| TROVIEW INTELLIGENCE | France Extended-Stay and Serviced Apartment Market | Q2 2026 |

| TROVIEW INTELLIGENCE · COUNTRY INTELLIGENCE REPORT |

By City · By Stay Duration · By End-User Segment · By Booking Mode

The France serviced apartment market reached USD 3.46 billion in 2024 and the Ile-de-France region accounted for 33.05% of the French hospitality market in 2025, with Adagio operating 41 aparthotels across Ile-de-France comprising 21 Adagio Access and 20 Adagio Original properties and planning three additional openings in 2026, corporate and business travellers accounting for nearly half of France market revenue in 2024 as multinationals, conference organisers, and trade fair participants generate sustained extended-stay demand across Paris, Lyon, and Marseille, Adagio targeting 200 sites by 2028 reflecting institutional confidence in France's position as a primary European business hub, and the European Travel Commission recording an 11% increase in Europeans planning seven-to-twelve-night trips in 2025 that directly benefits France's premier luxury and leisure extended-stay destinations, confirming that France is simultaneously the EU's leading corporate extended-stay market by occupancy depth and its fastest-growing leisure extended-stay destination by stay duration.

| Standard License: USD 6,500 | Enterprise License: USD 9,500 |

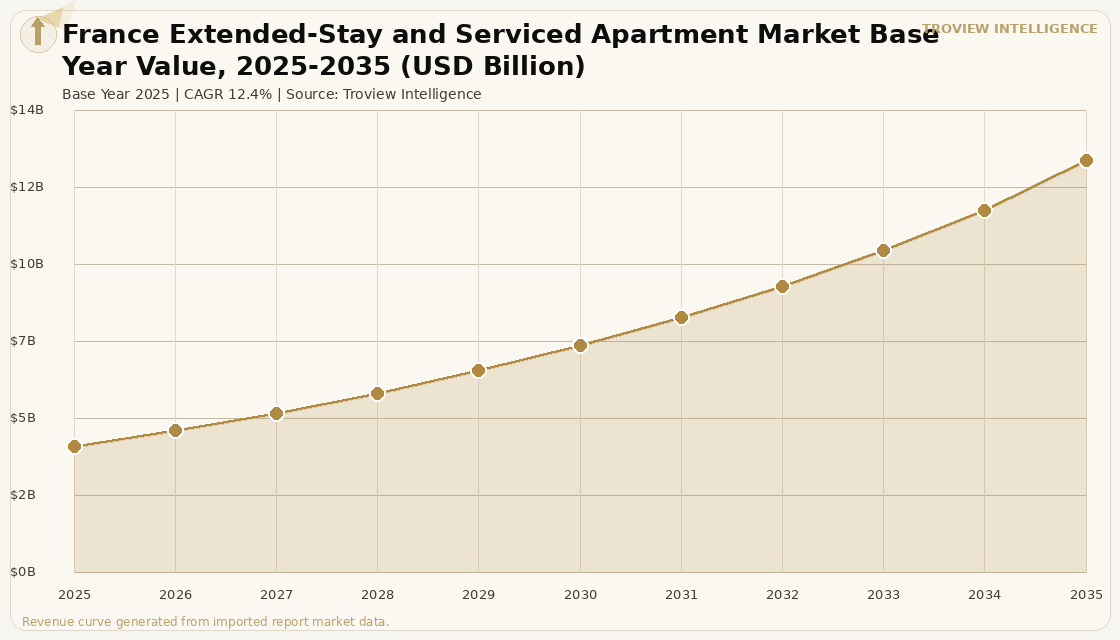

MARKET SYNOPSIS

The France extended-stay and serviced apartment market size was USD 3.94 Billion in 2025 and is expected to register a revenue CAGR of 12.4% during the forecast period, reaching USD 12.84 Billion by 2035. Market revenue growth is supported by France's structural position as one of Europe's most active corporate extended-stay markets, driven by the country's role as host to the European headquarters of multinational corporations, the Paris-based conference and trade fair calendar anchored by venues including Paris Expo Porte de Versailles and Palais des Congres, and the expanding base of expatriate professionals undertaking intra-company transfers and project-based relocations to Paris, Lyon, and the broader La Defense business district. Corporate and business travellers accounted for nearly half of France serviced apartment market revenue in 2024, with the expats and relocators segment identified as the fastest-growing demand cohort through 2033 per Adagio operational disclosures and Accor Investor Day 2025 data, driven by rising numbers of international students, diplomatic staff, and executives on intra-company transfers who prioritise convenience, security, and proximity to workplaces. The Ile-de-France region accounted for 33.05% of the French hospitality market in 2025 per UNWTO France inbound tourism data and Adagio Investor communications, and serviced apartments secured the fastest CAGR of any accommodation category through 2031 within the French hospitality market, with brands including Adagio targeting 200 sites by 2028 illustrating the category's institutional traction and capacity to scale within urban footprints per Adagio corporate communications and Accor Investor Day 2025. For instance, in February 2026, Adagio, France, the joint venture between Accor and Pierre and Vacances, opened the 132-unit Adagio Access Nanterre Aparthotel in La Defense in western Paris, the ninth property developed in partnership with Sergic, with Adagio's director of development Arthur Jaeger confirming that the Nanterre opening demonstrates the operator's commitment to strengthening its presence in the most dynamic regions and that three additional Ile-de-France openings are planned for 2026 per Serviced Apartment News reporting of February 2026. These are some of the key factors driving revenue growth of the market.

