By Port Type · By Geography · By Asset Class · By Occupier

Port-adjacent industrial rents climbed 65% between 2019 and 2023 and remain 33% higher than the national US average, yet port-proximate markets captured only 19% of US net absorption in 2025 the lowest share in 15 years as occupiers redesigned logistics networks around cost, resilience, and flexibility, while the Reshoring Initiative documented USD 60 billion in US manufacturing reshoring in 2025 and the Laredo-Nuevo Laredo land port processed the largest commercial vehicle volumes of any US land border crossing, anchoring the nearshore industrial corridor that defines the Mexico-US port-adjacent manufacturing market.

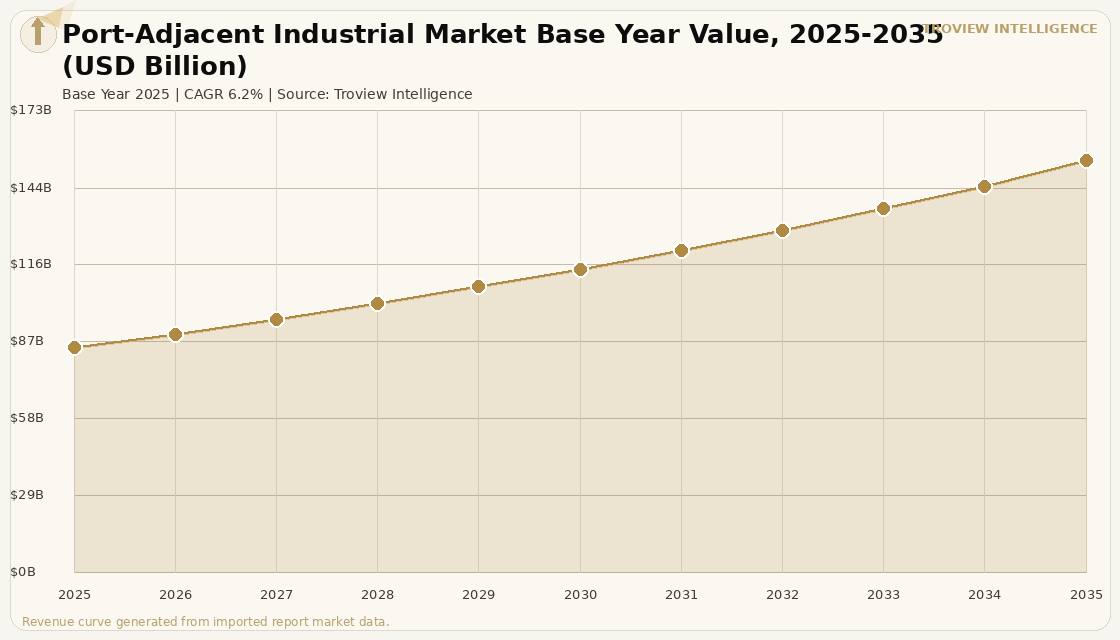

MARKET SYNOPSIS

The global port-adjacent industrial market size was USD 84.46 Billion in 2025 and is expected to register a revenue CAGR of 6.2% during the forecast period, reaching USD 154.82 Billion by 2035. Port-adjacent industrial real estate encompasses facilities located within immediate proximity of seaports, land border crossings, and intermodal terminals assets that command a structural rent premium due to their ability to reduce container dwell time, customs processing costs, and first-mile freight distances. Industrial rents in port markets climbed 65% between 2019 and 2023 and remain 33% higher than the national US average per industry analysis, reflecting the enduring locational premium that proximity to container terminals, roll-on roll-off facilities, and bonded warehouse zones commands. Port-adjacent industrial assets occupy the highest-rent tier of the global logistics real estate market, where lease duration, covenant strength, and cargo throughput volume sustain institutional investment at cap rates materially below those available in inland markets. Cargo volumes at the 10 largest US maritime ports declined just 0.3% in 2025 despite ongoing geopolitical uncertainty and tariff volatility, per industry trade flow data, confirming the resilience of port throughput that underpins long-term demand for proximate industrial real estate.

