| TROVIEW INTELLIGENCE | Healthcare REIT Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Geography · By Property Type · By Investor Class · By Lease Structure

Welltower Inc. is the world's most valuable healthcare REIT with a market capitalisation of USD 150.23 billion as of June 15 2026 per financecharts.com, having raised its dividend 10.4% in mid-2025 marking its second consecutive double-digit annual dividend increase and its 37th consecutive quarter of dividend growth, generating USD 7.99 billion in revenue for 2024, completing USD 11 billion in net investments in 2025 including over 900 senior living community acquisitions, announcing USD 23 billion in transactions in October 2025, and closing or contracting USD 5.7 billion in deals in 2026 year-to-date including the USD 3.2 billion Amica Senior Lifestyle Canadian transaction while Ventas Inc. with a market capitalisation of approximately USD 41 billion reported Q1 2026 normalised FFO of 94 cents per share up 9% year-on-year with 15% same-store cash NOI growth in its senior housing operating portfolio and USD 4.8 billion in senior housing acquisitions since Q4 2024, and Healthpeak Properties announced the formation of Janus Living REIT in early 2026 for its 34-community senior housing portfolio with USD 675 million of investments already lined up confirming that global healthcare REITs are riding demographic tailwinds that make them the most structurally advantaged real estate asset class in the public markets.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

