| TROVIEW INTELLIGENCE | Boutique Hotel Market | Q2 2026 |

By Geography - By Hotel Type - By Size - By Booking Channel

The global boutique hotel market was valued at USD 26.68 Billion in 2024 with the luxury boutique segment holding a 53.2% revenue share, 67.3% of luxury travellers now prioritise personalised service and authentic cultural immersion over standardised hotel amenities, lifestyle boutique properties are growing at 8.9% CAGR driven by design-forward aesthetics and social-media positioning that appeals to affluent millennials, and Spain's hotel sector closed 2025 with a full-year ADR of EUR 166.1 a 4.8% increase and RevPAR growth of 5.5% that outperformed Europe as a whole where ADR grew only 1.2% and RevPAR grew only 1.5%, confirming that boutique-heavy leisure markets with supply-constrained licensing environments are generating the strongest rate growth in European hospitality.

MARKET SYNOPSIS

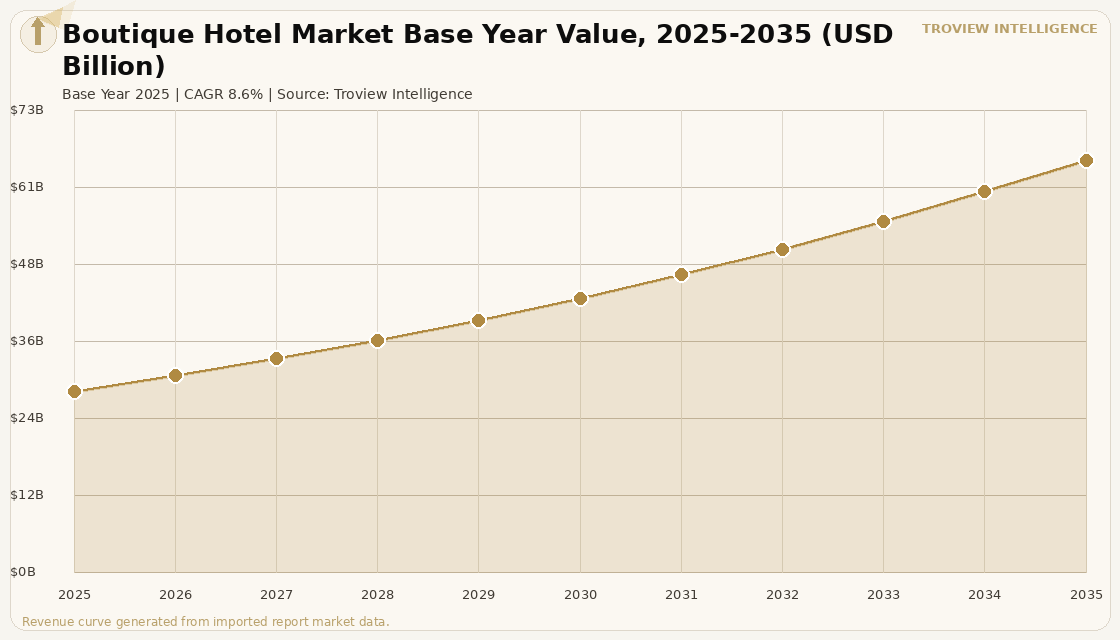

The global boutique hotel market size was USD 28.62 Billion in 2025 and is expected to register a revenue CAGR of 8.6% during the forecast period, reaching USD 64.94 Billion by 2035. The boutique hotel market encompasses independently operated and collection-branded properties typically featuring 10 to 100 rooms that differentiate through distinctive design, personalised service, authentic local cultural connection, and curated guest experiences rather than through the standardised amenity suite and loyalty programme reach of large hotel chains. The luxury boutique segment held a 53.2% revenue share in 2024, with leisure travellers comprising 70.2% of boutique hotel guests per verified market data, and direct bookings accounting for 41.2% of all boutique hotel reservations a structurally higher direct booking share than large branded hotels reflecting the brand authenticity and personalised pre-arrival communication that drives guests to book directly with boutique properties rather than through OTA intermediaries. Lifestyle boutique hotels the segment characterised by design-forward aesthetics, curated local programming, and social-media-driven positioning grew at 8.9% CAGR through 2025, driven by strong demand from younger affluent cohorts in their 30s and 40s who allocate a disproportionate share of discretionary spending to experiential travel per verified consumer research. For instance, in 2025, Marriott International, United States, continued expanding its lifestyle boutique collection brands including Moxy Hotels, Autograph Collection, and Tribute Portfolio across European gateway cities, adding designed-experience properties in Barcelona, Madrid, and Lisbon that compete directly with independent boutique operators for millennial and Gen Z leisure travellers while providing loyalty programme distribution that independent properties cannot match. These are some of the key factors driving revenue growth of the market.