The France serviced apartment market reached USD 3.46 billion in 2024 per Adagio and Accor group operational data, with the market characterised by a direct booking dominance driven by long-stay corporate guests who prefer direct agreements with operators to secure customised payment terms, tailored service packages, and the multilingual support staff that multinational corporate clients require for their relocating employees. UN Tourism's World Tourism Barometer recorded that Europe welcomed nearly 340 million tourists in H1 2025, surpassing pre-pandemic levels per the organisation's biannual report, with France maintaining its position as the world's most visited country and Paris generating a sustained international leisure demand base that supports serviced apartment occupancy beyond the corporate segment through extended leisure stays. The post-pandemic rise of hybrid and remote work has expanded the France serviced apartment market's demand base beyond traditional corporate clients to include professionals on temporary assignments or workcation stays seeking flexible, fully furnished spaces with work-friendly amenities in Paris and France's other major urban centres. Lodgis, France, which manages a portfolio of over 10,000 furnished apartments serving corporate clients including relocation agencies and multinationals across Paris and Lyon, provides a benchmark for the depth of corporate housing demand in the French market, with the company offering corporate apartment solutions for stays ranging from one month to multiple years across all Paris arrondissements per Lodgis company information. These are some of the key factors driving revenue growth of the market.

However, the France extended-stay and serviced apartment market faces regulatory and competitive constraints that temper revenue growth across the forecast period. The French regulatory environment for furnished rental properties has become progressively more complex, with Paris imposing minimum stay requirements and furnished rental registration obligations on properties offered through short-term rental platforms and municipal authorities in Lyon, Marseille, and Bordeaux implementing or strengthening restrictions on the conversion of long-term residential housing to furnished tourist accommodation requirements that increase compliance costs for operators and limit the geographic pipeline of new serviced apartment development in France's highest-demand urban submarkets. Competition from Airbnb and Vrbo, which collectively aggregate a substantial volume of French furnished rental supply operating outside the institutional serviced apartment framework, exerts downward pricing pressure in leisure-oriented markets where online platform pricing responds dynamically to real-time demand in a way that institutionally managed serviced apartment operators cannot fully match. Iran-US geopolitical tensions and resulting energy price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, create upward pressure on French energy costs given the country's partial dependence on gas-fired peaking generation and LNG imports, increasing operating expenses for serviced apartment operators whose full kitchen, laundry, and climate control amenities generate above-average per-unit energy consumption. These factors substantially limit France extended-stay and serviced apartment market growth over the forecast period.

France's serviced apartment market has a structural demand advantage that no other European country except Germany can match: a corporate tenant base that is genuinely multinational at scale. The Paris La Defense business district hosts the European headquarters of more Fortune 500 companies than any other location outside London, and each of those headquarters generates a continuous flow of intra-company transfer, project deployment, and executive relocation demand that cannot be served by hotels. A relocating executive from New York who is assigned to Paris for eighteen months needs a two-bedroom apartment in the 8th arrondissement with a full kitchen, French-speaking concierge support, and a company lease that can be extended quarterly. Adagio, Frasers, and the institutional operators who serve that demand are not competing with Airbnb. They are the corporate housing infrastructure of the French economy's international business class. The operators who have built genuine scale in Paris Adagio's 41 Ile-de-France properties, Lodgis's 10,000-unit corporate portfolio understand this. The institutional investors who have not yet correctly priced this asset class are still catching up." Troview Intelligence Head of France Extended-Stay and Serviced Apartment Research

