By Property Type - By Business Model - By City - By Ownership

City Spotlights: Mumbai - Bengaluru - Hyderabad

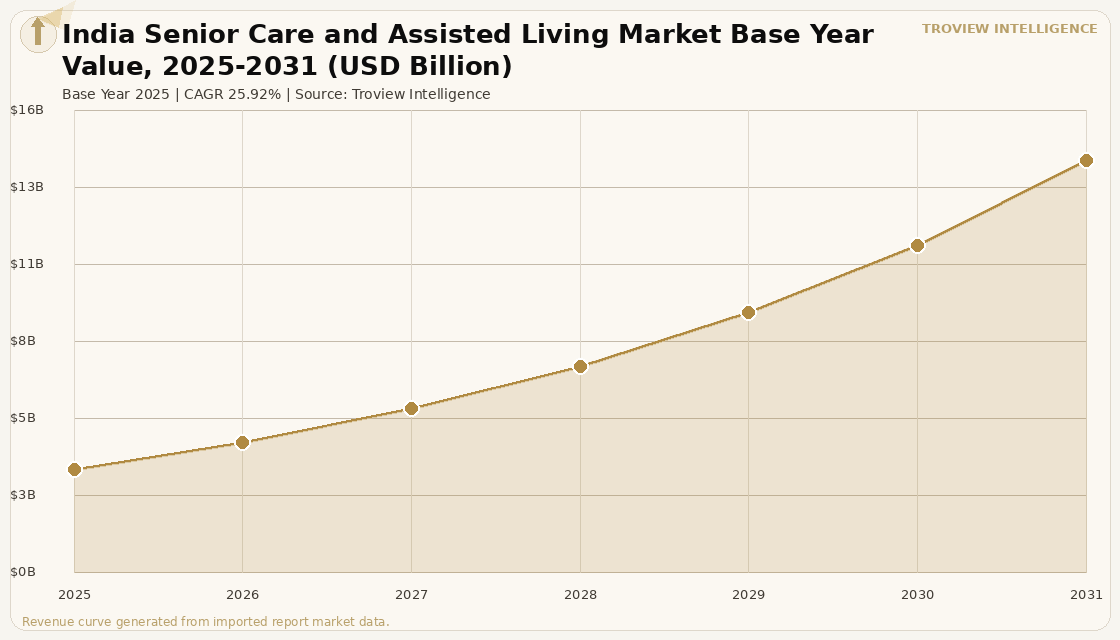

India's senior care market was valued at USD 3.55 Billion in 2025 and is growing at a CAGR of 25.92% through 2031 , India's 156.7 million over-60 population in 2024 is the world's second-largest elderly cohort growing to 346 million by 2050, the sector's 1.3% market penetration compared to 6% in the United States and Australia signals vast addressable demand, nearly 15,000 new senior living homes are expected by 2030 at an estimated investment of INR 26,000 crore per ASLI and JLL India joint report, and Antara Senior Care opened its sixth Indian facility and first in Chennai in May 2026 while Primus Senior Living raised USD 20 million from General Catalyst in October 2024.

MARKET SYNOPSIS

The India senior care and assisted living market size was USD 3.55 Billion in 2025 and is estimated to grow from USD 4.47 Billion in 2026 to reach USD 14.14 Billion by 2031, at a CAGR of 25.92% during the forecast period . India is one of the world's fastest-growing senior care markets, driven by a demographic curve that is steepening with near-mathematical certainty: India's over-60 population stood at 156.7 million in 2024 the world's second-largest elderly cohort and is projected to more than double to 346 million by 2050, representing nearly 21% of India's total projected population at that point per JLL India senior living analysis published November 2024. Against this demographic demand, India's senior living market penetration stands at only 1.3% the share of the elderly population residing in formal senior living, assisted living, nursing care communities, and continuing care retirement communities compared to mature markets including the United States and Australia where penetration rates exceed 6%, confirming a structural demand gap of extraordinary scale. The estimated target market for senior living facilities is projected to grow from 1.57 million households in 2024 to 2.27 million by 2030 per JLL data, with nearly 15,000 new senior living homes expected to come up by 2030 at an estimated investment of INR 26,000 crore per ASLI and JLL India joint report published August 2025. For instance, in May 2026, Antara Senior Care, a subsidiary of Max India Limited, opened a new 43-bed assisted living facility on Chennai's East Coast Road Antara's sixth facility in India and first in Chennai offering 24/7 medical and nursing support, physiotherapy, nutrition management, and mental wellness programmes, confirming the company's geographic expansion from its original NCR and Dehradun base into South India's rapidly growing organised senior care market per verified elderly care market data. These are some of the key factors driving revenue growth of the market.

