By Submarket · By Asset Type · By Occupier Sector · By Lease Structure

Dallas-Fort Worth posted 27.2 million square feet of positive net absorption in 2025, its seventh consecutive year exceeding 20 million square feet and a feat unmatched by any other US market, as leasing volume of 56.1 million square feet ran more than 50% above long-term norms and Amazon, Google, Medline Industries, and Hayes Company confirmed the region's role as the country's primary inland distribution hub.

MARKET SYNOPSIS

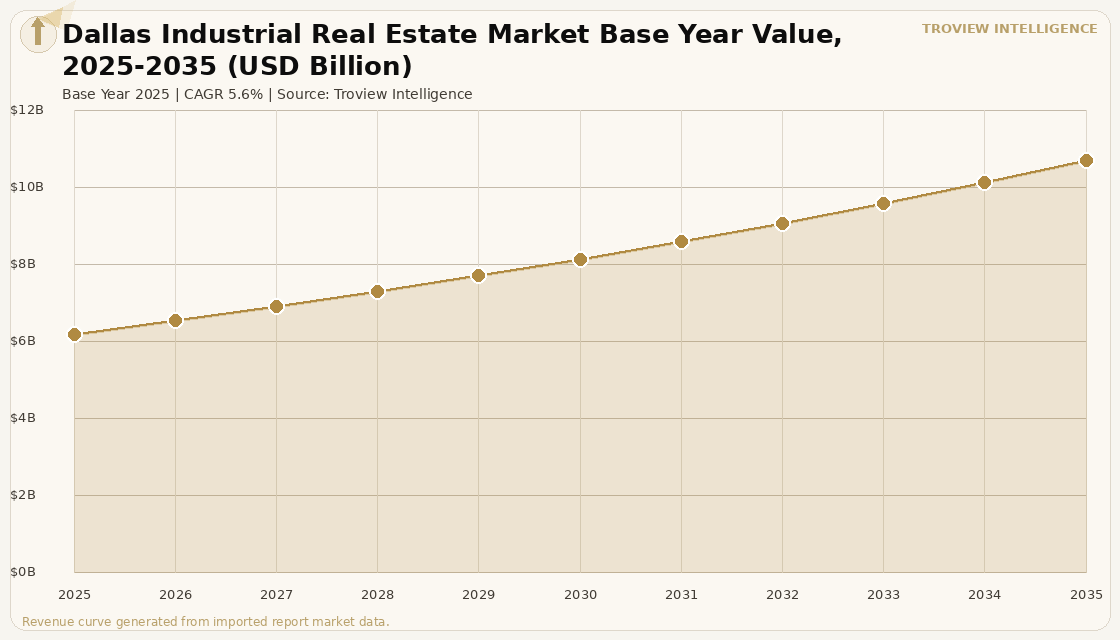

The Dallas industrial real estate market size was USD 6.24 Billion in 2025 and is expected to register a revenue CAGR of 5.6% during the forecast period, reaching USD 10.77 Billion by 2035. Dallas-Fort Worth ended 2025 as the strongest industrial real estate market in the United States, posting nearly 27.2 million square feet of positive net absorption for the year per Avison Young Q4 2025 DFW Industrial Market Report, marking the seventh consecutive year the market exceeded 20 million square feet of annual absorption a streak unmatched by any other US market. Leasing volume reached 56.1 million square feet, more than 50% above long-term norms. Overall vacancy ended Q4 2025 at 9.2%, a decline of 70 basis points from one year prior per Partners Real Estate Q4 2025 market report, with the market classified in neutral conditions as neither landlords nor tenants held a dominant negotiating position. Industrial assets traded near USD 140 per square foot at cap rates averaging 6.2% per CoStar Capital Market Analytics data.

Dallas-Fort Worth's industrial market is underpinned by structural advantages that distinguish it from every other large US market. The DFW Airport vicinity provides direct airfreight access to domestic and international markets from the largest contiguous industrial land reserve of any major US airport corridor. Alliance Airport in North Tarrant County, purpose-built as an industrial airport by Hillwood Development, has become the dominant inland distribution campus in the southern United States, hosting national distribution operations for major retailers and logistics providers. Low operating costs, a large and growing workforce, and no state income tax have sustained a consistent pipeline of corporate relocations and expansions that generate durable multi-decade leasing demand. For instance, in full-year 2025, major occupiers including Medline Industries, Amazon, Google, and Hayes Company committed to DFW industrial space per Avison Young market data, confirming the region's strategic centrality to US consumer goods, technology hardware, and healthcare supply chains. Rent growth maintained a 4.3% annual pace, its twelfth consecutive quarter of deceleration from the 2022 peak but still outperforming most major US markets per Partners Real Estate market analysis. These are some of the key factors driving revenue growth of the market.

