By Asset Type · By Geography · By End-User · By Building Grade

Global net absorption of logistics real estate accelerated to 436 million square feet on a seasonally adjusted annual basis in the second half of 2025 per Prologis Research, with net absorption outpacing new supply in Q4 2025 and pushing vacancy down as Prologis recorded record lease signings of 228 million square feet for the full year a market inflection that positions rent growth to accelerate through 2026 as construction completions fall and first-generation supply is absorbed.

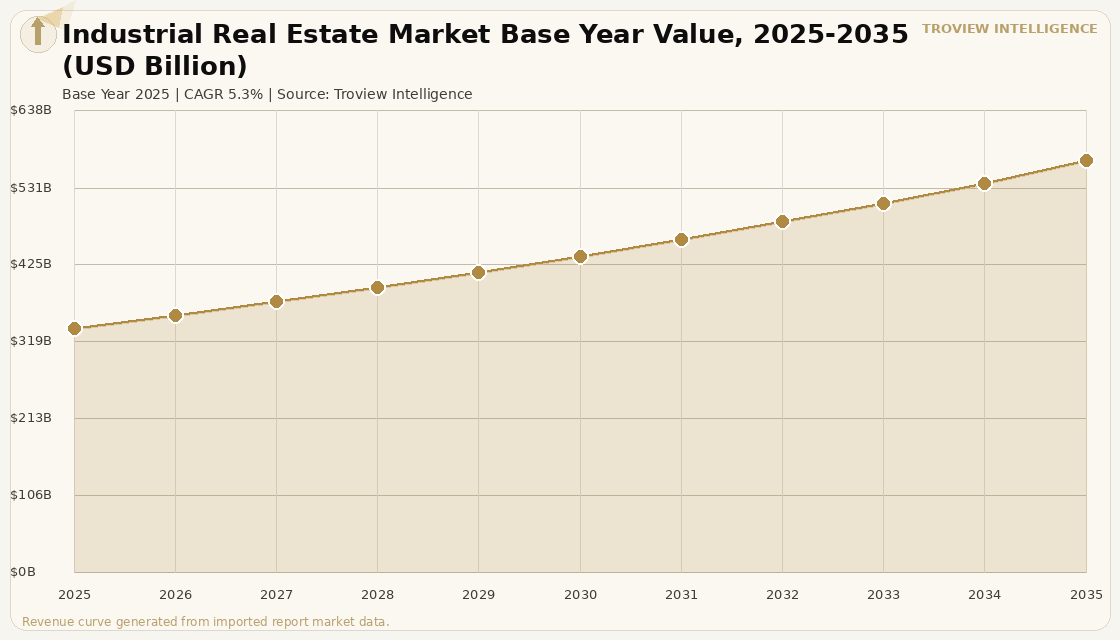

MARKET SYNOPSIS

The global industrial real estate market size was USD 337.62 Billion in 2025 and is expected to register a revenue CAGR of 5.3% during the forecast period, reaching USD 569.42 Billion by 2035. Market revenue growth is supported by structural demand from e-commerce expansion, supply chain nearshoring, and the proliferation of large-format logistics facilities serving last-mile delivery networks in high-density urban corridors. Prologis, the global leader in logistics real estate, recorded record lease signings of 228 million square feet in 2025, with e-commerce tenants representing approximately 20% of those transactions per Prologis Q4 2025 investor disclosures. Global net absorption accelerated to 436 million square feet on a seasonally adjusted annual basis in the second half of 2025, rising from a pace of 393 million square feet in the first half of the year per Prologis Research. Net absorption outpaced new supply in Q4 2025, pushing vacancy down 10 basis points quarter-over-quarter to 7.4%, with Prologis citing this as confirmation that the US logistics real estate market shifted materially by the end of 2025 and that vacancy rates were at or near their cyclical peak.

