| TROVIEW INTELLIGENCE | Casino and Integrated Resort Market | Q2 2026 |

By Geography - By Revenue Type - By Resort Format - By End-User

Macau's casinos generated MOP 118.77 billion (USD 14.7 billion) in gross gaming revenue in H1 2025 a 4.4% year-on-year increase with citywide hotel occupancy averaging 90.1%, Las Vegas Strip GGR reached USD 840 million in January 2025 alone a 22.5% year-on-year surge the Las Vegas Strip set a record ADR of USD 193.16 in 2024, Marina Bay Sands delivered a record quarterly EBITDA of USD 768 million in Q2 2025 per Las Vegas Sands SEC filing, and Wynn Al Marjan Island the UAE's first integrated resort with a casino licence from the GCGRA secured October 2024 topped out at 283 metres across 70 floors in December 2025, confirming the Middle East's emergence as the next frontier for integrated resort development.

MARKET SYNOPSIS

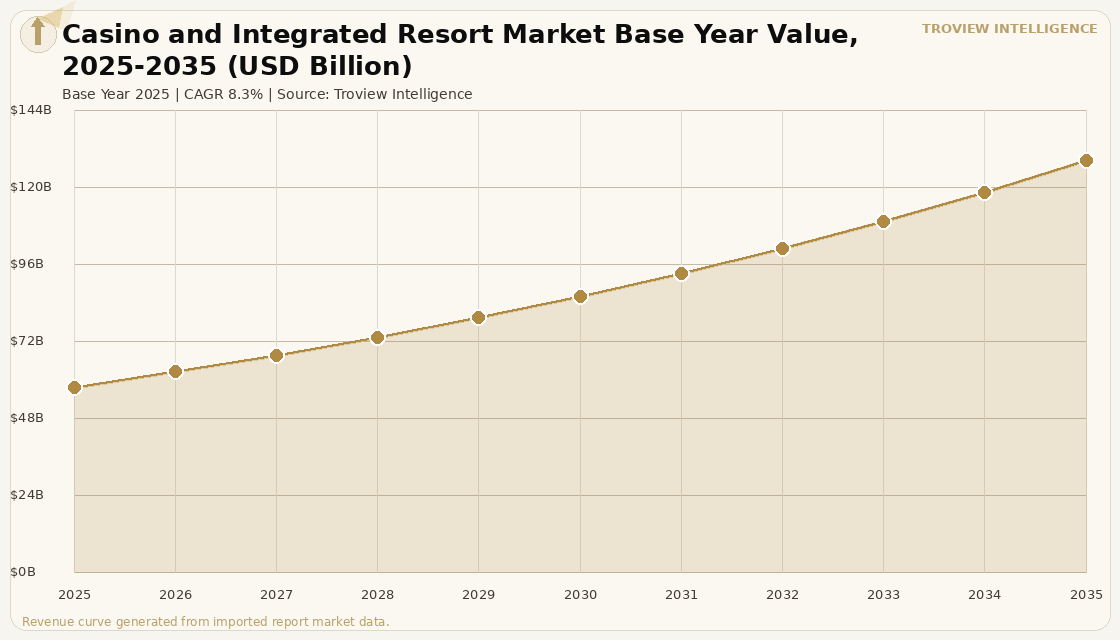

The global casino and integrated resort market size was USD 57.82 Billion in 2025 and is expected to register a revenue CAGR of 8.3% during the forecast period, reaching USD 128.47 Billion by 2035. The casino and integrated resort market encompasses large-scale destination properties that combine casino gaming floors with luxury hotel accommodation, convention and exhibition facilities, branded dining and retail, live entertainment venues, and wellness infrastructure a multi-revenue model where non-gaming revenue at the most sophisticated integrated resorts including Marina Bay Sands and Wynn Las Vegas accounts for 40 to 60% of total property revenue, reducing earnings volatility compared to pure-play casino assets. The 2025 market estimate is grounded in verified company revenues: Las Vegas Sands Corporation reported Q2 2025 net revenue of USD 3.18 billion including Macao adjusted property EBITDA of USD 566 million and Marina Bay Sands record adjusted property EBITDA of USD 768 million per LVS SEC filing of July 2025; MGM Resorts International's partnership with Marriott generated 140,000 incremental bookings within months of its launch, demonstrating the importance of hospitality distribution ecosystems to integrated resort revenue diversification. Macau the world's largest casino market by GGR generated MOP 118.77 billion (USD 14.7 billion) in H1 2025 at a 4.4% year-on-year growth rate, with citywide hotel occupancy averaging 90.1% and Cotai strip properties benefiting from regional family tourism and premium-mass segment growth as the post-pandemic shift away from VIP baccarat toward higher-volume premium-mass play stabilised Macau's GGR composition. For instance, in December 2025, Wynn Resorts and Marjan announced that Wynn Al Marjan Island the UAE's first integrated resort, holding the region's initial land-based casino licence issued by the General Commercial Gaming Regulatory Authority in October 2024 reached its topping-out milestone at 283 metres across 70 floors, with the USD 5.1 billion project featuring 1,542 rooms, 225,000 square feet of gaming space, 22 restaurants, and a Spring 2027 opening target confirmed by Wynn Resorts press release. These are some of the key factors driving revenue growth of the market.

