By District - By Hotel Tier - By Guest Segment - By Ownership Type

Districts: Eixample - Gothic Quarter - El Born - Barceloneta - Gracia

Barcelona's hotel supply grew only 0.1% year-on-year in the year to May 2025 adding just 462 rooms to a market of over 75,000 as the city's hotel licence moratorium in central districts maintained the structural ADR premium that drove H1 2025 ADR to EUR 195.5, RevPAR to EUR 149.80, and H1 2025 GOP margin to 45.1% with 66.9% GOP flow through, while institutional investors concentrated EUR 518 million of hotel investment in the city with boutique hotel licences in Eixample, Gothic Quarter, and Born commanding the scarcest and most capital-intensive transactions in Spain's hotel investment market.

MARKET SYNOPSIS

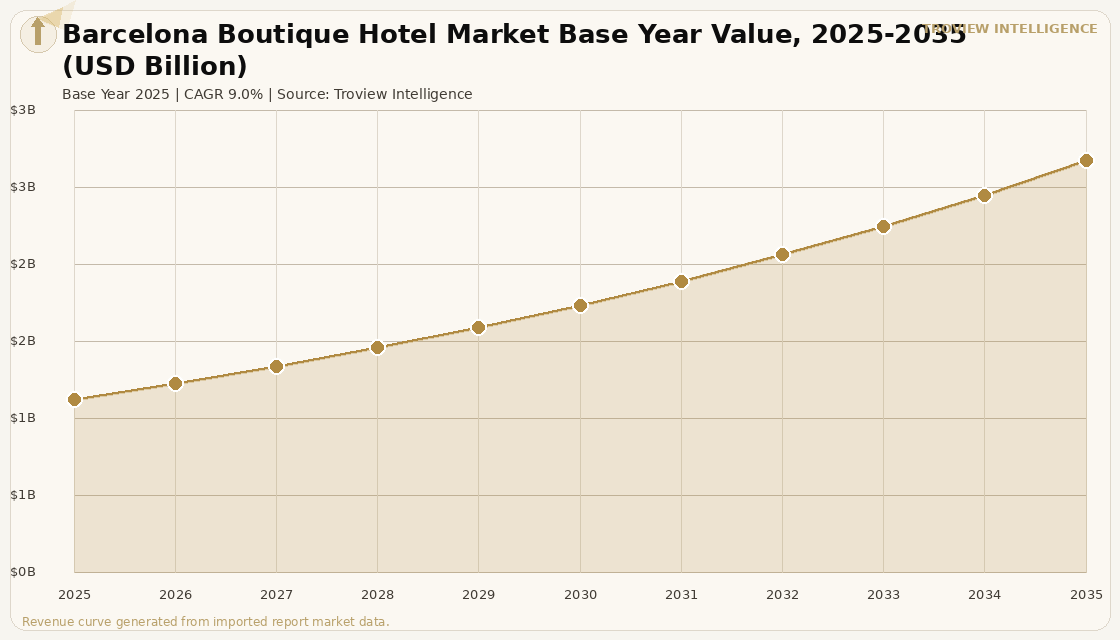

The Barcelona boutique hotel market size was USD 1.24 Billion in 2025 and is expected to register a revenue CAGR of 9.0% during the forecast period, reaching USD 2.94 Billion by 2035. Barcelona is Europe's most supply-constrained major hotel market and Spain's highest-ADR city after Marbella, with hotel supply growing only 0.1% year-on-year in the year to May 2025 adding just 462 rooms as the city government's hotel licence moratorium in central districts maintains structural scarcity that drives ADR growth irrespective of demand cycles. H1 2025 ADR in Barcelona reached EUR 195.5 per Cushman and Wakefield Spain H1 2025 data a 3.1% year-on-year increase with RevPAR reaching EUR 149.80 (up 1.6%), occupancy at 76.6%, and the full-year ADR reported by STR as Spain's second-highest national city rate. Barcelona hotels in the year to May 2025 achieved a GOP margin of 45.1% up from 43.9% with 66.9% GOP flow through, confirming that revenue growth significantly outpaced cost growth at the operating level despite payroll and cost of sales increases per Hospitality Net Barcelona Hotel Market Spotlight. For instance, in 2025, Barcelona's hotel investment market received EUR 518 million of total hotel investment, with institutional investors accounting for 63% of total volume and private investors 35%, with the most competitive transactions in the market concentrated on boutique hotel properties in Eixample, Gothic Quarter, and Born where hotel licences provide irreplaceable access to the city's highest-demand visitor corridors, per GG Real Estate Barcelona verified investment market data. These are some of the key factors driving revenue growth of the market.

Barcelona's boutique hotel market in 2025 is characterised by the paradox of demand strength and supply paralysis. The HVS Barcelona Market Pulse 2025 confirmed that average daily rates continue to rise despite ongoing local pushback against overtourism and the introduction of protective measures with the combination of supply constraint and sustained international demand from 220 direct flight connections across 200 cities in 64 countries creating an ADR growth environment that will continue as long as the moratorium persists. The city's port hosted 2.8 million cruise passengers in 2024, with city officials considering further reducing cruise terminals from seven to five following a prior reduction from nine in 2018, a measure that would modestly reduce mass-market visitor inflows while boutique hotel guests who are typically higher-spending independent travellers on extended stays would be largely unaffected. Barcelona's boutique hotel operating economics are exceptional by European standards: well-run boutique assets in Eixample and Born targeting annual returns of 5 to 8%, with value-add, capital expenditure, and brand repositioning programmes capable of unlocking 10 to 15% depending on occupancy and ADR uplift performance per GG Real Estate Barcelona verified investment market analysis.

