| TROVIEW INTELLIGENCE | Sydney Real Estate Tokenization and Digital Assets Market | Q2 2026 |

| TROVIEW INTELLIGENCE · CITY INTELLIGENCE REPORT |

By Property Segment · By Platform Type · By District Zone · By Investor Type

Segment Profiles: Harbour Waterfront · CBD Commercial · Inner West Residential · Greater Western Sydney · Industrial and Logistics

Sydney is Australia's largest and highest-value property market, with median house prices in premium suburbs exceeding AUD 4 million and the combination of Australia's obsession with real estate and Sydney's position as the country's financial and technological capital creating the most concentrated real estate tokenisation ecosystem in Australia, Propy has integrated with Australian land registries to enable digital title minting in progressive states with New South Wales among the most likely early adopter jurisdictions, ASIC's headquarters in Sydney positions the city as the primary regulatory engagement and compliance hub for Australia's new Digital Assets Framework, BrickX and DomaCom both operate from Sydney with specific named property investments in premium Inner Sydney and Eastern Suburbs residential addresses, the 45% annual growth in Australians investing in RWAs per the 2025 Australian Treasury Digital Asset Survey is disproportionately concentrated in New South Wales where higher property prices create the largest affordability gap that tokenisation solves, Cadena Legal as a NSW-registered legal practice has specifically analysed Sydney commercial property tokenisation scenarios including the example of a commercial building in Sydney tokenised into 10,000 tokens, and several Australian states have introduced Digital Stamp Duty at lower rates for tokenised property trades confirming Sydney as the primary city-level market for Australia's real estate tokenisation ecosystem.

| Standard License: USD 2,200 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