Industrial real estate has emerged as the most sought-after institutional real estate asset class of the past decade, with Prologis, Blackstone, and sovereign wealth funds competing for logistics parks, distribution centres, and last-mile fulfilment assets across North America, Europe, and Asia Pacific. The e-commerce share of total US retail sales, excluding autos and gasoline, hit a record 23.2% in Q3 2024 and was projected to reach 25.0% by year-end 2025 per US Census Bureau retail trade data, sustaining the structural demand that underpins rent growth in well-located warehouse and distribution facilities. Supply chain resilience priorities following pandemic-era disruptions have driven a nearshoring and onshoring trend, with more than 60% of companies planning to move manufacturing facilities closer to end markets per US Department of Commerce sector surveys, generating demand for new industrial facilities in domestic manufacturing corridors. Third-party logistics providers accounted for 34.1% of bulk industrial leasing activity through Q3 2024, rising from 30.6% in the prior year per industry transaction data, confirming their role as the market's most active and fastest-growing occupier segment. For instance, in Q2 2025, Prologis, United States, recorded 43.8 million square feet of lease starts during the fourth quarter alone, while the company's Prologis Industrial Business Indicator Utilisation Rate trended above 85% in Q2 2025, 50 basis points above full-year 2024 averages as customers front-loaded inventories ahead of changing trade policies, per Prologis Q2 2025 research publication. These are some of the key factors driving revenue growth of the market.

However, the global industrial real estate market faces structural constraints that moderate growth. The post-pandemic construction surge delivered an excess of new supply in several major markets, particularly in the United States where more than 400 million square feet of the nearly one billion square feet of new industrial supply added since Q1 2023 remained vacant as of late 2024 per US industry transaction data. National US industrial asking rents posted only approximately 1.4% year-on-year growth as of late 2025, a sharp deceleration from the 9 to 10% annual gains recorded at the 2022 peak, as elevated vacancy in newer product and ongoing tenant flight to quality reduced the leverage of landlords holding older secondary buildings. Global logistics real estate rents declined by approximately 5% in 2024 per Prologis Research as the first broad reversal of rent growth since 2010, reflecting elevated supply and subdued demand in markets including Europe and the United States. Manufacturing-heavy regions in Mexico, Canada, and China faced demand and rental headwinds from uncertainty around trade policies that dampened expansion decisions by large industrial users. These factors substantially limit global industrial real estate market growth over the forecast period.

Industrial real estate spent 2024 and 2025 digesting the fastest construction cycle in modern history. The 2026 setup is straightforward: completions are falling, absorption is rising, and utilisation is at 85 percent with inventories lean. The markets that attract rent growth fastest in 2026 will be the ones where first-generation space is fully absorbed and speculative construction has stopped and that list is led by high-barrier coastal markets and secondary cities where manufacturing and nearshoring are generating genuine new demand rather than demand deferred from pandemic-era growth." Troview Intelligence Head of Global Industrial Real Estate Research

SEGMENT INSIGHTS

By Asset Type

Warehouse and distribution facilities are expected to account for a significantly large revenue share in the global industrial real estate market during the forecast period.

Based on asset type, the global industrial real estate market is segmented into warehouse and distribution, manufacturing facilities, flex and light industrial, cold storage, and data centres. Warehouses and distribution centres dominate by floor area and transaction volume, accounting for the majority of leasing activity driven by third-party logistics operators, e-commerce fulfilment platforms, and major retail chains building out dedicated logistics networks. Cold storage is the fastest-growing segment, as post-pandemic demand for refrigerated grocery fulfilment and pharmaceutical supply chain investment has driven sustained development of temperature-controlled facilities in proximity to urban consumption centres. Prologis's utilisation data tracking approximately 85% across its global portfolio confirms that modern distribution warehouses are operating near the occupancy threshold above which supply constraints generate meaningful rent growth.

By Geography

North America is expected to account for a significantly large revenue share in the global industrial real estate market during the forecast period.

Based on geography, the global industrial real estate market is segmented into North America, Europe, Asia Pacific, and Middle East and Africa. North America dominates global industrial real estate revenue, underpinned by the United States' largest institutional logistics real estate market in the world, with Prologis, Blackstone, and major pension funds holding diversified portfolios across Sun Belt, Midwest, and coastal gateway markets. Asia Pacific is expected to register the fastest revenue CAGR, driven by India's logistics park development programme, China's continued warehouse network expansion serving its vast domestic e-commerce base, and Japan's sustained demand for modern cold storage and fulfilment facilities from its ageing e-commerce platform operators. Europe's industrial market is recovering from a 1% net effective rent decline in 2024, the first since 2010, as demand stabilises and new construction slows.