However, the Dallas industrial market faces structural constraints. Sublease availability reached a record 15 million square feet in Q3 2025, up 17.3% year-over-year per Newmark market data, including the addition of the 1.1 million square foot former J.C. Penney distribution centre, providing discounted competition that constrains effective rent recovery across the mid-quality warehouse segment. The construction pipeline, while declining from its peak, still stood at 28.3 million square feet under construction at year-end 2025, requiring sustained absorption to prevent vacancy from re-widening as new supply is delivered. Southeast Dallas continues to experience slow lease-up in older product, and data centre developers competing for South Dallas land are reducing the available industrial land supply in that submarket while simultaneously elevating land costs for remaining industrial users. Negative absorption in the manufacturing segment, which recorded 121,430 square feet of negative net absorption in Q4 2025, reflects lingering trade policy uncertainty that has delayed factory-related leasing decisions. These factors substantially limit Dallas industrial real estate market growth over the forecast period.

DFW's seventh consecutive year above 20 million square feet of net absorption is the most compelling single data point in US industrial real estate. No other market has done it once, let alone seven times running. The Alliance submarket is effectively a privately planned industrial city Hillwood built the airport, the roads, and the buildings, and the tenants followed. South Dallas is the more complicated story. Data centre demand for land is a genuine constraint on industrial supply there, and the former J.C. Penney sublease is a weight on mid-quality rents. But the overall direction is clear. Deliveries are falling, absorption is rising, and DFW is the one US industrial market where the structural demand case does not depend on a cyclical tailwind." Troview Intelligence Head of Dallas Industrial Real Estate Research

SEGMENT INSIGHTS

By Asset Type

Warehouse and distribution properties are expected to account for a significantly large revenue share in the Dallas industrial real estate market during the forecast period.

Based on asset type, the Dallas industrial real estate market is segmented into warehouse and distribution, flex industrial, and manufacturing facilities. Warehouse and distribution dominates DFW's industrial market by floor area and leasing volume, with the segment recording 7.6 million square feet of positive net absorption in Q4 2025 alone per Partners Real Estate quarterly data, driven by national retailers, third-party logistics operators, and e-commerce fulfilment platforms selecting DFW for its central US location and transportation infrastructure depth. Flex industrial is the most resilient segment against the vacancy correction, maintaining a 6.6% vacancy rate in Q4 2025, significantly below the overall market's 9.2%, as the smaller footprint and diverse tenant mix of flex buildings provide insulation against the demand swings that have concentrated in large-format bulk distribution. Manufacturing recorded negative absorption of 121,430 square feet in Q4 2025, reflecting caution among industrial producers navigating US trade policy uncertainty, but is expected to recover as nearshoring commitments translate from announced to leased.

By Submarket

The Alliance and North Tarrant County submarket is expected to account for a significantly large revenue share in the Dallas industrial real estate market during the forecast period.

Based on submarket, the Dallas industrial real estate market is segmented into Alliance and North Tarrant County, DFW Airport and surrounding corridor, South Dallas and Southeast Dallas, I-20 and Southwest Dallas, McKinney and Northeast Corridor, and secondary submarkets including Denton, Lewisville-Highway 121, and East Forney. Alliance and North Tarrant County leads market absorption and commands the strongest investor demand, anchored by Hillwood Development's master-planned industrial campus built around Alliance Airport. The DFW Airport vicinity maintains the premium industrial rents in the market due to airfreight access and corporate proximity, with infill spaces under 50,000 square feet commanding USD 10 to 12 NNN and new suburban product reaching USD 12 to 15 NNN per M&D CRE market data. South Dallas faces a distinctive constraint: data centre developers are competing for available industrial land, compressing the supply of new industrial sites and creating upward land cost pressure that reshapes the area's viability for standard logistics use.

By Occupier Sector

Consumer goods, logistics, and e-commerce occupiers are expected to account for a significantly large revenue share in the Dallas industrial real estate market during the forecast period.

Based on occupier sector, the Dallas industrial real estate market is segmented into consumer goods and retail distribution, third-party logistics and freight, e-commerce fulfilment, manufacturing, healthcare and medical supply, and technology hardware logistics. Consumer goods companies anchored two of the three largest Q3 2025 leasing transactions in DFW, a departure from prior quarters when logistics and distribution companies dominated large block activity per Newmark Q3 2025 market data. Three of the top five Q3 2025 leases were renewals rather than new entrants, confirming that existing occupiers are prioritising operational continuity over relocation, which sustains base occupancy but moderates the pace of new demand absorption. Healthcare and medical supply, represented by Medline Industries among 2025's major movers, is an expanding occupier category in DFW that benefits from the market's central location and temperature-controlled facility availability.

