| TROVIEW INTELLIGENCE | Extended-Stay and Serviced Apartment Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Geography · By Stay Duration · By End-User Segment · By Booking Mode

The 2025 Global Serviced Apartment Industry Report published by Ariosi and Travel Intelligence Network based on 1.6 million room night bookings through Habicus Group documents a global average daily rate of GBP 145 with London, Paris, and Amsterdam all recording year-on-year variance below 2%, the European Travel Commission confirming an 11% increase in trips lasting seven to twelve nights in 2025 indicating a structural shift toward longer-duration stays, serviced apartments demonstrating a 72% average occupancy rate globally against 65% for traditional hotels per market analysis, extended stays of fourteen to ninety days constituting 48% of total serviced apartment occupancy, corporate and business travellers accounting for approximately 58% of global demand, and Adagio pursuing a target of 200 sites by 2028 while Ascott Limited launched 4 new Citadines-branded properties in Indonesia and Thailand adding 3,200 units in 2024 confirming that the extended-stay and serviced apartment sector is structurally outperforming the broader hospitality market on every primary operating metric.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

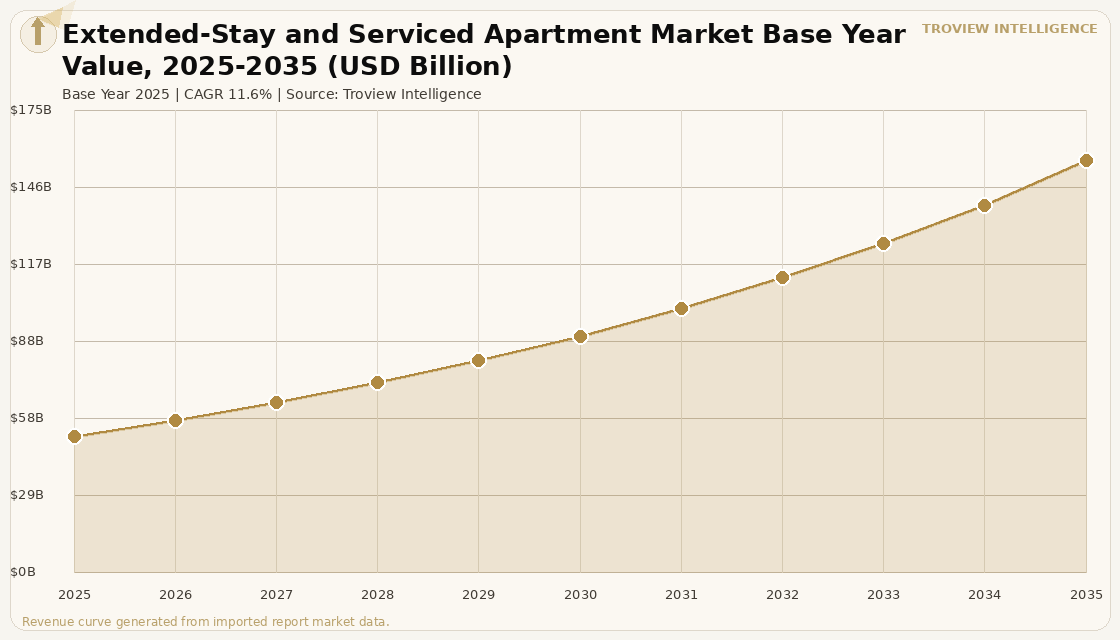

MARKET SYNOPSIS

The global extended-stay and serviced apartment market size was USD 51.84 Billion in 2025 and is expected to register a revenue CAGR of 11.6% during the forecast period, reaching USD 156.28 Billion by 2035. The market encompasses institutionally managed, fully furnished serviced apartment properties offering hotel-grade amenities including housekeeping, concierge, and on-site services, targeting corporate business travellers, expatriates, relocating professionals, and leisure travellers on stays of seven nights and above. Market revenue growth is supported by a structural shift in global travel behaviour toward longer-duration stays: the European Travel Commission confirmed a 11% increase in Europeans planning trips of seven to twelve nights in 2025 alongside a concurrent decline in stays of less than seven nights per Savills European Serviced Apartment Report of April 2026, indicating a durable behavioural transition rather than a cyclical demand spike. Serviced apartments demonstrated a global average occupancy rate of 72% in 2025 against 65% for traditional hotels, with extended stays of fourteen to ninety days constituting 48% of total occupancy and corporate business travellers accounting for approximately 58% of global demand per market analysis, confirming the sector's structural operational advantage over conventional hotel accommodation formats. The UN Tourism World Tourism Barometer recorded a 5% increase in international tourism arrivals in H1 2025 relative to H1 2024, with 690 million arrivals globally and Europe welcoming nearly 340 million tourists, surpassing pre-pandemic levels a demand environment that directly supports occupancy and rate performance for serviced apartment operators in global gateway cities. For instance, in August 2024, Ascott Limited, Singapore, announced plans to open 20 new properties over the next four years as part of its global expansion strategy, targeting key markets across Asia, Europe, and the Americas, with the company having already launched four new Citadines-branded serviced apartments in Indonesia and Thailand adding 3,200 units in 2024 to capitalise on post-pandemic corporate travel and extended-stay demand recovery per Ascott Limited company announcement of August 2024. These are some of the key factors driving revenue growth of the market.