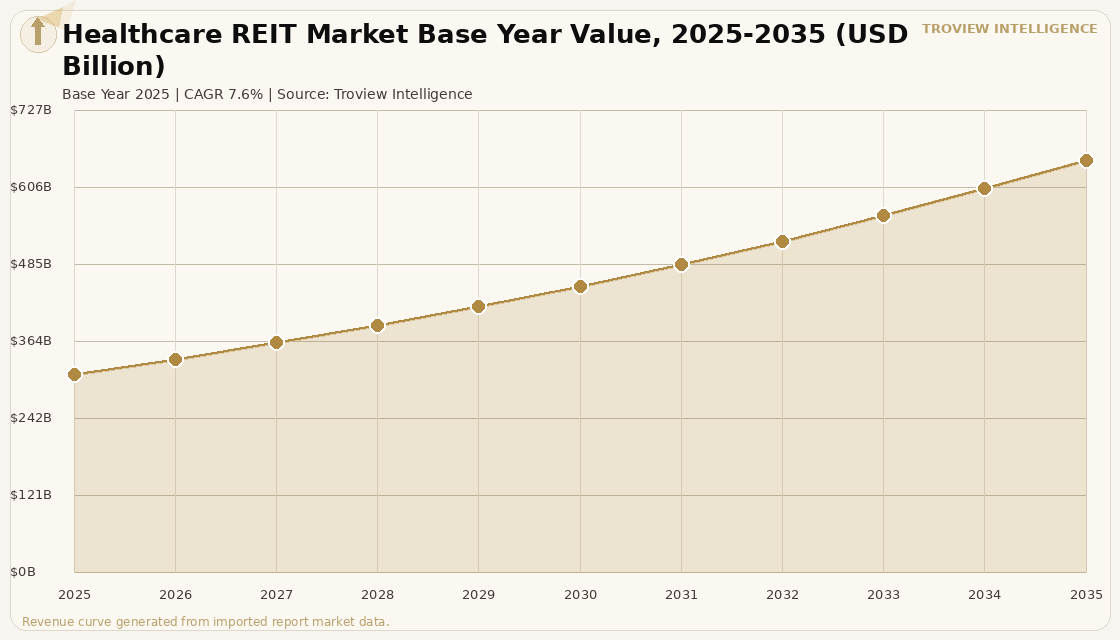

MARKET SYNOPSIS

The global healthcare REIT market size was USD 312.84 Billion in 2025 and is expected to register a revenue CAGR of 7.6% during the forecast period, reaching USD 649.18 Billion by 2035. The 2025 market estimate is grounded in verified company revenues: Welltower Inc. generated USD 7.99 billion in revenue for 2024 and held a market capitalisation of USD 95.77 billion in 2025 per verified financial data, completing USD 11 billion in net investments in 2025; Ventas Inc. reported USD 1.287 billion in operating revenue for 2024, a 10.59% annual increase, with a market capitalisation of approximately USD 27.11 billion in 2025; and the UK healthcare real estate market alone deployed over GBP 12 billion in 2025 per Savills UK Healthcare Roundup 2026, representing the highest annual total on record. The market encompasses publicly listed healthcare real estate investment trusts operating in senior housing, skilled nursing facilities, medical office buildings, hospitals, and life sciences campuses, together with private non-traded healthcare REITs, healthcare-focused infrastructure funds, and direct institutional real estate investors in healthcare property globally. Market revenue growth is anchored in the most durable demand driver in real estate: demographic ageing. The oldest Baby Boomers are turning 80 in 2026, marking what Welltower describes as a pivotal demographic moment driving senior housing demand to record levels, with 1 in 5 seniors over 80 having complex care needs that require dedicated healthcare real estate, and Ontario's 80-plus population alone projected to nearly double by 2040. Welltower announced USD 23 billion in transactions in October 2025, underscoring a clear intent to capitalise on the burgeoning silver economy that is driving unprecedented senior housing demand against constrained supply per Welltower investor communications. For instance, in 2026 year-to-date, Welltower Inc., United States, closed or contracted USD 5.7 billion in deals including the USD 3.2 billion Amica Senior Lifestyle Canadian transaction, the largest single healthcare REIT acquisition in Canada on record, confirming that the world's largest healthcare REIT is accelerating its senior housing portfolio concentration strategy with institutional conviction at a speed that smaller competitors cannot match per Welltower company disclosures. These are some of the key factors driving revenue growth of the market.

Ventas Inc., United States, with a market capitalisation of approximately USD 41 billion and more than 1,400 properties across North America and the United Kingdom, reported Q1 2026 normalised FFO of 94 cents per share, up 9% year-on-year, driven in part by its senior housing operating portfolio that saw 15% same-store cash NOI growth, representing the segment where Ventas has been converting triple-net lease properties to SHOP to capture operational upside per Motley Fool analysis of May 2026. The company has deployed USD 4.8 billion in senior housing acquisitions since Q4 2024 as part of a deliberate acceleration of its senior housing portfolio, with SHOP providing 53% of its NOI by the end of 2025, up from 31% at the end of 2021, demonstrating the sector's structural momentum toward operator-driven returns that compound demographic tailwinds with operational efficiency improvements. Healthpeak Properties, United States, with approximately 700 properties totalling 49 million square feet, announced in early 2026 the formation and planned IPO of Janus Living REIT, contributing its entire 34-community senior housing portfolio and having already lined up USD 675 million of investments for the new entity, with the separation designed to unlock the value of the senior housing portfolio and enable more effective pursuit of expansion per Motley Fool analysis of March 2026. The UK healthcare real estate market recorded its strongest year on record in 2025 with over GBP 12 billion deployed, driven by US REITs including Welltower, CareTrust REIT, and Ventas deploying capital at unprecedented scale across UK care homes and medical properties per Savills UK Healthcare Roundup 2026 and Investors in Healthcare March 2026. These are some of the key factors driving revenue growth of the market.

However, the global healthcare REIT market faces structural constraints that temper the pace of return growth across the forecast period. Interest rate sensitivity remains the primary near-term risk for healthcare REIT valuations, as REITs that rely on debt capital for acquisitions face higher financing costs in the sustained higher-interest-rate environment of 2024 to 2026 relative to the near-zero interest rate environment that defined healthcare REIT underwriting assumptions from 2012 to 2022, compressing the spread between capitalisation rates and financing costs that determines the accretiveness of new acquisitions. Life sciences and medical office building segments of healthcare REITs face specific headwinds, with Nareit's 2025 healthcare REIT outlook noting that NIH funding cuts, FDA headcount reductions, and tariffs have materially impacted the ability of REITs to underwrite new deals in life science, reducing transaction velocity in the segment that was the fastest-growing healthcare REIT sub-category from 2019 to 2022. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect healthcare REIT operations through their impact on energy costs for the 24-hour care environments of senior housing, skilled nursing, and hospital properties that require continuous HVAC, medical-grade electrical systems, and temperature-controlled environments generating above-average energy consumption relative to conventional commercial real estate. These factors substantially limit global healthcare REIT market growth over the forecast period.

Welltower's market capitalisation went from USD 30 billion to USD 150 billion in five years. That is not a valuation re-rating. That is a structural repositioning of how institutional capital prices the intersection of demographic inevitability and operational leverage in senior housing. The oldest Baby Boomers turn 80 in 2026. One in five people over 80 needs complex care that requires dedicated healthcare real estate. The supply of purpose-built senior housing has been constrained since 2020. The demand wave has not started yet it is beginning. Welltower's USD 23 billion in transactions in October 2025 and its USD 5.7 billion in 2026 year-to-date deals are not speculative positioning for a cycle that might arrive. They are the execution of a strategy built on a demographic fact that is as close to certainty as macroeconomics gets. Every healthcare REIT that understood this before 2020 has delivered extraordinary shareholder returns. Every one that understood it in 2022 has still generated above-market returns. The ones that understand it now and can access equity capital at Welltower's cost of capital will be the next decade's outperformers." Troview Intelligence Head of Global Healthcare REIT Research

