By Sub-Market - By Brand Tier - By Asset Class - By Source Market

Sub-Markets: Palm Jumeirah - Downtown Dubai - DIFC - JBR Beach - Dubai Marina

Dubai's luxury hotel segment generated an average ADR of approximately AED 1,470 (USD 400) and RevPAR of approximately AED 1,100 (USD 300) in H1 2025, with H1 2025 citywide occupancy above 81%, Dubai welcomed 19.6 million international tourists in full-year 2025, the luxury segment holds ADR premiums of 15 to 25% over unbranded equivalents, Atlantis The Royal opened at a USD 1.4 billion investment setting the global benchmark for ultra-luxury hotel development cost in an emerging luxury gateway, and 12,000 new luxury keys are due by 2030 creating both opportunity and yield compression risk for existing asset owners.

MARKET SYNOPSIS

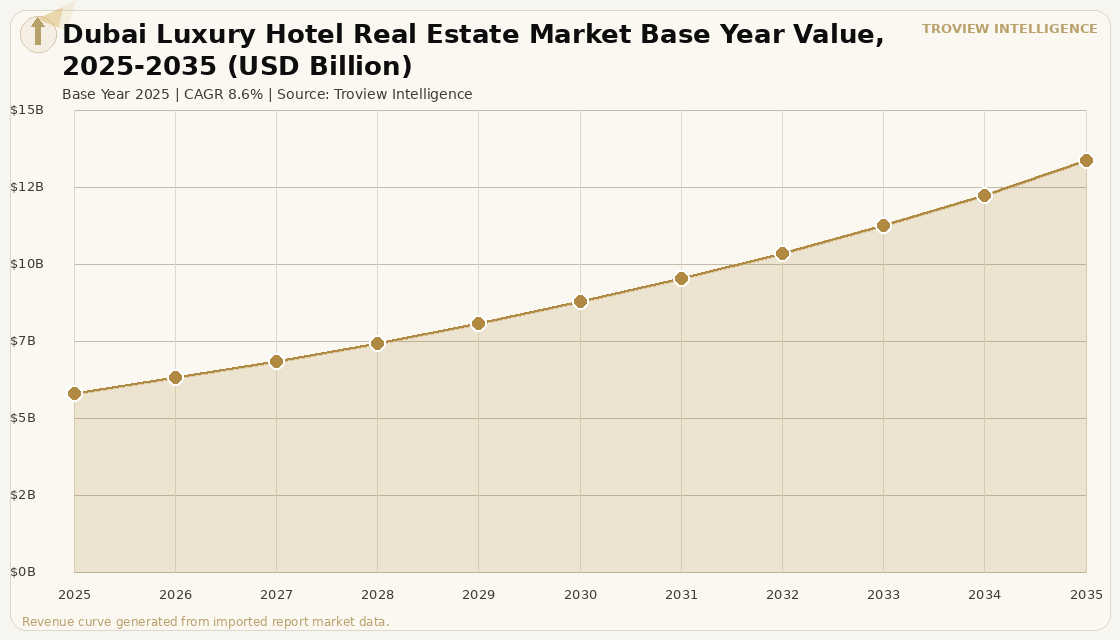

The Dubai luxury hotel real estate market size was USD 5.72 Billion in 2025 and is expected to register a revenue CAGR of 8.6% during the forecast period, reaching USD 13.14 Billion by 2035. Dubai is the Middle East's largest luxury hotel market and one of the world's top ten luxury hotel investment destinations, with a hotel inventory of 152,300 to 158,700 rooms across approximately 730 establishments in 2025, of which five-star and four-star hotels jointly account for 64% of total stock per Cavendish Maxwell Dubai hotel market data. Dubai's luxury hotel segment operates at metrics that benchmark favourably against established global luxury gateways: H1 2025 luxury ADR of approximately AED 1,470 (USD 400) and luxury RevPAR of approximately AED 1,100 (USD 300), citywide occupancy of 81% in H1 2025, and branded luxury properties commanding ADR premiums of 15 to 25% above comparable unbranded inventory per verified hospitality intelligence. Dubai hosted 19.6 million international tourists in full-year 2025, with Western Europe as the largest source market, and the Department of Economy and Tourism confirmed 12.54 million international visitors in January to August 2025 alone a 5.1% year-on-year increase recording 29.03 million occupied room nights and a full-year RevPAR of AED 413 (7.6% year-on-year growth) and ADR of AED 526 (4.6% year-on-year growth) across all hotel categories. For instance, in 2024, Atlantis The Royal, United Arab Emirates, completed its Palm Jumeirah opening at a total development investment of USD 1.4 billion representing approximately USD 2.3 million per key across 795 rooms and suites generating peak ADRs above AED 5,000 (USD 1,360) for suites and establishing the global ultra-luxury hotel development cost benchmark for emerging luxury gateway cities, per verified hospitality investment analysis. These are some of the key factors driving revenue growth of the market.

