By Destination - By Property Type - By Source Market - By Booking Channel

Destination Spotlights: Bangkok - Phuket - Chiang Mai

Thailand hosted 1,582 hostels across 276 cities in 2025 per Hostelz comparison data, recorded 32.97 million foreign tourist arrivals in 2025 per TAT with long-haul arrivals from Europe, the UK, US, and Australia reaching a record 10.8 million a 10.6% year-on-year increase Phuket recorded H1 2025 hotel occupancy of 79.5% with ADR up 7.8% to THB 5,652 per Knight Frank Thailand while dorm bed rates in Phuket run USD 10 to USD 20 per night versus USD 8 to USD 14 in Bangkok, and Bangkok welcomed approximately 32.4 million international visitors in 2024 making it the world's most-visited city by international arrivals.

MARKET SYNOPSIS

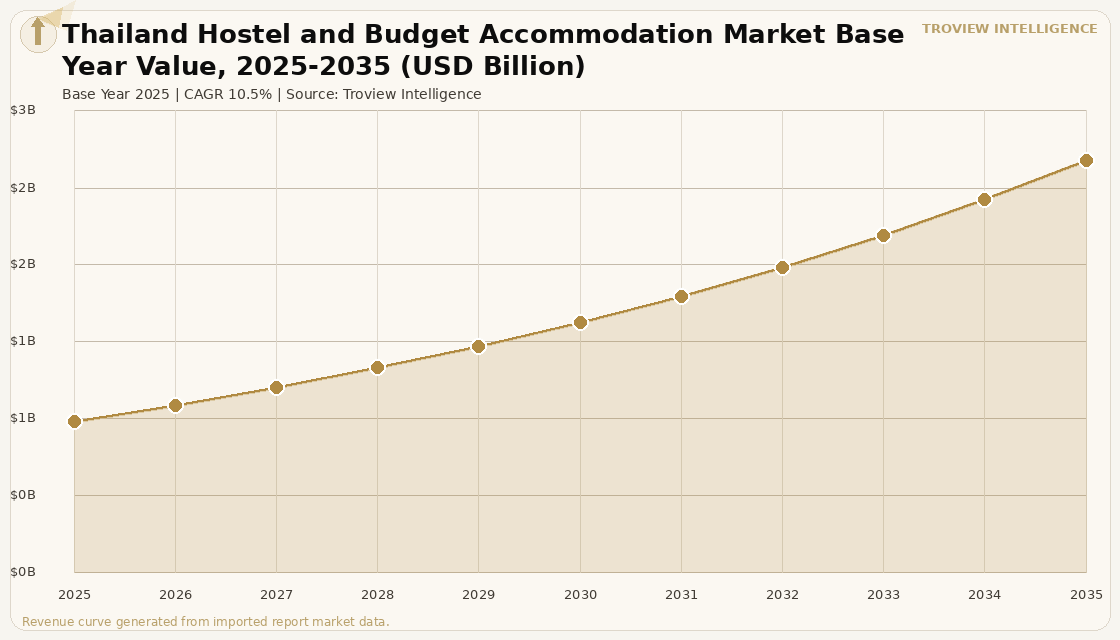

The Thailand hostel and budget accommodation market size was USD 0.84 Billion in 2025 and is expected to register a revenue CAGR of 10.5% during the forecast period, reaching USD 2.28 Billion by 2035. Thailand is Southeast Asia's largest and most established hostel and budget accommodation destination, hosting 1,582 hostel properties across 276 cities per Hostelz comparison data among the highest national hostel density counts globally for a country of Thailand's geographic scale with Bangkok, Phuket, Chiang Mai, Pai, Krabi, and Koh Phangan collectively constituting one of the world's most traversed backpacker circuits. Thailand recorded 32.97 million foreign tourist arrivals in 2025 generating 1.53 trillion baht in visitor spending per TAT and SKHAI verified data with long-haul arrivals from Europe, the United Kingdom, the United States, and Australia reaching an all-time record of 10.8 million in 2025 representing a 10.6% year-on-year increase, and with India emerging as Thailand's third-largest source market at 2.49 million visitors driving growing demand for the sub-USD 30 per night budget accommodation segment that hostels and guesthouses serve. Dormitory bed rates across Thailand's major backpacker hubs range from USD 6 to USD 15 per night in Bangkok and Chiang Mai to USD 10 to USD 20 in Phuket and coastal resort destinations where island logistics costs and higher underlying land values support premium budget pricing per verified travel cost research. For instance, in 2025, Mad Monkey Hostels, Australia, continued expanding its Thailand portfolio with properties in Bangkok, Phuket, Chiang Mai, and Koh Phi Phi, applying its social-programming and community-events model developed in Australia to the Southeast Asian backpacker market and achieving occupancy rates above 80% at peak season across its Thailand network by differentiating through organised tours, bar events, and activity bookings that drive F&B and ancillary revenue alongside bed night income. These are some of the key factors driving revenue growth of the market.