North America led the global boutique hotel market with a 37.2% revenue share in 2024, generating USD 9.3 billion per verified market data, driven by the dense concentration of boutique hospitality investment in New York, San Francisco, Nashville, Austin, and Miami where urban revitalisation programmes and destination resort development created new boutique product. Europe maintained steady 6.1% growth through heritage tourism recovery and sustainability-focused boutique investment, with Spain emerging as the continent's strongest individual boutique hotel market by RevPAR performance as the country closed 2025 with national ADR of EUR 166.1 growing 4.8% year-on-year versus Europe's 1.2% average and RevPAR growing 5.5% versus Europe's 1.5% average per STR and Cushman and Wakefield Hotel Barometer data published March 2026. Asia Pacific is the fastest-growing region for boutique hotels, expanding at 8.9% CAGR through 2033, with India registering the highest projected country-level CAGR as the domestic HNWI population's preference for heritage property restoration boutique hotels palace hotels, haveli conversions, and plantation estate retreats drives demand for intimate experiential accommodation that the country's independent boutique sector is uniquely positioned to supply.

However, the global boutique hotel market faces structural constraints that temper revenue growth across multiple markets. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation and travel uncertainty that particularly affects independent boutique hotel operators who lack the energy procurement scale advantages of large hotel chains through rising utility costs that erode margins on properties where personalised service and labour-intensive operations already represent 35 to 45% of total operating expenditure. The structural market share shift toward soft-brand and collection boutique affiliated with major chains Marriott's Autograph Collection, Hilton's Curio Collection, IHG's Vignette Collection is creating competitive pressure for truly independent boutique operators who cannot access comparable loyalty programme distribution and face OTA commissions of 15 to 25% on the bookings they cannot convert to direct. Supply licensing restrictions in mature boutique markets including Barcelona where the city government has maintained a moratorium on new hotel licences in central districts since 2015 create both an investment opportunity for owners of existing licensed boutique assets and a structural constraint on the market's ability to grow supply to meet demand. These factors substantially limit global boutique hotel market growth over the forecast period.

The boutique hotel market's competitive moat in 2025 is simultaneously widening and narrowing. It is widening because experiential travel is a genuinely structural demand shift the preference of the 30 to 50-year-old affluent traveller for distinctive, design-led, locally-connected accommodation over the standardised hotel experience is not a trend. It is a generational realignment of the value placed on authenticity versus convenience. It is narrowing because every major chain now operates a boutique collection that delivers 70% of the independent boutique experience at 100% of the loyalty programme and distribution infrastructure. The operators who will outperform in this environment are those who offer the remaining 30% the genuinely irreplaceable local embeddedness, the owner-personality-driven service culture, the neighbourhood-specific food and beverage programming at a price point that justifies the sacrifice of Marriott Bonvoy points. Barcelona's Eixample boutique operators understand this. Barcelona's hotel licence moratorium has made their assets worth more every year without them having to do anything. That is the most powerful structural advantage in boutique hospitality." Troview Intelligence Head of Global Boutique Hotel Market Research

SEGMENT INSIGHTS

By Hotel Type

Luxury boutique hotel type is expected to account for a significantly large revenue share in the global boutique hotel market during the forecast period.

Based on hotel type, the global boutique hotel market is segmented into luxury boutique hotels, lifestyle boutique hotels, classic and heritage boutique hotels, and budget and design boutique hotels. Luxury boutique hotels dominated with 53.2% revenue share in 2024 per verified market data, serving the ultra-HNWI and upper-affluent traveller cohort that prioritises service personalisation, low room counts (typically 10 to 50 rooms), and exceptional F&B programming over the standardised amenities of large luxury chains. Lifestyle boutique hotels properties including Ace Hotel Group, 25hours Hotels, and citizenM that balance design aspiration with accessibility at price points 35.2% below pure luxury positioning are expected to register the fastest revenue CAGR during the forecast period, driven by the affluent millennial and Gen Z traveller cohort that allocates the highest share of leisure travel spending to design-forward, socially-connected boutique experiences.

By Hotel Size

Small boutique hotels of up to 50 rooms are expected to account for a significantly large revenue share in the global boutique hotel market during the forecast period.

Based on hotel size, the global boutique hotel market is segmented into small boutique properties of up to 50 rooms, medium boutique properties from 50 to 100 rooms, and larger boutique-characterised properties above 100 rooms that retain boutique experience through individualised design and service. Small properties of up to 50 rooms dominate the independent boutique segment by property count and by owner-operator profile, as the sub-50-room format enables the genuine service personalisation where guests are recognised by name and preferences are anticipated from reservation stage that defines the boutique experience at its most authentic. Medium boutique properties from 50 to 100 rooms are expected to register the fastest CAGR during the forecast period, as the segment benefits from the scale efficiencies of 60 to 100 rooms while maintaining the curated design identity and locally-embedded programming that differentiates boutique from branded product.