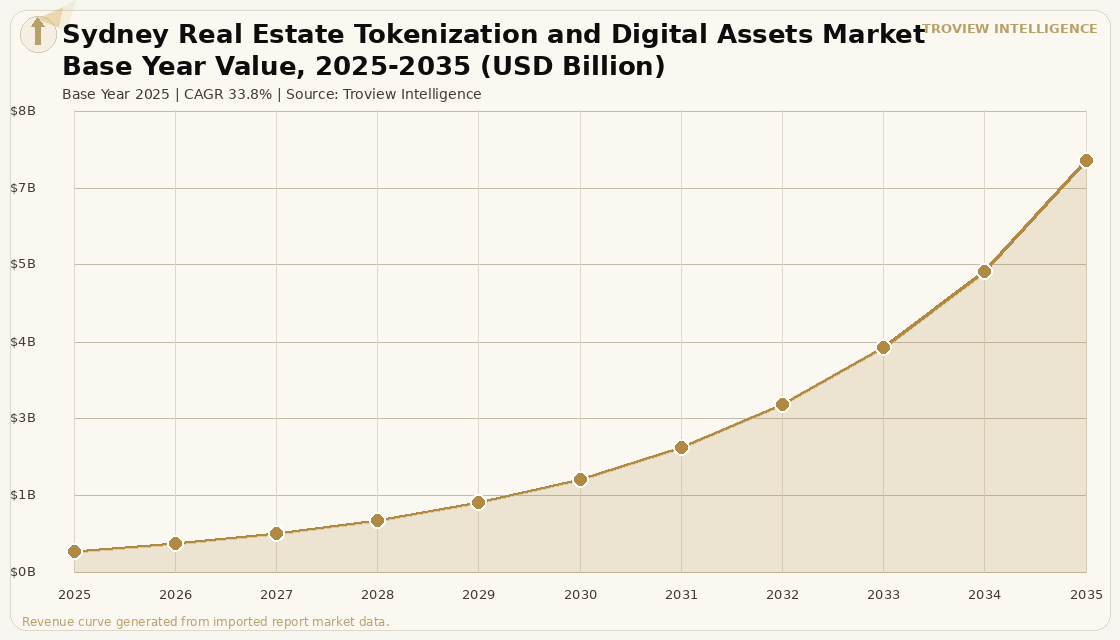

The Sydney real estate tokenization and digital assets market size was USD 384.6 Million in 2025 and is expected to register a revenue CAGR of 33.8% during the forecast period, reaching USD 7.24 Billion by 2035. The market encompasses the total investible and platform-generated revenue from real estate tokenisation, fractional property digital assets, and blockchain-based property transaction infrastructure across Greater Sydney encompassing the 33 Local Government Areas of the Greater Sydney region from the Northern Beaches and Upper North Shore through the Eastern Suburbs, Inner West, and South Sydney to Greater Western Sydney and the Parramatta economic corridor where Australia's highest concentration of premium residential property, CBD commercial real estate, and technology-literate investor population creates the most concentrated real estate tokenisation opportunity in the country. Sydney's real estate tokenisation market derives its scale from the fundamental mismatch between Sydney property values where median house prices in premium suburbs including Mosman, Bronte, and Bellevue Hill regularly exceed AUD 4 million per Australian property data and the capital accessible to Australian retail and younger-cohort investors whose household savings are insufficient for a conventional mortgage deposit in Sydney's most desirable suburbs, creating the exact affordability gap that fractional tokenised real estate products are designed to bridge. Cadena Legal, a NSW-registered legal practice, specifically used the example of a commercial building in Sydney tokenised into 10,000 tokens each representing a 0.01% ownership stake in its analysis of Australian real estate tokenisation frameworks, confirming that Sydney commercial real estate is the most commonly referenced tokenisation scenario in Australian legal and regulatory analysis and that NSW's regulatory environment is being specifically shaped with Sydney property tokenisation use cases in mind. For instance, in 2025, BrickX, Australia, operates specific named Sydney residential properties in its fractional ownership portfolio including properties in Inner West and Eastern Suburbs locations that retail investors can access through brick purchases from as little as a few hundred Australian dollars demonstrating that production-scale fractional tokenised real estate products targeting Sydney property addresses are available to Australian retail investors and are generating the investor adoption metrics that the 2025 Australian Treasury Digital Asset Survey's 45% annual RWA growth figure reflects. These are some of the key factors driving revenue growth of the market.

The Corporations Amendment (Digital Assets Framework) Bill 2025's passage through both Australian houses on April 1 2026, combined with ASIC's October 2025 update to Information Sheet 225 that specifically added tokenised real estate as an example and the establishment of a sector-wide no-action position through June 30 2026, creates the most comprehensive regulatory foundation for Sydney real estate tokenisation in the market's history, with New South Wales expected to be among the first states to implement the land registry adaptations that enable digital title minting after Propy's integration with Australian land registries in progressive states confirmed the technical feasibility of blockchain-based title registration for Australian property. The RealT platform lawsuit in Detroit in July 2025 where the City of Detroit sued RealT claiming property mismanagement and neglect across rental units with massive code violations across vacant and blighted properties per Prophecy Market Insights analysis serves as the cautionary example for the Australian real estate tokenisation market of what governance and operational accountability standards must accompany blockchain-based property ownership to maintain investor protection at the token holder level, with ASIC's licensing requirements, disclosure obligations, and conduct standards specifically designed to prevent the operational governance failures that the RealT Detroit situation illustrated. These are some of the key factors driving revenue growth of the market.

However, the Sydney real estate tokenization and digital assets market faces structural constraints that limit the pace of platform development and investor adoption through the forecast period. New South Wales' property law framework anchored in the Torrens title system administered by NSW Land Registry Services does not currently provide for transfer of property ownership through blockchain-based token transfer without a conventional paper-based or electronic conveyancing instrument, meaning that tokenised ownership of Sydney properties typically operates through an intermediate legal entity structure most commonly a Special Purpose Vehicle or a Managed Investment Scheme that holds the property title while investors own tokens representing beneficial interests in the SPV or MIS, rather than tokens representing direct property title, creating legal complexity that reduces the ease of understanding and trust for retail investors who are accustomed to the simplicity of conventional property purchase. The cost of Sydney real estate as the underlying asset for tokenisation creates per-token economics that differ fundamentally from lower-cost property markets: a Sydney CBD office building valued at AUD 200 million tokenised into 1 million tokens creates a per-token NAV of AUD 200 and a minimum meaningful investment size that is higher than equivalent tokenisation programmes for lower-cost Australian regional or overseas properties, limiting the true fractional accessibility of Sydney commercial real estate tokenisation relative to the USD 50 minimums achievable with lower-cost US residential properties on RealT. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect Sydney real estate tokenisation platform operating costs through their impact on NSW electricity prices generated from natural gas power stations. These factors substantially limit Sydney real estate tokenisation and digital assets market growth over the forecast period.