SEGMENT INSIGHTS

| 03 | CITY PROFILE ANALYSIS |

Five Cities Defining France's Extended-Stay and Serviced Apartment Market

| Ile-de-France Hospitality Share | Adagio Ile-de-France Portfolio | Global ADR 2025 | Primary Demand Driver |

| 33.05% of French hospitality market (2025) | 41 properties (21 Access + 20 Original); 3 opening 2026 | GBP 145 Paris <2% YoY variance (GSAIR 2025) | La Defense MNC HQs, diplomatic missions, UNESCO/OECD |

Paris is France's largest and most institutionally mature extended-stay and serviced apartment market, accounting for the majority of the country's corporate serviced apartment demand through the concentration of multinational corporate headquarters in La Defense and the central business districts of the 8th, 16th, and 17th arrondissements, whose collective intra-company transfer and executive relocation activity represents the most consistent and highest-value corporate extended-stay demand base in continental Europe. Adagio operates 41 aparthotels across the Ile-de-France region as of early 2026, comprising 21 Adagio Access and 20 Adagio Original properties, with the February 2026 opening of Adagio Access Nanterre in La Defense bringing the company's west Paris presence directly adjacent to the La Defense business district that houses the French and European headquarters of corporations including Total, LVMH, Societe Generale, Capgemini, and dozens of international multinationals per Serviced Apartment News reporting. The 2025 GSAIR recorded a Paris ADR of approximately GBP 145 with year-on-year variance below 2%, illustrating the pricing resilience that comes from a corporate contract-dominated demand base whose booking volumes are less sensitive to macroeconomic fluctuations than leisure transient accommodation. Lodgis manages over 10,000 furnished corporate apartments in Paris and Lyon, offering the deepest single-operator corporate housing portfolio in France's primary market per Lodgis company information.

| Key Demand Drivers | Major Conference Venue | Corporate Housing Depth | Infrastructure |

| Biotech, pharma, manufacturing, trade fairs | Eurexpo Lyon leading trade fair host | Lodgis corporate portfolio in Paris and Lyon | TGV 2hrs Paris, Lyon-Saint Exupery international airport |

Lyon is France's fastest-growing corporate extended-stay and serviced apartment market, anchored by a business cluster in biotechnology, pharmaceuticals, agribusiness, manufacturing, and financial services whose multinational component generates sustained demand for extended-stay accommodation from international professionals on assignment to the Lyon metropolitan area. The Eurexpo Lyon exhibition and convention centre, one of France's leading trade fair venues, generates periodic high-demand spikes for serviced apartment capacity from conference participants requiring accommodation above standard hotel availability during major events including Sirha, Pollutec, and Batimat. Lyon's position as a European biotech hub with major pharmaceutical company operations from Sanofi and Boehringer Ingelheim, alongside the concentration of technology and digital companies that have established Lyon offices as an alternative to Parisian cost levels, creates a structural corporate extended-stay demand base that is expanding at above the national average growth rate. Lyon's accessibility by TGV from Paris in two hours and its international airport connectivity to European and Middle Eastern hubs makes it a secondary but complementary market to Paris for corporate serviced apartment operators expanding their French national footprint.

MARSEILLE, BORDEAUX AND TOULOUSE REGIONAL GROWTH MARKETS LEISURE AND AEROSPACE DEMAND

| Marseille Driver | Bordeaux Driver | Toulouse Driver | PACA CAGR to 2031 |

| Port industry, Euroméditerranée urban project, tourism | Wine tourism, corporate expansion, university population | Airbus, aerospace industry, student and engineer demand | 5.52% Provence-Alpes-Cote d'Azur |

Marseille, Bordeaux, and Toulouse represent France's three primary regional extended-stay and serviced apartment growth markets, each driven by a distinct demand profile that differentiates them from the pure corporate demand base of Paris and Lyon. Marseille's serviced apartment market is driven by the Euroméditerranée urban regeneration project one of France's largest urban renewal programmes combined with port industry corporate demand and Mediterranean leisure tourism, with the Provence-Alpes-Cote d'Azur region projected to grow at a 5.52% CAGR through 2031 per Adagio and Accor group regional operational data. Bordeaux combines wine tourism leisure demand with a growing corporate and technology sector relocating from Paris, attracting operators seeking to deploy serviced apartment inventory in markets where residential property values are lower than Paris but where corporate demand growth is outpacing supply additions. Toulouse is the primary aerospace and defence extended-stay market in France, with Airbus's global headquarters and the city's concentration of aerospace engineering, satellite, and defence technology companies generating sustained corporate extended-stay demand from international engineers and executives on multi-month assignment programmes.