India's senior living market is structured around two primary property types independent living and assisted living offered through three primary business models: outright sale freehold at average ticket sizes of INR 1 to 2 crore, long-lease and rental formats, and hybrid sale-plus-lease models. Independent living accounted for 64.50% of India's senior living market share in 2025 , with outright sale freehold holding 62.70% of market size. The southern states supply 62% of India's organised senior living capacity despite representing only 7 of India's top-20 metros, a geographic concentration driven by lower fertility rates, higher NRI parent population, and more permissive cultural attitudes toward professional senior care in South India . Bengaluru held a 19.20% stake in the India senior living market in 2025, reflecting its combination of temperate climate, advanced hospital infrastructure, and cosmopolitan culture. The market is witnessing a significant shift as competition moves from small local operators to integrated real estate and healthcare alliances that bundle preventive care, telemedicine, and social engagement services with Columbia Pacific Communities, Antara Senior Care, and Ashiana Housing leading this transition with continuum-of-care campus models where independent, assisted, and memory care wings co-exist on a single property.

However, the India senior care and assisted living market faces structural constraints that moderate the pace of organised sector growth despite the exceptional demand fundamentals. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation that increases operating costs for senior care facilities whose electricity consumption for climate control, medical equipment, and elevator systems represents a significant share of the operating cost base that cannot be reduced without compromising resident safety and comfort standards. The cultural bias in India toward family-based elder care where joint family living has historically been the default care arrangement for elderly parents creates a sales cycle challenge for organised senior care operators: residents and their families must overcome deeply embedded cultural stigma against institutional elder care before committing to a professional senior living arrangement, requiring marketing investment and cultural education that extends the customer acquisition timeline significantly compared to Western markets where professional senior care is an established social norm. High land values in Mumbai and Delhi NCR where plot valuations make large-scale campus development economically challenging compared to southern cities restrict the supply of new senior living units in India's highest-demand metro markets, forcing developers toward satellite city locations in Navi Mumbai and Gurugram where land is more affordable but proximity to family and medical infrastructure is reduced. These factors substantially limit India senior care and assisted living market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "India's senior care market at 1.3% penetration against 156.7 million elderly persons is one of the most compelling healthcare real estate investment arguments I have seen in 20 years of market analysis. The United States and Australia have both demonstrated that penetration rates can reach 6% and beyond as cultural attitudes evolve and professional senior care quality improves. India is not at 1.3% penetration because demand is not there. It is at 1.3% penetration because supply has not been built, regulation has not matured, and cultural attitudes have not yet shifted enough for organised senior care to be the default choice for middle-class Indian families navigating aging parents. All three of those constraints are changing simultaneously. The NRI parent demographic is the clearest signal: parents of Non-Resident Indians are in Mumbai, Delhi, and Bengaluru without their children nearby, with disposable income, with health insurance, and with a clear preference for professionally managed senior care that their children in London, New York, and Singapore can monitor remotely. That is the early adopter market. Southern India captured it first. Mumbai and NCR will be next." Troview Intelligence Head of India Senior Care and Assisted Living Research

SEGMENT INSIGHTS

Three Cities Shaping India's Senior Care Market

| Elderly Population (MMR) | Land Cost Challenge | Key Development Zone | Key Operators Entering |

| ~3.5 million 60+ in MMR | Highest plot valuations in India | Navi Mumbai (Kharghar, Panvel) | Primus (Wadhwa Wise City), Columbia Pacific |