SEGMENT INSIGHTS

Four Regions Defining Global Healthcare REIT Investment

| Welltower Market Cap Jun 2026 | Welltower Q4 2025 SHOP NOI | Welltower 2025 Net Investments | Ventas Q1 2026 FFO/share |

| USD 150.23 Billion (financecharts.com) | +20.4% YoY (13th consecutive quarter above 20%) | USD 11 Billion (900+ senior communities) | 94 cents, +9% YoY; SHOP NOI +15% |

North America is the world's largest and most institutionally mature healthcare REIT market, anchored by Welltower's unprecedented market capitalisation growth from approximately USD 30 billion to USD 150.23 billion in five years driven by the systematic acquisition of senior living communities at scale, supported by the Welltower Business System data science platform that has generated 13 consecutive quarters of same-store SHOP NOI growth above 20%. Welltower received credit rating upgrades to A- from S&P and A3 from Moody's in March 2025, validating its financial position, and completed USD 11 billion in net investments in 2025 focused on acquiring over 900 senior living communities, with momentum continuing into 2026 through USD 5.7 billion in deals including the USD 3.2 billion Amica Senior Lifestyle Canadian transaction. The oldest Baby Boomers turning 80 in 2026 is accelerating the senior housing demand that Welltower's portfolio is positioned to capture, with the company's 89.5% occupancy rate in Q4 2025 up 400 basis points year-on-year demonstrating that existing portfolio is absorbing demand growth at above-stabilised levels. Ventas's USD 4.8 billion senior housing acquisitions since Q4 2024 confirm that North American healthcare REIT capital deployment is accelerating, not decelerating, as the demographic wave arrives.

| UK Healthcare RE Investment 2025 | PHP-Assura Portfolio | US Operators in London | Welltower UK Activity |

| GBP 12 Billion record (Savills) | GBP 6B, 1,200+ UK/Ireland assets post-merger | ~50% of independent hospital supply (IIH Mar 2026) | GBP 5.2B Barchester care home acquisition |

Europe's healthcare REIT and institutional healthcare real estate investment market recorded GBP 12 billion in UK healthcare property transactions in 2025, the highest annual total on record and approximately four times the five-year prior average per Savills UK Healthcare Roundup 2026, establishing the UK as the primary destination for cross-border healthcare REIT capital in the global market. Primary Health Properties' GBP 1.79 billion acquisition of Assura completed in August 2025, creating a combined primary care REIT with more than 1,200 UK and Ireland primary care assets, a portfolio of approximately GBP 6 billion, and projected cost synergies of at least GBP 9 million, positioned to deliver the investment required by the NHS 10-Year Plan per PHP and Edison Group analysis. US REIT capital has systematically targeted UK healthcare real estate at discounts to net asset value, with Welltower deploying GBP 5.2 billion in its Barchester care home acquisition, CareTrust REIT acquiring CareREIT at a premium to net asset value, and KKR and Stonepeak previously bidding for Assura before the PHP merger prevailed, confirming institutional confidence in UK healthcare REIT fundamentals across the senior housing, primary care, and private hospital segments.

| Parkway Life REIT Portfolio | Parkway 9M 2025 Distributable Income | First REIT | APAC REIT Driver |

| SGD 2.57 Billion, 75 properties | SGD 75.4M (+10.4% YoY) | SGD 1.12 Billion, 32 properties | Ageing population, private healthcare demand growth |

Asia Pacific's healthcare REIT market is anchored by Singapore's Parkway Life REIT and First REIT, with the Australian market attracting record Welltower capital investment through the GBP 5.2 billion Barchester transaction that included Australian care home assets. Parkway Life REIT, one of Asia's largest healthcare REITs, reported 9M 2025 gross revenue of SGD 117.3 million, up 8.2% year-on-year, with distributable income of SGD 75.4 million up 10.4% year-on-year, maintaining 17 consecutive years of DPU growth since its 2007 IPO, with gearing at 35.8% and interest coverage ratio of 8.9x confirming balance sheet strength for continued acquisition per Growbeansprout analysis of November 2025. Japan's healthcare real estate investment market is emerging as a growth opportunity, with Parkway Life REIT's 60 nursing homes and care facilities in Japan generating a significant and growing share of its total portfolio income, and with Japanese institutional real estate investment reaching a quarterly record of JPY 2.092 trillion in Q3 2025 per CBRE Japan Investment MarketView, creating the capital market depth that will support the formalisation of Japan's healthcare REIT sector.