Asia Pacific is the dominant casino and integrated resort market region, accounting for approximately 38% of 2025 revenue per verified industry data, anchored by Macau's six licensed concessionaires Sands China, Galaxy Entertainment Group, Wynn Macau, MGM China, Melco Resorts and Entertainment, and SJM Holdings and Singapore's duopoly of Marina Bay Sands and Resorts World Sentosa, which together contributed up to 2% of Singapore's national GDP in 2024. North America retained 42.10% of casino hotel revenue in 2025, led by the Las Vegas Strip where GGR reached USD 13.5 billion in 2024 and January 2025 Strip GGR surged 22.5% year-on-year to USD 840 million, with the luxury segment capturing 60.67% of casino hotel revenue in 2025 and charting a 7.42% CAGR through 2031. The Formula 1 Las Vegas Grand Prix demonstrated the event-economy multiplier effect that integrated resorts leverage: the race added USD 1.3 billion of local economic value and elevated RevPAR by 25 to 40% during race week, confirming that integrated resorts with convention, entertainment, and sports event infrastructure generate non-gaming revenue streams that pure-play casinos cannot replicate. Japan's MGM Osaka integrated resort commenced construction in April 2025 on Yumeshima island with 2,500 rooms and a 2030 opening target, per verified reporting the first legally sanctioned IR in Japan and a potential second round of bidding for Hokkaido and Tokyo licences signals that Japan will become Asia Pacific's largest new integrated resort market of the current decade.

However, the global casino and integrated resort market faces structural constraints that moderate the pace of revenue growth across multiple markets. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation and regional travel uncertainty that affects Middle Eastern integrated resort development particularly relevant to the Wynn Al Marjan Island project in Ras Al Khaimah, which relies on Gulf energy infrastructure for its operational systems and on Western European and Asian Pacific visitor flows that pass through or near Hormuz-adjacent geopolitical risk zones. VIP baccarat revenue volatility structurally inherent in the rolling chip segment that once dominated Macau's GGR and remains a significant component of Marina Bay Sands' gaming revenue creates earnings-per-quarter variance that equity markets penalise with lower valuation multiples relative to non-gaming hospitality companies, incentivising integrated resort operators to shift capital toward amenity investment that drives non-gaming revenue but also increases development cost and operating leverage. The construction and operating complexity of world-class integrated resorts with Wynn Al Marjan Island's total development cost reaching USD 5.1 billion and MGM Osaka's anticipated development budget in a similar range creates capital deployment concentration risk for operators who are simultaneously managing construction programmes in multiple jurisdictions while maintaining operational discipline at existing properties across Macau, Singapore, and Las Vegas. These factors substantially limit global casino and integrated resort market growth over the forecast period.

The integrated resort industry in 2025 and 2026 is in the most geographically expansive phase of its history. From a single Las Vegas model 30 years ago, the format has replicated across Macau, Singapore, the Philippines, South Korea, and is now landing in Japan and the UAE simultaneously. What is remarkable is that these are not incremental market entries they are transformational national economic events. MGM Osaka will be the first legal casino in Japan's history. Wynn Al Marjan Island will be the first in the UAE's history. Both carry the weight of being proof-of-concept for regulatory frameworks that have never been tested at scale. The operating lesson from Marina Bay Sands which generated USD 768 million of EBITDA in a single quarter, 2% of Singapore's GDP in 2024 as a standalone property, and has generated returns that made the SGD 8 billion investment thesis look conservative is that a well-regulated, well-capitalised integrated resort in a destination market with no domestic competition and strong international airlift can deliver returns that no other single asset in hospitality can match. Japan and the UAE are both trying to replicate that model. The structural question is whether each market can generate the visitor volumes and non-gaming revenue intensity that makes the development economics work at USD 5 billion development cost per resort." Troview Intelligence Head of Global Casino and Integrated Resort Research

SEGMENT INSIGHTS

By Revenue Type

Gaming revenue type is expected to account for a significantly large revenue share in the global casino and integrated resort market during the forecast period.