Thailand's hostel and budget accommodation market in 2025 is navigating a period of demand composition shift following the sharp decline in Chinese tourist arrivals down approximately 35% year-on-year in H1 2025 per Knight Frank Thailand reporting, as Chinese outbound travel redirected toward Vietnam, Japan, and domestic alternatives which has disproportionately affected Bangkok's midscale and group-tour-focused hotels and hostels while Phuket's European and long-haul market dependence has provided relative insulation from the Chinese demand decline. Thailand's Tourism Authority has responded by targeting a value-over-volume strategy for 2026 with goals of 39 to 40 million arrivals and 3.4 trillion baht in total tourism revenue, with TAT's stated strategy emphasising travellers who stay 14 to 21 days and spend 65,000 to 80,000 baht per trip a guest profile that aligns more closely with the Western long-stay backpacker than the Chinese group tour visitor. The Thailand Digital Arrival Card launched in July 2024 and attracting over 35,000 Destination Thailand Visa applications in its first year has created digital infrastructure for a new category of long-stay budget traveller the remote worker and digital nomad who generates sustained hostel and budget accommodation demand at above-backpacker daily spend levels.

However, the Thailand hostel and budget accommodation market faces structural constraints that moderate sustainable growth. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating rising long-haul airfare costs from fuel surcharges that increase the all-in cost of Southeast Asia backpacking trips from European and North American source markets, with budget travellers whose price sensitivity to transport costs is materially higher than luxury or business travellers making circuit-routing adjustments when Phuket and Bangkok airfare costs increase by USD 50 to USD 150 per person per direction. Phuket's hostel and budget accommodation prices are already 25 to 50% above mainland Thailand rates for comparable accommodation quality, a cost premium created by island logistics for imported goods, land scarcity on the island's west coast, and peak-season demand surges that push December to February hostel occupancy to 80 to 95% and compress remaining inventory at premium pricing per verified hospitality and travel cost data. Bangkok's oversupply challenge with 3,283 new hotel keys expected in H2 2025 alone and total 2025 new supply exceeding 5,100 keys representing the fastest annual supply growth since the pandemic per Knight Frank Thailand is creating downward rate pressure across midscale and budget accommodation that reduces absolute revenue per available bed for hostel operators competing with new budget hotel inventory. These factors substantially limit Thailand hostel and budget accommodation market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "Thailand's hostel market in 2025 has a structural advantage that most backpacker destinations cannot match: it has been a world-class backpacking destination for 30 years, and every generation of long-haul budget travellers arrives with Thailand already on their itinerary. That built-in demand gravity the Khao San Road to Phuket to Chiang Mai circuit means Thailand's hostel operators have baseline occupancy in peak season that their competitors in Vietnam and Cambodia are still building. The challenge in 2025 is the composition shift. The Chinese group tourist who booked blocks of rooms at midscale and budget hotels is not coming back at 2019 volumes. The Western long-haul backpacker who stays 14 to 21 days, books hostels, and spends broadly across F&B and activities is at an all-time high in 2025. That is a net positive for Thailand's hostel sector the Western backpacker spends differently and writes the social media content that recruits the next generation of visitors. Phuket is the clearest beneficiary. Bangkok's rate discipline problem is a supply story, not a demand story. Too many new hotel keys chasing a market that lost its largest source market in a single year." Troview Intelligence Head of Thailand Hostel and Budget Accommodation Research

SEGMENT INSIGHTS

Three Destinations Shaping Thailand's Budget Accommodation Market

| Int'l Visitors 2024 | H1 2025 Hotel Occupancy | H1 2025 ADR | 2025 New Supply |

| ~32.4 million (world's most visited) | 75.1% (-3.7pp YoY) | THB 4,260 (modest growth) | 5,100+ new keys fastest since pandemic |