Dubai's luxury hotel real estate investment market is evolving from a construction-led cycle toward an investment and asset management phase, as Knight Frank confirmed in its UAE Hospitality Market Review Autumn 2025 that increasing regional and international investors are attracted to a maturing market with strong fundamentals and deepening institutional capital. RevPAR growth in Dubai averages 6 to 8% annually, outpacing most established luxury hotel markets globally that are growing at 2 to 4% per year per verified market benchmarking, while the best-run luxury properties target 35 to 40% gross operating profit achievable only through rigorous cost control and experienced luxury hotel management. Conservative debt structures prevail in Dubai luxury hotel financing, with lenders rarely exceeding 60% loan-to-value, pushing many developments into equity-heavy or partnership models with institutional or sovereign investors a structure that limits total leverage risk but concentrates equity return requirements on the operating performance of the asset. Dubai's events calendar global summits, Formula 1, Dubai World Cup, Dubai Airshow, and the expanding MICE infrastructure of the Dubai World Trade Centre provides occupancy anchor events that create predictable premium ADR windows across the calendar year, differentiating Dubai from pure leisure resort markets where seasonal demand volatility requires more aggressive yield management.

However, the Dubai luxury hotel real estate market faces structural constraints that limit the pace of RevPAR growth over the forecast period. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are creating regional security perception concerns for Western European and North American HNWI travellers who collectively account for over a third of Dubai's international visitor base that could dampen luxury hotel occupancy during periods of Hormuz-related news flow even in the absence of any direct impact on Dubai's operational environment. The pipeline of 12,000 new luxury keys by 2030 creates a structural yield compression risk: a 5-point occupancy drop or 10% ADR decline can halve EBITDA margins for luxury properties operating on fixed cost bases where personnel costs constitute 35 to 40% of total operating expenditure, making the 2027 to 2029 new supply delivery window a period of elevated investment risk for luxury hotel assets in Dubai. Third-party OTA dependency with Booking.com and Expedia delivering 35 to 40% of Dubai hotel bookings at commission costs of 15 to 25% erodes profitability for all but the best-capitalised branded properties with mature direct booking programmes, limiting the net RevPAR improvement available to independent luxury operators who lack the global loyalty programme distribution of Marriott Bonvoy and Hilton Honors. These factors substantially limit Dubai luxury hotel real estate market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "Dubai's luxury hotel market is at an inflection point that every mature gateway city reaches eventually: the transition from supply-led growth where new iconic assets create demand and lift the entire market's perception to a competitive equilibrium where RevPAR growth requires operational excellence rather than simply being the newest property in a supply-starved market. The Atlantis The Royal cleared this bar definitively: USD 1.4 billion in development, USD 2.3 million per key, peak ADRs above USD 1,360 for suites. The next 12,000 luxury keys will not all clear this bar. The assets that will outperform in the 2027 to 2030 period are the ones with irreplaceable location premiums Palm Jumeirah waterfront, Downtown Burj Khalifa adjacency, DIFC financial district connectivity and branded operating platforms with proven direct booking capability. The assets that will face RevPAR compression are those that rely on OTA distribution at 15 to 25% commission to fill rooms they cannot fill on their own." Troview Intelligence Senior Analyst, Dubai Luxury Hotel Real Estate

