| TROVIEW INTELLIGENCE | India Smart Building Technology Market | Q2 2026 |

| TROVIEW INTELLIGENCE · COUNTRY INTELLIGENCE REPORT |

By Component · By Application · By End Use · By Region

Region Profiles: South India (Bengaluru, Chennai, Hyderabad) · West India · North India · East India

India's Smart Cities Mission has completed more than 90% of over 8,000 multi-sectoral projects representing INR 1.6 lakh crore (approximately USD 19.2 billion) in total investment with Integrated Command and Control Centres using AI and IoT operational in all 100 smart cities as of January 2025 per Prop News Time reporting, the Cabinet Committee on Economic Affairs approved 12 new industrial smart city projects under the National Industrial Corridor Development Programme with an investment of INR 286.02 billion (USD 3.41 billion) expected to attract INR 1.52 trillion (USD 18.12 billion) from large industries and MSMEs on August 28 2024, Schneider Electric India delivered double-digit growth in non-residential buildings and data centre end markets in 2024 per Schneider Electric's FY2024 full-year results, Siemens Smart Infrastructure identified India as a stronghold market with a localized growth strategy per its December 2024 Capital Market Event, the Indian Green Building Council has registered more than 12 billion square feet of green buildings with over 14,500 certified projects and the IGBC Bengaluru Chapter has set a target to certify 10 billion square feet over the next decade per Business Standard October 2024 reporting, Johnson Controls showcased energy-efficient cooling and digital building management solutions at ACREX India 2025 targeting India's growing data centre, industrial, and commercial sectors, the Indian Green Building Council released new guidelines for Smart Net-Zero Energy Buildings in January 2025 emphasizing integrated IoT platforms and advanced BMS, and AI-enabled energy solutions are cutting power consumption in Indian commercial buildings by 20% to 30% with the IGBC estimating that smart automation enhances overall building efficiency by 40% confirming India as one of the world's highest-velocity smart building technology adoption markets.

| Standard License: USD 6,500 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