The 2025 Global Serviced Apartment Industry Report published by Ariosi and Travel Intelligence Network based on 1.6 million room night bookings through Habicus Group documented a global average daily rate of GBP 145 with London, Paris, and Amsterdam all recording year-on-year rate variance below 2%, confirming the pricing stability that distinguishes the serviced apartment segment from more rate-volatile hotel accommodation. HVS analysis of the European serviced apartment sector published in 2025 noted that operators across Europe reported a notable increase in average length of stay in 2024, identifying this as a positive structural indicator that the serviced apartment model is aligning with the modern traveller's longer-duration accommodation preferences and shifting back toward the traditional booking pattern of extended occupancy. JLL's US Select-Service and Extended-Stay Hotel Outlook 2025 confirmed that extended-stay formats have outperformed traditional lodging categories in the United States, with RevPAR levels exceeding pre-pandemic benchmarks and disciplined supply additions sustaining average daily rate levels. In July 2024, Staycity Group, Ireland, acquired a site adjacent to Nine Elms Station in London for an undisclosed sum, pursuing GBP 70 million of development funding upon receiving planning clearance for an aparthotel development using an operating leaseback structure per verified trade press, illustrating the active acquisition and development strategies being deployed by European serviced apartment operators in gateway city locations. These are some of the key factors driving revenue growth of the market.

However, the global extended-stay and serviced apartment market faces structural constraints that temper revenue growth across the forecast period. Competition from short-term rental platforms including Airbnb and Vrbo exerts downward pressure on pricing power and occupancy for serviced apartment operators, particularly in leisure-oriented markets where short-term rental supply has expanded materially since 2020 and where platform pricing algorithms respond to real-time demand more dynamically than institutionally managed serviced apartment operators can. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis affecting approximately 20% of global seaborne LNG flows, create upward pressure on utility costs for serviced apartment operators in LNG-dependent electricity markets, as full-service apartment amenities including kitchen appliances, laundry facilities, and climate control generate higher energy consumption per unit than equivalent hotel rooms. The shift toward shorter booking windows and flexible cancellation policies documented in HVS's 2025 European serviced apartment sector analysis complicates revenue management for operators whose cost structure reflects the housekeeping, maintenance, and amenity provision required for extended-stay guests, creating margin pressure when short-notice cancellations replace the predictable long-stay bookings that optimise operating leverage. Regulatory risk in urban markets including rent control ordinances, minimum stay requirements, and licensing frameworks targeting furnished rental properties in cities including Paris, Berlin, and Amsterdam increases operational complexity and limits the geographic pipeline of new serviced apartment development in the highest-demand European markets. These factors substantially limit global extended-stay and serviced apartment market growth over the forecast period.

The serviced apartment sector has a structural advantage over conventional hotels that the market has consistently underpriced relative to traditional hospitality real estate. A seventy-two percent average occupancy rate against sixty-five percent for hotels. Forty-eight percent of stays above fourteen nights, reducing turnover costs to a fraction of hotel equivalents. Corporate contracts providing twelve to thirty-six months of forward booking visibility that no hotel chain can replicate in its transient leisure segment. These are not cyclical performance advantages that reverse when the travel cycle turns. They are structural advantages that compound over time as corporate clients deepen reliance on specific operators and as the demographic of long-duration travellers remote workers, digital nomads, executive relocators continues to grow as a share of total business travel expenditure. The operators who have understood this and invested in building genuine institutional-quality serviced apartment platforms Ascott, Adagio, Frasers, Sonder are not competing with hotels. They are building a separate asset class with different income characteristics, different tenant economics, and a different institutional investor appeal that will take another decade to be correctly priced." Troview Intelligence Head of Global Extended-Stay and Serviced Apartment Research