The global port-adjacent industrial market is simultaneously experiencing the highest structural rent premiums in its history and a shift in new leasing activity toward inland markets, creating a bifurcated investment landscape. Port-proximate markets captured just 19% of total US industrial net absorption in 2025, the lowest share in 15 years per industry analysis, as industrial rents 33% above the national average have redirected large-format distribution requirements particularly facilities above 500,000 square feet to lower-cost inland locations where land availability enables the campus formats that mega-DC operators require. Port markets recorded only 2% growth in industrial demand in 2025 versus 21% growth across inland markets per industry analysis, reflecting a broader reconfiguration of supply chains away from linear port-to-distribution-centre models toward multi-node networks. The Reshoring Initiative documented USD 60 billion in US manufacturing reshoring in 2025, with over 62% of new investments located more than 200 miles inland, generating demand for distribution centres positioned near production rather than ports. For instance, in December 2025, GreensPORT Industrial Park in Houston, United States, reached 100% occupancy in less than one month after completion, with the 38-acre port-adjacent development providing direct access to Gulf Coast port terminals and attracting tenants supporting Gulf Coast supply chains, per FreightWaves reporting of February 2026. These are some of the key factors driving revenue growth of the market.

However, the global port-adjacent industrial market faces structural constraints. Rising costs in coastal logistics markets are contributing to occupier flight to inland alternatives, with industrial rents in the top US port-proximate markets including Long Beach at USD 1.72 per square foot above the national average and Newark at USD 1.68 per square foot above average, creating a meaningful cost disadvantage for large-format tenants that can accept the delivery time trade-off of an inland location. Land scarcity within viable port proximity zones constrains new supply and forces occupiers to choose between paying premium rents for existing port-adjacent stock or relocating inland, compressing the addressable tenant pool for new port-adjacent development. US-China trade policy shifts and the associated diversion of container traffic have disrupted the established flow patterns of major ports including Los Angeles and Long Beach, with cargo diversions to East Coast and Gulf Coast ports creating temporary geographic mismatches between established port-adjacent industrial supply and new cargo flows. Security risks at key land border crossings in Mexico, including periodic cartel-related freight disruptions, create operational uncertainty for port-adjacent industrial users in the cross-border manufacturing corridor. These factors substantially limit global port-adjacent industrial market growth over the forecast period.

Port-adjacent industrial is the most permanent, least substitutable tier of the logistics real estate market. You cannot move a container port. You cannot replicate Laredo's position as the entry point for 40% of all US-Mexico overland trade. The rent premium is not irrational it reflects locational scarcity that no amount of inland development can replicate. What is changing is which functions need to be port-adjacent. Cross-dock and transloading operations, bonded warehouses, and container freight stations must be at the port. Large-scale bulk distribution can move inland. The market is not losing port-adjacent demand. It is segmenting it more precisely." Troview Intelligence Head of Global Port-Adjacent Industrial Research

SEGMENT INSIGHTS

By Port Type

Seaport-adjacent industrial facilities are expected to account for a significantly large revenue share in the global port-adjacent industrial market during the forecast period.

Based on port type, the global port-adjacent industrial market is segmented into seaport-adjacent, land border crossing-adjacent, airport-adjacent airfreight industrial, and intermodal terminal-adjacent logistics parks. Seaport-adjacent facilities dominate by investment value and rent premium, anchored by the Ports of Los Angeles and Long Beach in Southern California, the Port of New York and New Jersey, and the Port of Rotterdam in the Netherlands, where container throughput volumes sustain constant demand for cross-dock, transloading, and container freight station operations that cannot be performed inland without adding cost and transit time. Land border crossing-adjacent industrial is the fastest-growing segment globally, driven by the nearshoring trend that is concentrating new manufacturing investment in Mexico's northern border cities and the corresponding logistics real estate demand at Laredo-Nuevo Laredo, El Paso-Ciudad Juárez, and Otay Mesa-Tijuana crossings where Mexican production enters the US market.

By Geography

North America is expected to account for a significantly large revenue share in the global port-adjacent industrial market during the forecast period.

Based on geography, the global port-adjacent industrial market is segmented into North America, Asia Pacific, Europe, and Middle East and Africa. North America dominates global port-adjacent industrial revenue, with the Inland Empire adjacent to the Ports of Los Angeles and Long Beach, the New Jersey-Pennsylvania corridor near the Port of New York and New Jersey, and the Laredo border corridor serving Mexico-US manufacturing trade generating the three highest-revenue port-adjacent industrial concentrations globally. Asia Pacific is expected to register the fastest revenue CAGR, driven by Singapore's Jurong Industrial Estate, Japan's Tokyo Bay industrial corridor, and India's port-adjacent logistics park development under the Sagarmala programme, which is investing in port connectivity to create the infrastructure prerequisites for institutionally developed port-adjacent industrial parks. Europe's port-adjacent industrial market is led by the Netherlands' Rotterdam-Maasvlakte logistics zone and Germany's Hamburg port industrial district.