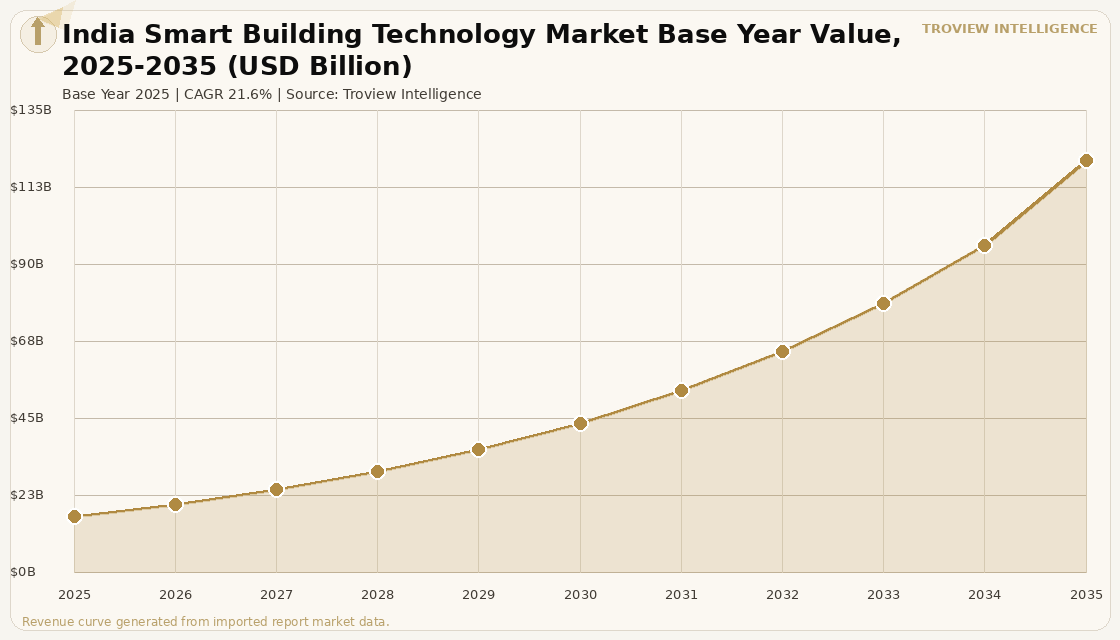

The India smart building technology market size was USD 16.48 Billion in 2025 and is expected to register a revenue CAGR of 21.6% during the forecast period, reaching USD 120.62 Billion by 2035. The 2025 market estimate is grounded in verified government programme data and company financial disclosures: India's Smart Cities Mission has completed more than 90% of over 8,000 multi-sectoral projects representing INR 1.6 lakh crore (approximately USD 19.2 billion) in total investment, with the government allocating INR 48,000 crore of which INR 46,787 crore has been disbursed and over 90% of funds utilised, and Integrated Command and Control Centres established in all 100 smart cities using AI, IoT, and data analytics per Prop News Time January 2025 reporting; the Cabinet Committee on Economic Affairs approved 12 new industrial smart city projects under the National Industrial Corridor Development Programme with INR 286.02 billion (USD 3.41 billion) in direct government investment expected to attract INR 1.52 trillion (USD 18.12 billion) in private investment per India Briefing August 29 2024; and the Indian Green Building Council registered more than 12 billion square feet of green buildings with over 14,500 certified projects per IGBC data and Business Standard October 2024 reporting. Market revenue growth is anchored in the structural convergence of India's government-driven smart city programme which has established the ICCC infrastructure backbone in 100 cities that serves as the anchor demand for smart building technology platforms and IoT sensor networks with the commercial real estate sector's accelerating adoption of energy management, BMS, and AI-powered building automation driven by Schneider Electric's India double-digit growth in non-residential buildings per FY2024 results, Johnson Controls' ACREX India 2025 focus on energy-efficient cooling and digital BMS for commercial, healthcare, and data centre clients, and Siemens Smart Infrastructure's strategic identification of India as a stronghold market with C&S Electric integration and Building X deployment. The IGBC estimates that AI-enabled energy solutions cut power consumption in Indian commercial buildings by 20% to 30%, while smart automation enhances overall building efficiency by 40% creating verifiable operating cost reduction outcomes that compress the payback period on BMS investment in India's elevated energy cost commercial building environment. For instance, in March 2024, Mahindra Lifespace Developers Ltd., India, launched Bengaluru's first Net Zero Waste and Energy residential project Mahindra Zen with over 200 homes across 4.25 acres holding IGBC pre-certified Platinum rating, following the success of Mahindra Eden as India's first Net Zero Energy development, per India building automation market analysis, confirming that Indian residential developers are committing to IGBC-certified net-zero smart building standards as a mainstream product differentiation strategy rather than a compliance-only measure. These are some of the key factors driving revenue growth of the market.

The commercial real estate sector in India has received over USD 400 million in investments from 2020 to 2023 per ResearchAndMarkets analysis of the India BMS market, alongside the addition of 12,000 new hotel rooms in 2023 projected to grow by 3.3% annually, while foreign direct investment amounting to USD 22.07 billion in service and technology sectors has accelerated the demand for effective BMS solutions in the IT parks, corporate campuses, and technology centres that constitute the primary commercial real estate stock where global technology companies are deploying India operations. India is targeting a 25% contribution to GDP from the manufacturing sector alongside the establishment of approximately 1 million direct jobs from the NICDP smart city programme, creating the industrial facility construction pipeline that will require advanced BMS platforms with validated energy management and multi-system integration capability in the new industrial corridors being developed across Gujarat, Rajasthan, Maharashtra, Karnataka, and Andhra Pradesh per CCEA August 2024 approval. The Indian Green Building Council's goal to achieve 10 billion square feet of certified green buildings in the next 10 years confirmed by IGBC Bengaluru Chapter Chairman Chandrashekar Hariharan at the CII-IGBC media event in October 2024 represents the institutional commitment to a certification pace that implies the systematic deployment of IoT platforms, advanced BMS, and smart energy management systems across every certified green building developed in India through 2035. These are some of the key factors driving revenue growth of the market.

However, the India smart building technology market faces structural constraints that limit the pace of adoption through the forecast period. The high initial cost of implementing comprehensive BMS and smart building infrastructure which ranges from USD 2.50 to USD 7.00 per square foot for international-standard systems creates a significant financial barrier for India's large volume of small-to-medium developers and building owners whose total project economics cannot support the capital expenditure that full-featured smart building technology deployment requires, with over 35% of medium-sized building developers in developing nations having delayed smart upgrades due to financial constraints as of 2024. The availability of skilled professionals capable of designing, installing, commissioning, and maintaining increasingly sophisticated smart building platforms is a structural constraint in India, with the smart building technology sector requiring a combination of building engineering, IT network management, AI and data analytics, and cybersecurity expertise that the current Indian educational and training infrastructure is not producing at the rates required by the market's accelerating deployment pace. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect India's smart building technology market through the energy cost transmission that makes the electricity operating costs of India's commercial buildings which are connected to gas-linked power grids in several states volatile, simultaneously creating urgency for energy management system deployment and constraining the capital budgets of building owners facing elevated energy costs. These factors substantially limit India smart building technology market growth over the forecast period.