By Booking Channel

Direct booking channel is expected to account for a significantly large revenue share in the global boutique hotel market during the forecast period.

Based on booking channel, the global boutique hotel market is segmented into direct bookings, online travel agency bookings, travel agent and tour operator bookings, and global distribution system bookings. Direct bookings account for 41.2% of boutique hotel reservations per verified market data a structurally higher share than the 25 to 30% direct booking rates typical of large branded hotels reflecting the brand identity strength of well-positioned independent boutique hotels that drives guests to book directly to access rate parity and personalised pre-arrival communication. Online travel agency bookings are expected to register the fastest CAGR during the forecast period, driven by the continued expansion of Booking.com, Expedia, and Mr. and Mrs. Smith into boutique-specialist curation that provides independent boutique operators with discovery channels they could not previously access without significant marketing investment.

REGIONAL ANALYSIS

NORTH AMERICA LARGEST

| NA Revenue Share 2024 | NA Revenue (2024) | US Boutique Pipeline | Fastest-Growing US Market |

| 37.2% of global market | USD 9.3 billion | Nashville, Austin, Miami | Lifestyle boutique at 8.9% CAGR |

North America is the global boutique hotel market leader, with the United States accounting for 87.8% of the North American segment and generating the deepest venture capital, private equity, and institutional investment into boutique hotel concepts including Ace Hotel Group, Proper Hotel, and 1 Hotels that have pioneered the lifestyle boutique format now being replicated globally. Urban revitalisation projects in Nashville, Austin, and Miami have created concentrated boutique hotel investment zones where historically neglected warehouse and industrial districts have been converted to design-forward hospitality product targeting affluent millennial leisure travellers a pattern replicated from New York's Meatpacking District and San Francisco's SoMa that has made mid-sized US gateway cities the proving ground for new boutique hotel concepts before their European and Asian Pacific rollouts. Hyatt Hotels Corporation, United States, continued expanding its boutique-adjacent Andaz and Thompson collections in North American gateway cities, competing for the affluent leisure segment that independent boutique operators serve while providing loyalty programme distribution that drives higher direct booking conversion rates.

EUROPE

| Spain RevPAR Growth 2025 | Spain ADR Growth 2025 | Spain ADR vs Europe Avg | Barcelona H1 2025 ADR |

| +5.5% YoY (CW/STR data) | EUR 166.1 (+4.8% vs Europe +1.2%) | 4x Europe average rate growth | EUR 195.5 (+3.1% YoY) |

Europe is the global boutique hotel market's strongest rate-growth region in 2025, with Spain recording full-year ADR growth of 4.8% that was four times the European average of 1.2% per STR and Cushman and Wakefield Hotel Barometer data published March 2026, and full-year RevPAR growth of 5.5% against Europe's 1.5% average. The Spanish boutique hotel market benefits from a structural supply constraint driven by municipal hotel licensing moratoria Barcelona has maintained a moratorium on new hotel licences in central districts since 2015, creating artificial scarcity that forces ADR growth among existing operators and from the sustained leisure tourism demand from Northern European source markets that fills boutique properties at occupancy rates above 75% through ten to eleven months per year. France's heritage property boutique segment chateaux hotels, vineyard estates, and Relais and Chateaux members in Provence and the Loire Valley generates the second-highest per-room rate among European boutique operators, with ultra-luxury independent properties achieving EUR 500 to EUR 1,500 per night in peak summer season.

ASIA PACIFIC

| APAC CAGR (through 2033) | Fastest Country CAGR | India Boutique Driver | Japan Boutique Format |

| 8.9% fastest global region | India (highest boutique CAGR) | Heritage palace and haveli hotels | Ryokan Japan's native boutique |

Asia Pacific is the fastest-growing boutique hotel region, expanding at 8.9% CAGR through 2033, driven by India's heritage property boutique segment palace hotels, haveli conversions, and colonial-era plantation retreats that serves a domestic ultra-HNWI population ranking fourth globally in individuals with assets exceeding USD 100 million alongside international luxury leisure travellers seeking authentic cultural immersion that India's independent boutique operators uniquely provide. Japan's ryokan format the nation's indigenous boutique hospitality tradition of intimate family-operated inns offering curated multi-course kaiseki dining, onsen bathing, and traditional spatial design is experiencing premium pricing recovery following the post-pandemic surge in inbound HNWI travel stimulated by yen depreciation, with premium ryokan in Kyoto, Hakone, and Noto Peninsula commanding USD 500 to USD 2,000 per night. Thailand's boutique resort segment in Chiang Mai, Phuket, and Koh Samui continued to expand in 2025 as Southeast Asian destination tourism recovered to above pre-pandemic demand levels across all source markets per verified industry data.