SEGMENT INSIGHTS

SUB-MARKET ANALYSIS

Sub-Market Deep-Dives

| Anchor Development | Development Cost | Peak Suite ADR | Key Operators |

| Atlantis The Royal | USD 1.4 billion (~USD 2.3M per key) | Above AED 5,000 (USD 1,360) | Kerzner, One and Only, Waldorf Astoria |

Palm Jumeirah is Dubai's primary ultra-luxury hotel sub-market, anchored by the USD 1.4 billion Atlantis The Royal development that completed in 2024 and set a new global benchmark for ultra-luxury hotel development cost at approximately USD 2.3 million per key across 795 rooms and suites. The Palm corridor also hosts One and Only The Palm Kerzner International's ultra-exclusive low-key-count resort offering sub-100-room intimacy at ADRs competitive with Atlantis's most premium inventory Waldorf Astoria The Palm, and Sofitel The Palm as the primary five-star alternatives to ultra-luxury pricing. The Palm Jumeirah sub-market benefits from a physical product island isolation, beachfront access, marina views, and architectural spectacle that cannot be replicated in any other Dubai location, providing a genuine scarcity premium that sustains ADR leadership against competing luxury sub-markets Downtown and in JBR. During peak periods including global summits, UAE national celebrations, and New Year's Eve, Palm Jumeirah luxury suites command ADRs above AED 5,000 (USD 1,360), confirming the sub-market's ability to generate luxury performance metrics competitive with the world's most expensive hotel addresses.

| Key Luxury Anchor | Brand Operators | MICE Driver | Occupancy Profile |

| Burj Khalifa and Dubai Mall | Armani Hotel, Address Downtown | Dubai Fountain, events, MICE | Highest year-round consistency |

Downtown Dubai is the city's most consistently high-occupancy luxury hotel sub-market, benefiting from the unique Burj Khalifa adjacency premium that no other global hotel address can replicate and the Dubai Mall footfall of approximately 100 million annual visitors that provides the sub-market with a year-round leisure and retail tourism anchor entirely independent of the events calendar. The Armani Hotel Dubai, designed by Giorgio Armani and located within Burj Khalifa itself, generates the highest brand exclusivity premium in the Downtown sub-market, while the Address Downtown and Address Boulevard provide five-star luxury at scale for the MICE, leisure, and bleisure traveller cohort that dominates the sub-market's occupancy base. Downtown Dubai's luxury hotel occupancy is the most seasonally stable of any Dubai sub-market, with the Burj Khalifa New Year's Eve fireworks display alone generating one of the highest-ADR single nights of the global calendar for any address with direct tower-view rooms. Emaar Properties, UAE, as the developer of the Downtown district, continues to invest in mixed-use luxury assets including branded residences, retail, and hotel product that maintain the sub-market's premium positioning relative to competing Dubai luxury corridors.

| Primary Operator | Anchor Financial Tenants | Corporate ADR Profile | MICE Facilities |

| Four Seasons DIFC, Ritz-Carlton | Goldman Sachs, HSBC, 150+ firms | Highest corporate ADR in Dubai | DIFC convention and event facilities |

The Dubai International Financial Centre sub-market is Dubai's primary corporate and financial services luxury hotel cluster, anchored by the Four Seasons DIFC and The Ritz-Carlton DIFC that serve the corporate travel demand from more than 150 global financial institutions, law firms, and professional services companies with licensed operations in the DIFC free zone. DIFC luxury hotels command the highest corporate ADRs in the Dubai market, as financial sector executives requiring proximity to counterparty institutions, legal advisors, and regulators housed within the DIFC boundaries pay a meaningful location premium over equivalent luxury accommodation in the Palm or Downtown sub-markets. The DIFC Convention Centre and Gate Building event facilities drive a significant MICE premium for adjacent luxury hotels during the Gulf Capital Markets Summit, Dubai Fintech Summit, and International Conference of Insurance Supervisors that collectively generate weeks of near-full-occupancy luxury hotel demand at above-average ADR. Four Seasons Hotels and Resorts, Canada, positioned its DIFC property as the brand's financial district flagship in the Middle East, targeting the HNWI corporate traveller who requires both the proximity to financial infrastructure and the consistent service quality that Four Seasons delivers across its global platform.