India's smart building market has an institutional anchor that most countries do not have: 100 cities with government-funded, operationally proven ICCCs that have been running AI and IoT building and city management platforms for years under the Smart Cities Mission. That is not a pilot. That is a production-scale national deployment of integrated command and control infrastructure that creates the reference architecture, the vendor ecosystem, the trained operator base, and the government familiarity with smart building platforms that commercial building developers can point to when justifying their own BMS investment decisions. The private sector acceleration follows the public sector proof-of-concept. Schneider Electric delivering double-digit growth in Indian non-residential buildings, Johnson Controls presenting at ACREX India 2025 on data centre and commercial building solutions, Siemens identifying India as a stronghold market these are commercial consequences of the government having already created the ecosystem. The IGBC target of 10 billion square feet in 10 years is the demand pipeline that these companies are positioning to supply. The question is not whether the market grows. The question is whether the skills base and the BMS installation supply chain can scale fast enough to deploy at the rate the policy and commercial demand requires." Troview Intelligence Head of India Smart Building Technology Research

SEGMENT INSIGHTS

| IGBC Bengaluru Chapter Target | Mahindra Zen Launch | Key Smart Building Clusters | Green Building Congress 2024 |

| 10 Billion sqft green buildings in 10 years | Bengaluru first Net Zero Waste + Energy project Mar 2024 | Electronic City, Whitefield, Manyata Tech Park, RMZ Eco World | Hosted in Bengaluru, November 14-16 2024 |

South India's smart building technology market is the most commercially developed in India, anchored by Bengaluru's extraordinary concentration of IT parks and commercial office campuses where global technology companies including Infosys, Wipro, TCS, and the major international tech multinationals have deployed advanced BMS and energy management systems across campuses that total tens of millions of square feet of premium commercial real estate. The IGBC Bengaluru Chapter's goal of achieving certification for 10 billion square feet over the next ten years confirmed by Chapter Chairman Chandrashekar Hariharan at the October 2024 CII-IGBC media event per Business Standard reporting represents an institutional commitment that drives systematic smart building technology demand across the Bengaluru commercial real estate development pipeline. Mahindra Lifespace Developers launched Bengaluru's first Net Zero Waste and Energy residential project in March 2024, reflecting the extension of smart building energy management standards from the IT park commercial sector into the premium residential market that is increasingly demanding IoT-enabled home automation, smart energy monitoring, and IGBC platinum certification as standard features.

| Pune Smart Building Initiative | Gujarat NICDP Smart City | Mumbai RERA Compliance | West India IGBC Participation |

| Real-time air quality monitoring + predictive maintenance (2024) | Part of 12 NICDP projects approved USD 3.41B Aug 2024 | Driving BMS adoption in premium residential projects | Major contributors to 12B sqft registered footprint |

West India's smart building technology market is anchored by Mumbai's premium commercial real estate market where Grade A office towers and mixed-use developments in Bandra-Kurla Complex, Lower Parel, and Nariman Point deploy international-standard BMS platforms for the financial services and corporate headquarter tenants who specify smart building capability as a lease condition and Pune's expanding commercial and manufacturing sector where the municipal corporation's 2024 expansion of smart building initiatives to include real-time air quality monitoring and predictive maintenance represents a city administration actively supporting smart building technology adoption across public and private sector buildings. Gujarat's industrial corridors, which include smart city projects under both the DMIC and NICDP programmes, are developing greenfield industrial smart building infrastructure at scale, with the Gujarat government's 25% subsidy on total fixed capital investment for IGBC-certified buildings directly subsidising the smart building technology investment in the state's growing industrial facility stock.

| Delhi NCR Commercial Real Estate | Smart Cities ICCC | DMIC Industrial Corridor | Government Buildings |

| Major BMS and energy management adoption Gurugram, Noida | Delhi, Jaipur, Chandigarh AI and IoT platforms operational | Smart building infrastructure in new industrial townships | BMS retrofit programme for central government office estate |

North India's smart building technology market is growing at the fastest rate among India's major regional markets, driven by the Delhi NCR commercial real estate boom in Gurugram and Noida where Grade A office towers and data centre facilities are specifying advanced BMS from the design stage, the Smart Cities Mission ICCCs operational in Delhi, Jaipur, Chandigarh, and other North India cities that are generating sustained demand for smart building technology platforms and IoT sensor networks in government and civic buildings, and the DMIC industrial corridor development that is creating new smart industrial townships in Rajasthan, Haryana, and Uttar Pradesh where plug-and-play smart building infrastructure is being specified as a standard feature per Finance Minister Nirmala Sitharaman's July 2024 Budget announcement of industrial parks near 100 cities under NICDP.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from company press releases, IGBC, Ministry of Housing and Urban Affairs, India Cabinet Committee on Economic Affairs, ACREX India 2025, and verified trade press.