However, the Barcelona boutique hotel market faces structural constraints that are real despite the exceptional current operating metrics. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation that affects Barcelona boutique operators whose electricity costs have risen significantly as Spain's energy mix adjusts to natural gas price volatility a cost pressure that reduces the net operating income benefit of ADR growth for boutique operators with fixed lease structures and limited ability to pass utility cost increases through to room rate pricing. Barcelona's overtourism management agenda a proposed doubling of the city tax from EUR 3.25 to approximately EUR 6.50 per guest per night, stricter controls on tourist apartment licences that affect the supply base competing with boutique hotels, and the potential restructuring of cruise infrastructure creates a complex policy environment where individually beneficial and harmful interventions are being implemented simultaneously, requiring boutique hotel investors to model multiple regulatory scenarios over a five to ten year hold period. The HVS Barcelona Market Pulse 2025 noted that as with other European cities, Barcelona faces potential headwinds from US dollar depreciation that may impact inbound travel from the USA a source market that generates above-average spending per night in Barcelona boutique hotels though no material effect had materialised in Q1 2025 per HVS reporting. These factors substantially limit Barcelona boutique hotel market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "Barcelona's boutique hotel market is a textbook example of what happens when a city becomes so desirable that its government restricts the supply of accommodation in the name of resident wellbeing. The hotel licence moratorium since 2015 was designed to protect Barcelona's neighbourhoods from overtourism. What it has also done is make existing hotel licences particularly in Eixample, Gothic Quarter, and Born worth dramatically more than the buildings that contain them. A 30-room boutique hotel in the Eixample with a valid hotel licence and market-rate ADR of EUR 250 to EUR 300 is not primarily valued on its current NOI. It is valued on the optionality embedded in its licence: the ability to operate in a market where its competitors cannot legally enter. That is a fundamentally different investment proposition from a boutique hotel in Madrid or Lisbon where new licensed supply can respond to demand. The investor who understands this is buying a regulatory moat. The investor who ignores this is simply buying a hotel." Troview Intelligence Senior Analyst, Barcelona Hotel Real Estate

SEGMENT INSIGHTS

District Deep-Dives

| Licensed Boutique Properties | Investment Competition | ADR Range | District Advantage |

| 95 hotels in Eixample | Most competitive in Barcelona | EUR 200-350 for boutique tier | Modernista architecture, central, connected |

Eixample is Barcelona's primary boutique hotel district, hosting 95 licensed hotel properties more than any other district concentrated in a 19th-century grid layout of Modernista architecture that provides the design authenticity and neighbourhood character that boutique hotel guests prioritise per GG Real Estate Barcelona investment market analysis. The Eixample's combination of proximity to Passeig de Gracia (Barcelona's premier shopping and architecture corridor), dense restaurant and bar programming, and the architectural heritage of Gaudi's Casa Batllo and Casa Mila creates the neighbourhood immersion experience that defines boutique hospitality at its most commercially compelling. Investment competition for licensed boutique hotel assets in Eixample is the most intense of any Barcelona district, with institutional investors including private equity and hotel REITs competing with Spanish family offices and international boutique hotel operators for properties that combine existing hotel licences with Modernista building fabric and upper-upscale ADR positioning. Well-run Eixample boutique hotels target annual returns of 5 to 8%, with value-add repositioning programmes unlocking 10 to 15% depending on the starting occupancy, ADR, and operator performance per verified investment market benchmarking.

| Licensed Hotels in District | Heritage Asset Profile | ADR Premium | Primary Guest Type |

| 7 hotels most scarce in Barcelona | Roman foundations, medieval streets | EUR 250-500 for boutique tier | Leisure, design, architecture tourists |

The Gothic Quarter is Barcelona's most heritage-authentic boutique hotel district and its most licence-scarce, with only 7 licensed hotels in the district per GG Real Estate Barcelona data, making existing hotel licences in the Barri Gotic the rarest and most premium hospitality real estate assets in the city. The neighbourhood's Roman foundations, medieval street grid, and proximity to Barcelona Cathedral create an authenticity premium that no other Barcelona district can replicate a boutique hotel occupying a converted medieval merchant house within the Roman wall circuit commands ADR premiums of 30 to 60% above comparable accommodation in the Eixample simply through the power of address and architectural heritage. The Gothic Quarter's boutique hotel operators serve the most affluent leisure, design, and architectural tourism segment in Barcelona, with guests willing to accept smaller room dimensions and older building fabric in exchange for the irreplaceable experience of sleeping in a building with 2,000 years of history at its foundations. New boutique hotel supply in the Gothic Quarter is essentially impossible under the current moratorium, making existing licensed assets permanent scarcity instruments in a market where demand continues to grow.

| District Character | Boutique Hotel Aesthetic | Guest Profile | Growth Driver |

| Art galleries, independent F&B, artisans | Design-led, local brand collaborations | Affluent millennial and Gen Z travellers | Social media, design tourism, F&B culture |

El Born is Barcelona's fastest-growing boutique hotel district by ADR appreciation rate, serving the affluent millennial and Gen Z leisure traveller who prioritises neighbourhood authenticity, independent food and beverage programming, and design-forward aesthetics over the branded luxury experience. The Born's concentration of independent art galleries, artisan workshops, independent restaurant and cocktail bar operators, and the landmark Museu Picasso creates the cultural programming density that boutique hotels in the district leverage as a differentiator with properties offering curated neighbourhood dining guides, artist collaborations, and locally-roasted coffee programmes that generate a sense of local embeddedness impossible to replicate in chain-affiliated properties. El Born boutique hotel operators have invested heavily in social media content strategy, with design-forward common areas, rooftop terraces, and locally-commissioned art installations generating earned media reach that provides discovery channel benefits at minimal marketing cost. Licensed boutique hotel properties in El Born are increasingly competitive investment targets as the district's gentrification and tourism appeal have appreciated consistently over the past decade.