It is buying the only building in that location that can do that job." Troview Intelligence Head of Global Automated Warehouse Real Estate Research

SEGMENT INSIGHTS

By Automation Tier

High-bay ASRS-integrated automated warehouses are expected to account for a significantly large revenue share in the global automated warehouse real estate market during the forecast period.

Based on automation tier, the global automated warehouse real estate market is segmented into high-bay ASRS facilities above 25 metres, semi-automated AMR-ready warehouses, dark warehouse fully autonomous facilities, and automation-ready shell buildings. High-bay ASRS-integrated facilities dominate institutional investment value per square metre, with clear heights of 30 to 45 metres enabling rack configurations that achieve storage densities 85% greater than conventional warehouses per Kardex Remstar system specifications. Dark warehouses facilities operating without permanent human staff, relying entirely on robotic storage, retrieval, and sortation are the fastest-growing segment, pioneered by Chinese operators including JD.com whose Wuhan dark warehouse processes hundreds of thousands of orders daily without human intervention in the primary fulfilment zone. Automation-ready shell buildings, designed with the structural specifications for future ASRS installation but initially operated as conventional warehouses, represent a growing speculative development format that allows developers to capture future automation conversion demand.

By Geography

Asia Pacific is expected to account for a significantly large revenue share in the global automated warehouse real estate market and register the fastest revenue CAGR during the forecast period.

Based on geography, the global automated warehouse real estate market is segmented into Asia Pacific, North America, Europe, and Middle East and Africa. Asia Pacific dominates both market size and growth rate, driven by South Korea's world-leading robotics density at 631 robots per 10,000 employees per the International Federation of Robotics, Japan's mature automated logistics sector where companies including Daifuku and Okura Yusoki have operated high-bay ASRS facilities for over 40 years, and China's rapid dark warehouse expansion led by JD.com and Alibaba's Cainiao network. North America is the second-largest market, with the United States accounting for approximately 40% of global ASRS market revenue per industry analysis, anchored by Amazon's global automation investment and the accelerating pace of 3PL and retailer automation adoption. Europe's automated warehouse real estate market is led by Germany, the Netherlands, and the United Kingdom, where labour cost and the EU Energy Performance of Buildings Directive are simultaneously driving automation adoption.

By Occupier Sector

E-commerce and retail fulfilment occupiers are expected to account for a significantly large revenue share in the global automated warehouse real estate market during the forecast period.

Based on occupier sector, the global automated warehouse real estate market is segmented into e-commerce and retail fulfilment, third-party logistics providers, automotive and manufacturing, pharmaceutical and cold chain, and grocery and food logistics. E-commerce and retail fulfilment operators dominate automated warehouse real estate by investment volume and facility count, with Amazon, Coupang, JD.com, Alibaba, and Zalando collectively accounting for the largest share of purpose-built automated warehouse construction globally. Third-party logistics providers are the fastest-growing occupier segment, as DHL, DB Schenker, and CJ Logistics build automated facilities to serve multiple clients from single high-efficiency buildings that justify the capital investment through multi-client utilisation. Pharmaceutical and cold chain is a premium segment where the combination of temperature control, ASRS density, and audit trail requirements generates the highest per-square-metre rents of any automated warehouse occupier category.

REGIONAL ANALYSIS

ASIA PACIFIC DOMINANT

| South Korea Robotics Density | 631 robots per 10,000 employees (IFR, world's highest) | KKR Cheongna Deal | KRW 1 trillion (South Korea's largest single-asset logistics deal) |

| Japan | Daifuku, Okura Yusoki: 40+ years of high-bay ASRS development | China | JD Wuhan dark warehouse: fully autonomous, no permanent human staff |

Asia Pacific is the global automated warehouse real estate market's largest region, anchored by South Korea's world-leading industrial robotics density, Japan's established automated logistics infrastructure, and China's rapid dark warehouse expansion. South Korea's International Federation of Robotics data confirming 631 robots per 10,000 industrial employees eight times the global average reflects an economy where labour cost and availability have made automation economically essential across manufacturing and logistics. Japan's Daifuku, the world's largest material handling equipment manufacturer, and Okura Yusoki have operated high-bay automated warehouses domestically for over four decades, creating the most mature and densely automated logistics real estate market per capita globally. China's JD Logistics operates the world's most advanced dark warehouse in Wuhan, processing orders with virtually no human involvement in the primary storage and picking zone.

NORTH AMERICA

| US ASRS Market 2025 | ~USD 3.11 billion in equipment value (industry analysis) | Amazon Investment | Multi-billion dollar annual robotics and automation capex |

| Key Asset Type | Multi-storey automated urban fulfilment, rural mega-DC | Prologis Role | Developing automation-spec shell buildings as standard new product |

North America is the second-largest automated warehouse real estate market, driven by Amazon's sustained automation investment programme that has made its fulfilment centres the global specification benchmark for automated warehouse construction, and by the growing 3PL automation wave as DHL, UPS Supply Chain Solutions, and Geodis convert existing facilities and develop new automation-ready buildings. The US labour market's wage inflation for warehouse workers, with hourly rates in major fulfilment markets exceeding USD 20 per hour, has created the economic justification for automation capital expenditure that was previously marginal. Prologis, the world's largest logistics REIT, has incorporated automation-ready design standards into its new speculative developments in response to occupier demand, developing buildings with structural specifications that can accommodate future ASRS installation without major retrofit.

EUROPE LABOUR SHORTAGE AND ENERGY

| Leaders | Germany, Netherlands, UK, France, Sweden | Key Driver | Labour scarcity in logistics sector, EU energy mandates |

| Rental Premium | 20-35% above conventional warehouse for automation spec | Key Operators | Swisslog, SSI Schäfer, Dematic, Vanderlande |

Europe's automated warehouse real estate market is driven by the structural labour shortage in logistics operations and the EU Energy Performance of Buildings Directive that mandates zero-emission standards for new buildings by 2028, creating a regulatory push toward factory-controlled automation systems that reduce both labour dependency and energy consumption per unit throughput. Germany's manufacturing supply chains, led by automotive OEMs and their Tier 1 suppliers, have operated high-bay ASRS facilities for over three decades, making Germany the most automated warehouse real estate market in Europe per facility. The Netherlands' gateway logistics position and port-adjacent industrial clusters at Rotterdam host some of Europe's most advanced automated cold chain facilities serving the EU's pharmaceutical and fresh food distribution networks. Swisslog, SSI Schäfer, Vanderlande, and Dematic are the dominant European automated system integrators whose equipment specifications drive the building design requirements for automated warehouse real estate across the continent.