The Mumbai Metropolitan Region is India's largest addressable senior care market by affluent elderly population, hosting approximately 3.5 million persons aged 60 and above across Mumbai city, Navi Mumbai, Thane, and the extended metropolitan region, with a high concentration of NRI parents, retired professionals, and upper-middle-class seniors with the disposable income and cultural willingness to consider organised senior living arrangements. However, Mumbai's land market the most expensive in India creates a structural constraint for large-campus senior living development, where plot valuations in established Mumbai localities far exceed the per-square-foot economics required for viable senior living development at INR 4,000 to 6,000 per square foot residential pricing. Developers have responded by focusing senior living development in Navi Mumbai specifically Kharghar, Panvel, and Palaspa where land costs are materially lower, regulatory clearances through MahaRERA's senior living guidelines are accessible, and proximity to the Mumbai-Pune Expressway provides connectivity to both Mumbai's medical infrastructure and Pune's more affordable cost of living. Primus Senior Living's flagship project Primus Swarna at Wadhwa Wise City marketed as Mumbai's first senior living community within an integrated township of more than 200 acres in Panvel with 24/7 medical assistance exemplifies this suburban corridor development strategy, while Columbia Pacific Communities and multiple other operators are evaluating or committing to the Mumbai Metropolitan Region as their next major expansion geography. Manusmruti senior citizens' home in Kharghar, Navi Mumbai is an established assisted care facility in the market.

| National Market Share (2025) | Climate Advantage | NRI Parent Profile | Key Operators |

| 19.20% of India senior living market | Temperate year-round preferred for seniors | IT sector NRI parents Singapore, US, UK | Columbia Pacific, Athulya, Primus, Antara |

Bengaluru held a 19.20% stake in the India senior living market in 2025 , the largest share of any single Indian city, driven by a combination of temperate year-round climate that makes outdoor activities accessible across all seasons, advanced tertiary hospital infrastructure including Narayana Health and Manipal Hospitals, and a large population of NRI parents whose technology sector children working in Singapore, the United States, and the United Kingdom are willing to pay premium senior living fees for professionally managed care arrangements with digital monitoring capability. Bengaluru is the established base for multiple national senior care operators including Columbia Pacific Communities which operates multiple Bengaluru communities under The Virtuoso and Serene brands Athulya Senior Care, Primus Senior Living, and Antara Senior Care. The organised senior living market in Bengaluru is the most mature in western India, with established properties in Whitefield, Devanahalli, Yelahanka, and electronic city corridors that serve the NRI parent demographic with continuum-of-care campuses offering independent living graduation to assisted care without relocation.

| Projected CAGR (2026-2031) | Growth Driver | Land Cost vs Bengaluru | Key New Projects |

| 26.99% fastest of any Indian city | Pharma and biotech sector wealth | Lower land costs faster development | Expanding developer pipeline in corridors |

Hyderabad is expected to register the fastest CAGR of any Indian city in the senior care and assisted living market at 26.99% between 2026 and 2031 , driven by its pharmaceutical and biotechnology sector wealth corridors in Genome Valley and the Outer Ring Road zone that are generating a growing population of retiring professional and managerial-class seniors with the disposable income and health insurance coverage to access organised senior care. Hyderabad's competitive advantage for senior living development relative to Bengaluru is lower land costs combined with comparable medical infrastructure quality, accelerating regulatory clearance timelines, and strong connectivity to Hyderabad's expanding international airport that facilitates NRI family visits for parents residing in senior communities. The city's pharmaceutical sector employment base creates a unique senior care demand profile: retired senior scientists, research heads, and corporate executives from major pharmaceutical companies including Dr. Reddy's, Aurobindo Pharma, and Divi's Laboratories represent a high-income, health-literate senior cohort that prioritises clinical quality, wellness programming, and preventive health management in their senior living choice.