Based on revenue type, the global casino and integrated resort market is segmented into gaming revenue (casino floor GGR including slots, table games, baccarat, and poker), non-gaming accommodation revenue, food and beverage revenue, retail and entertainment revenue, and MICE and convention revenue. Gaming revenue dominates total market revenue at stabilised integrated resorts Macau operators generated MOP 118.77 billion (USD 14.7 billion) in H1 2025 GGR alone but non-gaming revenue is growing as a proportion of total integrated resort revenue at every major operator. At Marina Bay Sands, non-gaming revenue from The Shoppes retail, convention facilities, dining, and hotel accommodation collectively contributed to a quarterly property EBITDA of USD 768 million in Q2 2025 per LVS SEC disclosure. Non-gaming revenue is expected to register the fastest CAGR during the forecast period, driven by operator investment in live entertainment theatres, branded F&B programming with celebrity chef partnerships, luxury retail concession income, and MICE facilities that generate recurring corporate and government conference demand independent of gaming activity cycles.

By Resort Format

Fully integrated convention and leisure resort format is expected to account for a significantly large revenue share in the global casino and integrated resort market during the forecast period.

Based on resort format, the global casino and integrated resort market is segmented into fully integrated convention and leisure resorts, casino-anchored hotel complexes, tribal and regional destination casinos, and online gaming integrated with physical resort loyalty programmes. Fully integrated convention and leisure resorts properties of the Las Vegas Sands, MGM Resorts, and Wynn Resorts model combining gaming floors exceeding 100,000 square feet with 2,000 to 5,000 hotel rooms, exhibition halls, live entertainment venues, and branded retail dominate total revenue by asset value and by EBITDA generation capacity. Tribal and regional destination casinos in North America are expected to register the fastest CAGR during the forecast period within the segment, driven by states including New York, Texas, and Illinois advancing commercial casino legislation that will expand the addressable market for integrated resort development beyond the established Nevada and Atlantic City corridors.

By End-User

Leisure and destination gaming traveller end-user segment is expected to account for a significantly large revenue share in the global casino and integrated resort market during the forecast period.

Based on end-user, the global casino and integrated resort market is segmented into leisure and destination gaming travellers, premium-mass and VIP gaming patrons, MICE and convention delegates, and non-gaming resort guests. Leisure and destination gaming travellers dominate total end-user revenue in North American and emerging Middle Eastern integrated resorts, where the non-gaming guest who attends entertainment shows, dines at celebrity chef restaurants, and participates in pool and spa programming without visiting the casino floor constitutes 40 to 50% of total resort occupancy. Premium-mass gaming patrons the segment between VIP rolling chip players and mass-market slot and table players, characterised by direct credit arrangements and personalised service without the commission-driven junket intermediary model are the fastest-growing end-user segment globally, as Macau's six concessionaires and Singapore's two integrated resort operators have deliberately shifted their GGR composition toward premium-mass after the 2014 to 2016 anti-corruption campaigns in China reduced VIP junket volume.

REGIONAL ANALYSIS

ASIA PACIFIC DOMINANT

| Macau H1 2025 GGR | Macau Hotel Occupancy 2025 | LVS Q2 2025 MBS EBITDA | MGM Osaka Opening |

| MOP 118.77bn (USD 14.7bn) +4.4% | 90.1% citywide average | USD 768 million (record Q) | 2030, Yumeshima island, 2,500 rooms |

Asia Pacific is the global casino and integrated resort market's largest revenue region, accounting for approximately 38% of 2025 market revenue per verified industry data, anchored by Macau's six licensed concessionaires who generated MOP 118.77 billion (USD 14.7 billion) in H1 2025 gross gaming revenue a 4.4% year-on-year increase with citywide hotel occupancy averaging 90.1% per Lexology Macau gaming industry reporting. By mid-July 2025, cumulative Macau GGR had reached MOP 132.35 billion (USD 16.4 billion), representing 61% of the government's revised annual target and a 36.7% increase over the same period in 2024, confirming the recovery trajectory of a market whose pre-pandemic GGR peaked at approximately USD 37 billion annually. Macau's post-pandemic structural shift from VIP rolling chip gaming toward premium-mass play has improved GGR quality premium-mass is less volatile, does not require commission payments to junket operators, and is more predictable for quarterly earnings guidance purposes while simultaneously reducing total GGR potential compared to the junket-driven VIP peak years. Singapore's Marina Bay Sands, operated by Las Vegas Sands Corporation, delivered USD 768 million of adjusted property EBITDA in Q2 2025 a record quarter confirmed by LVS SEC filing with the property contributing up to 2% of Singapore's national GDP in 2024, demonstrating the macro-economic impact that a single world-class integrated resort can generate in a small open economy with strong international airlift infrastructure.