Bangkok is Thailand's largest hostel and budget accommodation market, anchored by the Khao San Road backpacker corridor which has been the defining hub of Southeast Asian backpacker travel since the 1980s and hosts hundreds of budget guesthouses, hostels, and travel agencies serving millions of annual budget travellers. Bangkok welcomed approximately 32.4 million international visitors in 2024 making it the world's most-visited city by international arrivals per verified data with hotel occupancy averaging 79% in 2024 and peaking at 84% in February and December. However, H1 2025 Bangkok hotel occupancy fell 3.7 percentage points to 75.1% with only modest ADR growth to THB 4,260 per Knight Frank Thailand, driven by the sharp decline in Chinese tourist arrivals down approximately 35% year-on-year in H1 2025 which disproportionately affected Bangkok's midscale and group-tour-focused accommodation, including many hostels and budget hotels that had oriented their room configuration and marketing toward Chinese group bookings. Bangkok faces an additional challenge from 3,283 new hotel keys launching in H2 2025 and over 5,100 total new keys in 2025 the fastest supply growth since the pandemic creating a buyer's market for accommodation that suppresses rate discipline across the budget segment. Hostel operators who differentiate through social programming, tour packaging, and F&B integration are sustaining occupancy above market average by capturing Western long-haul backpackers whose demand has grown to offset Chinese volume declines.

Phuket STRONGEST H1 2025 PERFORMANCE, 79.5% OCCUPANCY, ADR +7.8%

| H1 2025 Occupancy | H1 2025 ADR | Jan 2025 Peak Occupancy | Hostel Dorm Rate Premium |

| 79.5% (+vs Bangkok 75.1%) | THB 5,652 (+7.8% YoY) | 91.8% (above pre-pandemic) | USD 10-20/night (vs USD 8-14 Bangkok) |

Phuket delivered the strongest H1 2025 hotel market performance of any major Thailand destination, recording 79.5% occupancy and ADR of THB 5,652 a 7.8% year-on-year increase with January 2025 occupancy reaching 91.8%, exceeding pre-pandemic performance levels per GuestMetrix Thailand hospitality analysis citing Knight Frank data. Phuket's hostel and budget accommodation sector benefits from the island's structural demand characteristics a global beach and nightlife destination with direct flights from 64 countries, 19.7 million airport passengers in 2024 per Phuket airport authority data, and European leisure demand from Russia (1.9M arrivals nationwide in 2025), the United Kingdom (850,000 arrivals), and Germany generating year-round occupancy in the island's backpacker zones of Patong, Kata, and Karon. Dormitory bed rates in Phuket's hostel market range from USD 10 to USD 20 per night compared to USD 8 to USD 14 in Bangkok, reflecting the island logistics premium that makes all accommodation more expensive on Phuket and creating a revenue per available bed structure that supports better hostel operating margins despite the elevated cost base. Price increases of 10 to 25% were observed across budget and mid-range Phuket accommodation in advance of the 2025 holiday season per The Asian Affairs reporting, with travel agencies confirming Christmas and New Year reservations almost exhausted months in advance.

| Annual Visitors (2024) | Digital Nomad Profile | Hostel Dorm Rate | Key Advantage |

| ~11.2 million (intl + domestic) | Remote workers, Nimman coworking cluster | USD 7-12/night (lowest major city) | Lower costs + culture year-round demand |

Chiang Mai is Thailand's cultural tourism anchor and emerging digital nomad capital, hosting approximately 11.2 million international and domestic visitors in 2024 and providing the lowest major-city hostel bed rates in Thailand at USD 7 to USD 12 per dormitory night consistently cited as better value than Bangkok or Phuket for comparable quality by verified travel cost research. The city's Nimman neighbourhood has developed one of Southeast Asia's most concentrated coworking and cafe-with-Wi-Fi ecosystems, making Chiang Mai the default long-stay destination for digital nomads and remote workers who seek cultural richness, excellent street food, motorbike accessibility to national park day trips, and co-living infrastructure at costs 40 to 60% below Bangkok equivalents. Chiang Mai's hostel market benefits from year-round demand the November to February cool season generates European and North American backpacker peak demand, while the April Songkran festival drives regional Asian tourism, and the monsoon season from June to October attracts budget travellers who prefer the lower prices and lighter crowds that characterise the wet season destination. The cultural circuit connecting Chiang Mai to Pai, Mae Hong Son, and Chiang Rai generates multi-night budget accommodation stays across northern Thailand's independent hostel network.