SEGMENT INSIGHTS

Four Regions Defining Global Serviced Apartment Revenue

| North America Market Share 2025 | US Extended-Stay RevPAR | Corporate Occupancy Share US | Key Growth Cities |

| ~36.55% of global revenue | Above pre-pandemic levels (JLL 2025) | ~62% of total US serviced apartment bookings | Austin (+8% YoY), Denver (+6% YoY) occupancy |

North America is the largest global extended-stay and serviced apartment market, with the United States accounting for the dominant share of revenue driven by a corporate relocation infrastructure that generates multi-month extended-stay demand from technology, financial services, energy, and healthcare employers whose project deployment and talent mobility programmes produce predictable demand for serviced apartment inventory across major metros. JLL's US Select-Service and Extended-Stay Hotel Outlook 2025 confirmed that extended-stay formats have outperformed traditional lodging categories, with RevPAR levels exceeding pre-pandemic benchmarks, as disciplined supply additions sustained average daily rate levels in primary markets. Corporate housing demand contributed to approximately 62% of total US serviced apartment occupancy, with relocation and temporary assignment demand adding a further 21%, while cities including Austin and Denver recorded year-on-year occupancy growth of 8% and 6% respectively as corporate relocation activity shifted toward Sun Belt technology hubs per market analysis. Over 70% of US-based serviced apartments offered full kitchen facilities in 2024, with 68% of guests rating privacy and extended-stay convenience as key decision drivers per market analysis, reinforcing the segment's differentiation from standard hotel accommodation.

| European Pipeline to 2030 | Global ADR 2025 | HVS 2025 Finding | Pipeline Leaders |

| ~16,500 new rooms | GBP 145 (London, Paris, Amsterdam <2% variance) | Average length of stay increased notably in 2024 | UK 30%, Germany 20%, Spain+France 6% each |

Europe's extended-stay and serviced apartment market is characterised by the highest average stay durations globally, the deepest institutional operator pipeline, and the most concentrated corporate demand base in global gateway cities including London, Paris, Amsterdam, Frankfurt, and Zurich. The 2025 GSAIR documented a global ADR of GBP 145 with London, Paris, and Amsterdam all recording year-on-year rate variance below 2%, demonstrating the pricing stability that comes from a corporate contract-dominated booking base rather than leisure transient demand. HVS's 2025 European serviced apartment sector analysis noted that operators reported a notable increase in average length of stay in 2024 and identified the trend as a structural indicator of the model's alignment with modern traveller preferences. The European serviced apartment pipeline is expected to add approximately 16,500 rooms by 2030 per GSAIR 2025, with the UK accounting for 30% of the pipeline, Germany 20%, and Spain and France contributing approximately 6% each, reflecting the institutional capital and operator development activity concentrated in the continent's major business travel hubs.

| APAC Pipeline Share 2025 | Key Growth Markets | Ascott New Properties | India Expansion |

| ~38% of all upcoming branded projects globally | Singapore, Tokyo, Mumbai, Bengaluru, Shanghai | 4 new Citadines launches, 3,200 units added, 2024 | Ascott announced Aug 2024 multi-city India strategy |

Asia Pacific is the fastest-growing extended-stay and serviced apartment region globally, holding approximately 38% of all upcoming branded serviced apartment developments under construction as of 2025, driven by corporate travel demand across the region's major technology, financial services, and manufacturing business hubs and by the expansion of Global Capability Centre infrastructure in India and Southeast Asia that generates sustained demand for extended-stay accommodation from international professionals on two-to-twelve-month assignments. Ascott Limited, Singapore, the largest branded serviced apartment operator globally, announced in August 2024 its plans to expand in India across major cities, capitalising on rising demand from business travel and extended stays as part of its broader global expansion agenda, having already launched four new Citadines-branded properties in Indonesia and Thailand adding 3,200 units to its portfolio in 2024. In July 2024, Ascott announced a global partnership with Chelsea FC enhancing brand visibility across its global markets per Ascott company announcement. Singapore, Tokyo, and Hong Kong remain the Asia Pacific markets with the highest average daily rates for branded serviced apartments, driven by the concentration of multinational corporation regional headquarters and the sustained demand from expatriate professional communities that make long-term branded serviced apartment supply consistently undersupplied relative to demand in these gateway cities.