Japan's integrated resort development pipeline is the region's most significant multi-decade market entry. MGM Osaka commenced construction on Yumeshima island in April 2025, with 2,500 rooms and a 2030 opening target per verified Wikipedia and casino industry reporting, representing the first legally sanctioned casino in Japan's history following decades of legislative debate and a regulatory framework modelled on Singapore's licensed duopoly approach. Japan's integrated resort market potential is considered among the largest globally with Tokyo, Osaka, and Yokohama all having been considered as IR sites and the Japanese government's reported consideration of a fresh round of bidding for Hokkaido and Tokyo licences signals that MGM Osaka may be joined by a second and potentially third integrated resort before 2035, creating a Japan market that could rival Macau in total GGR within a decade of the first opening. Investor sentiment toward Macau was confirmed positive by equity market reactions: following Macau's June 2025 GGR release, shares in Wynn Resorts, Las Vegas Sands, and MGM Resorts rose 6 to 9% on US exchanges per Lexology reporting, reflecting capital market confidence in Macau's evolving gaming-entertainment hybrid model.

NORTH AMERICA

| NA Revenue Share 2025 | Las Vegas GGR 2024 | Strip Jan 2025 GGR Growth | Las Vegas Strip ADR Record (2024) |

| 42.10% of casino hotel revenue | USD 13.5 billion | 22.5% YoY to USD 840 million | USD 193.16 (all-time record) |

North America retained 42.10% of casino hotel revenue in 2025 per verified market data, led by the Las Vegas Strip where 2024 GGR reached USD 13.5 billion and the Strip set a record average daily room rate of USD 193.16 in 2024 the highest in the property's operational history confirming that Las Vegas's multi-decade investment in convention infrastructure, live entertainment programming, and celebrity-branded dining has successfully shifted the visitor value proposition beyond gaming. Nevada's January 2025 GGR jumped 12.5% year-on-year to USD 1.44 billion, with the Strip contributing USD 840 million representing a 22.5% year-on-year increase performance partially explained by the Q1 2024 Super Bowl comparison base being a high benchmark, but also confirming the structural momentum in Las Vegas as a global MICE and entertainment destination. The Formula 1 Las Vegas Grand Prix provided the clearest data point for the integrated resort event-economy thesis: the race added USD 1.3 billion of local economic value and elevated RevPAR by 25 to 40% during race week, confirming that integrated resorts with event infrastructure the T-Mobile Arena, Allegiant Stadium, and MSG Sphere adjacency generate non-gaming revenue multiples that justify the capital investment in entertainment assets as operational complements to the casino floor. MGM Resorts International's partnership with Marriott generated 140,000 incremental hotel bookings within months of launch, per verified market data, demonstrating the importance of external loyalty programme distribution for integrated resort occupancy optimisation.

MIDDLE EAST

| Wynn Al Marjan Development Cost | Gaming Space | Hotel Rooms | GCGRA Licence Issued |

| USD 5.1 billion total project | 225,000 sq ft (larger than Wynn LV) | 1,542 rooms + 22 private villas | October 4, 2024 first UAE licence |

The Middle East is the global casino and integrated resort industry's most significant new market entry since Singapore awarded its two IR licences in 2006, with the UAE's General Commercial Gaming Regulatory Authority issuing the region's first land-based casino licence to Wynn Resorts on October 4, 2024 a decision that opened a market in which gambling had been prohibited since the country's founding. Wynn Al Marjan Island is a USD 5.1 billion project on a 60-hectare site on Al Marjan Island in Ras Al Khaimah, featuring 1,542 rooms and suites, 22 private villas, 225,000 square feet of gaming space which Wynn confirmed is larger than its Las Vegas flagship casino floor 22 restaurants and bars, 15,000 square metres of retail, 7,500 square metres of convention space, a theatre, private beach clubs, and a deep-water marina, with a USD 2.4 billion construction loan secured per Hotelier Middle East verified reporting. The project topped out at 283 metres across 70 floors on December 15, 2025 per Wynn press release reaching its highest structural concrete point just 27 months after foundation works began with upon spire installation in 2026 the building will reach 352 metres, becoming the tallest structure in Ras Al Khaimah by over 100 metres. Ras Al Khaimah's tourism authority targets increasing annual visitor numbers from 1.3 million to 3.5 million by 2030, with Wynn Al Marjan Island as the anchor demand driver alongside Janu Al Marjan Island an Aman Group sister brand development announced November 2025 and now under construction creating a multi-property destination resort corridor on Al Marjan Island.