Submarket Deep-Dives

ALLIANCE / NORTH TARRANT COUNTY STRONGEST ABSORPTION, PREMIER INLAND CAMPUS

| Character | Purpose-built industrial airport campus by Hillwood Development | Vacancy Trend | Strongest performance in DFW; absorption leading market |

| Key Tenants | Major national retailers, logistics operators, manufacturing | Infrastructure | Alliance Airport, BNSF intermodal, I-35W, US-81 |

Alliance is the dominant submarket in Dallas-Fort Worth's industrial market and one of the most successful master-planned industrial developments in the United States. Hillwood Development's decision to build Alliance Airport as a privately operated industrial airfield and surround it with purpose-designed warehouse and distribution campuses created the only major US industrial market where the airport, roads, and buildings were developed in coordination rather than retrofitted around existing infrastructure. The submarket recorded the strongest absorption figures in the DFW market for 2025, with its combination of modern Class A product, multimodal transportation access, and available developable land sustaining consistent demand from national retailers, third-party logistics operators, and light manufacturers. Far north Fort Worth, within the Alliance catchment, held the largest active industrial construction pipeline in DFW at year-end per M&D CRE market analysis, reflecting developer confidence in continued demand from this submarket's proven tenant depth.

| Premium Rent Driver | Direct airfreight access, corporate proximity | Infill Rents | USD 10-12 NNN per sq ft (under 50,000 sq ft) |

| New Suburban Product | USD 12-15 NNN per sq ft | Market-Wide Average | USD 10.22 per sq ft (M&D CRE market data) |

The DFW Airport industrial corridor commands the highest asking rents in the Dallas market, driven by direct airfreight connectivity through DFW International Airport and proximity to the corporate headquarters and regional offices concentrated in Las Colinas, Grapevine, and Irving. Technology hardware logistics, pharmaceutical distribution, and high-value consumer electronics companies anchor the corridor's tenant mix, with the premium for airfreight access sustaining rent levels substantially above the market average. The corridor's infill land supply is constrained by the build-out of the Las Colinas and Southlake commercial districts, limiting new large-format industrial supply and sustaining the occupancy advantage of existing Class A buildings. The Intermodal Logistics Center, where NorthPoint Development completed a 1.25 million square foot speculative project pre-leased before delivery, confirms institutional developer confidence in this submarket's demand fundamentals.

| Challenge | Elevated vacancy; slow lease-up in bulk distribution | New Complication | Data centre developers competing for industrial land |

| Sublease Impact | J.C. Penney 1.1M sq ft former distribution centre | Market Dynamic | Discounted sublease space constraining effective rent |

South Dallas has been the most challenged submarket in the DFW industrial market through 2024 and 2025. The district absorbed a disproportionate share of the speculative construction surge, delivering large-format bulk distribution buildings into a period of subdued demand that left significant first-generation vacancy. Recovery has been slower than in Alliance and the airport corridor because the tenant profile bulk distribution users requiring 500,000 square feet or more is the segment most cautious about expansion commitments in an uncertain trade environment. An emerging complication is that data centre developers, drawn to South Dallas by available land and power infrastructure, are now competing with industrial users for the same development sites, reducing the available land supply for new industrial construction while elevating land costs for the sites that remain. The 1.1 million square foot former J.C. Penney distribution centre that entered the sublease market in Q3 2025 has set a discounted floor for large-block rents in the submarket.

I-20 / SOUTHEAST CORRIDOR VALUE INDUSTRIAL AND SECONDARY LOGISTICS

| Character | Value pricing, secondary logistics, growing e-commerce activity | Submarkets | Southeast Dallas, South Fort Worth, East Forney |

| East Forney | Anticipated growth due to favourable labour market | Cap Rate | Wider than Alliance; value-add investment interest |

The I-20 and Southeast Dallas corridor serves the value-oriented industrial tenant that requires large-format space at below-Alliance pricing, accepting the tradeoff of somewhat less direct access to the major Interstate-35 and I-45 logistics axes. The corridor includes Southeast Dallas, South Fort Worth, and the emerging East Forney industrial cluster east of the Trinity River, where a favourable labour market and lower land costs are attracting e-commerce fulfilment operators and consumer goods distributors unwilling to pay Alliance premiums. East Forney has been identified by market participants as one of the DFW submarkets most likely to see increased activity in 2025 and 2026, as proximity to the growing East Dallas and Forney residential communities provides a workforce base for large-scale fulfilment operations. Value-add investors have shown interest in the corridor's older functional industrial stock, where repositioning into modern specifications can generate meaningful rent premium gains against a low basis.