By End-User

Third-party logistics providers are expected to account for a significantly large revenue share in the global industrial real estate market during the forecast period.

Based on end-user, the global industrial real estate market is segmented into third-party logistics providers, e-commerce operators, retailers, manufacturers, cold chain operators, and government and defence tenants. Third-party logistics providers dominated bulk industrial leasing with 34.1% of transactions above 100,000 square feet through Q3 2024 per industry transaction records, growing their share from 30.6% in the prior period as outsourced logistics management expanded across retail and manufacturing supply chains. E-commerce operators are the fastest-growing end-user category by new lease volume, with Prologis recording e-commerce tenants at approximately 20% of 2025 new deals as last-mile fulfilment requirements drive repeated facility upgrades and expansions in markets with strong population growth and high consumer spending.

REGIONAL ANALYSIS

NORTH AMERICA LARGEST

| US Vacancy Q4 2025 | 7.4% (-10 bps QoQ, Prologis) | Prologis Lease Signings 2025 | 228 million sq ft (record) |

| 3PL Share of Bulk Leasing | 34.1% (through Q3 2024) | US Construction Decline | Completions expected down 50% in 2025 vs 2022 peak |

North America is the largest global industrial real estate market, led by the United States where Prologis Research documented vacancy falling to 7.4% in Q4 2025 as net absorption exceeded new supply for the first time in the post-boom correction. Record lease signings of 228 million square feet for full-year 2025 and a utilisation rate above 85% signal a market that has absorbed its excess inventory and is approaching the conditions that historically precede rent growth acceleration. Dallas-Fort Worth, Atlanta, Chicago, and New Jersey-Pennsylvania remain the core markets, while nearshoring-driven manufacturing corridors including Texas, Tennessee, and the Carolinas are generating new demand from domestic and foreign manufacturers relocating production closer to US consumer markets. Canada's manufacturing-adjacent markets in Ontario and Quebec faced trade policy headwinds in 2025 that moderated demand from cross-border logistics users.

EUROPE RECOVERY FROM

| European Rent Growth 2024 | -1% (first decline since 2010, Prologis Research) | Key Markets | Germany, Netherlands, Poland, United Kingdom |

| Demand Driver | E-commerce, nearshoring, cold chain | Construction Trend | Slowing starts improving supply-demand balance |

Europe's industrial real estate market is recovering from a 2024 correction in which net effective rents declined 1% year-on-year for the first time since 2010, driven by elevated supply from Germany and the Netherlands and subdued demand as retailers and logistics operators deferred expansion decisions. Germany, the Netherlands, and Poland remain the largest European markets by new logistics development volume, anchored by their position as the primary entry and distribution points for goods entering continental Europe. The United Kingdom's industrial and logistics market showed relative resilience, supported by e-commerce penetration rates higher than continental Europe and a tight supply of Grade A warehouse space near London and major conurbations. Construction starts are declining across Europe, with the supply-demand imbalance expected to self-correct as new completions slow through 2026 and 2027.

ASIA PACIFIC

| Global Net Absorption H2 2025 | 436 MSF (seasonally adjusted, Prologis Research) | Japan | Sustained cold storage and fulfilment demand |

| India | National Logistics Policy driving park development | China | Domestic e-commerce sustaining warehouse absorption |

Asia Pacific is the fastest-growing industrial real estate region, driven by India's National Logistics Policy which targets a reduction in logistics costs from 14% to 8% of GDP and has designated multi-modal logistics parks in 35 locations across the country, generating direct demand for institutional-grade warehouse and distribution facilities. China's domestic e-commerce market, the world's largest by transaction volume, sustained demand for logistics warehouses and urban fulfilment centres despite broader property market weakness, as JD.com, Alibaba, and Pinduoduo continued to expand their dedicated fulfilment networks. Japan's industrial market attracted sustained institutional investment from Prologis, GLP, and Mitsubishi Estate as demographic trends supporting food e-commerce and pharmacy delivery drove cold storage and temperature-controlled fulfilment demand. Singapore and South Korea serve as gateway logistics hubs for Southeast Asian manufacturing and distribution networks.