By Asset Class

Cross-dock and transloading facilities are expected to account for a significantly large revenue share in the global port-adjacent industrial market during the forecast period.

Based on asset class, the global port-adjacent industrial market is segmented into cross-dock and transloading facilities, container freight stations and bonded warehouses, cold chain port-adjacent facilities, port-adjacent manufacturing and light industrial, and last-mile delivery hubs. Cross-dock and transloading facilities dominate port-adjacent industrial revenue because they represent the function most exclusively dependent on port proximity, handling the transfer of goods from ocean containers to domestic truck or rail without intermediate storage. Cold chain port-adjacent facilities are the fastest-growing asset class, as the expansion of refrigerated food imports and pharmaceutical cold chain logistics has driven development of temperature-controlled facilities immediately inside port perimeters that can maintain cold chain integrity from vessel unloading through customs clearance.

REGIONAL ANALYSIS

NORTH AMERICA RENT PREMIUM

| Port Market Rent Premium | 33% above national US average (industry analysis) | Port Market Absorption Share 2025 | 19% of US net absorption (lowest in 15 years) |

| US Reshoring 2025 | USD 60 billion (Reshoring Initiative) | Key Markets | Inland Empire, NJ-PA, Savannah, Houston, Laredo-NL |

North America's port-adjacent industrial market commands the highest per-square-foot rents of any industrial real estate segment, with Long Beach at USD 1.72 per square foot above the national average and Newark at USD 1.68 above average per industry analysis. The fundamental tension in the North American market is between the irreplaceable locational value of port proximity and the cost reality that has redirected large-format distribution requirements to inland alternatives. The Laredo-Nuevo Laredo land port of entry, the busiest commercial land border crossing in the United States by trade value, anchors a distinct category of port-adjacent industrial demand driven by Mexico-US manufacturing trade rather than ocean container flows. Savannah, Georgia, anchored by the Ports of Savannah, has become one of the fastest-growing port-adjacent industrial markets in the eastern US, benefiting from cargo diversion from congested West Coast ports and sustained automotive and consumer goods supply chain investment in the Southeast.

EUROPE PORT LOGISTICS

| Primary Market | Rotterdam-Maasvlakte, Hamburg, Antwerp | Rotterdam | Europe's largest port by container throughput |

| Policy Driver | EU single market enabling seamless trans-European port logistics | Development | Maasvlakte 2 logistics zone, Antwerp port expansion |

Europe's port-adjacent industrial market is anchored by the Rotterdam-Maasvlakte logistics zone in the Netherlands, where the Port of Rotterdam processes the largest container volumes in Europe and its adjacent Maasvlakte 2 logistics development provides institutional-grade warehouse and distribution space directly connected to terminal quays. Rotterdam's port-adjacent industrial district is one of the most liquid institutional real estate investment markets in Europe, attracting Prologis, Goodman, and Segro as long-term operators. The Port of Antwerp in Belgium, Europe's second-largest container port, anchors a dense industrial and logistics cluster serving Belgian and German manufacturing supply chains. Hamburg's port industrial district serves German export manufacturing in automotive, chemicals, and machinery. The EU's single market framework eliminates inter-country customs delays for most pan-European supply chains, making European port-adjacent industrial assets primarily relevant for extra-EU import and export flows rather than intra-European distribution.

ASIA PACIFIC

| Singapore | Jurong Industrial Estate, world's leading transshipment hub | India Sagarmala | INR 5.5 trillion port-led development programme |

| Japan | Tokyo Bay industrial corridor, Nagoya port cluster | China | Yangtze River Delta port-adjacent logistics, Tianjin, Qingdao |

Asia Pacific is the fastest-growing port-adjacent industrial region, driven by India's Sagarmala programme, Singapore's continuing role as the world's primary transshipment hub, and China's port-adjacent logistics expansion across the Yangtze River Delta and Pearl River Delta. India's Sagarmala programme has committed INR 5.5 trillion to port-led development across 576 projects, including dedicated industrial zones adjacent to major port terminals at JNPT in Mumbai, Chennai, Visakhapatnam, and Paradip, creating the first generation of institutional-grade port-adjacent industrial parks in a country where the sector was previously dominated by informal operators. Singapore's Jurong Industrial Estate, adjacent to the world's second-busiest container port, is one of the most operationally efficient port-adjacent industrial zones globally, with direct port connectivity, bonded logistics zone status, and automated terminal access that enables rapid customs clearance for Asia-Pacific supply chains.