Sydney is the perfect laboratory for real estate tokenisation because it has two things simultaneously: the world's most culturally engaged property investor population and the world's most extreme residential property affordability gap for that same population. A 25-year-old in Sydney who earns AUD 85,000 per year cannot buy a median-priced house in the suburb where they grew up, cannot save a 20% deposit in less than ten years in a market that is appreciating faster than wages, and cannot get any property exposure without either buying in a distant regional city or compromising their lifestyle completely. But they can buy a BrickX brick in a Bondi or Newtown property for AUD 100 and hold a small stake in the Sydney residential market they understand intuitively. That is not a niche crypto-adjacent product. That is a mainstream financial product responding to the largest structural financial exclusion problem in the most property-obsessed culture in the world. When the Digital Assets Framework Bill AFSL regime creates the regulated platform environment that institutional-grade investors and superannuation funds require, Sydney real estate tokenisation will transition from the retail fractional BrickX model to the full institutional tokenised commercial real estate capital market model that Deloitte projected at USD 4 trillion globally. Sydney will be at the centre of that transition in Australia." Troview Intelligence Head of Sydney Real Estate Tokenization and Digital Assets Research

SEGMENT INSIGHTS

| 03 | PROPERTY SEGMENT ANALYSIS |

Five Sydney Property Segments for Real Estate Tokenisation Investment

HARBOUR WATERFRONT AND PREMIUM RESIDENTIAL (EASTERN SUBURBS) AUD 4M+ MEDIAN, HIGHEST TOKENISATION UNIT VALUE IN AUSTRALIA

| Mosman / Bellevue Hill Median | Tokenisation Appeal | Investor Profile | Challenge |

| AUD 4M+ highest Sydney residential values | Highest per-token NAV prestigious address access | HNW and SMSF investors seeking premium suburb exposure | SPV/MIS structure complexity for title in premium suburbs |

Sydney's harbour waterfront and Eastern Suburbs premium residential market encompassing Mosman, Cremorne, Bellevue Hill, Vaucluse, Point Piper, and the coastal suburbs from Bondi to Coogee represents the highest per-token NAV property segment available in Australian real estate tokenisation, where individual properties valued at AUD 4 million to AUD 10 million tokenised at 0.01% per token create investment unit values of AUD 400 to AUD 1,000 that provide retail investors with denominated exposure to the most prestigious residential addresses in Australia. The cultural cachet of owning a tokenised fraction of a Mosman harbourfront property or a Bellevue Hill estate even at the 0.01% level creates a demand for Sydney premium residential tokenisation that has no parallel in any other Australian property market segment, as the address prestige that premium Sydney residential real estate carries in Australian culture translates into investor demand that goes beyond pure financial return analysis and reflects the cultural significance of property ownership in premium suburbs that represents a social aspiration for many Australian investors. The SPV-based legal structure required for Sydney premium residential tokenisation where the SPV holds the Torrens title while investors hold beneficial interest tokens adds legal complexity relative to conventional property purchase but provides the ASIC-regulated investment vehicle framework that satisfies the compliance obligations of SMSF trustees investing member retirement savings in tokenised residential real estate.

| Primary Tokenization Example | Investor Profile | Post-Digital Assets Bill | Yield Driver |

| Cadena Legal: Sydney CBD building 10,000 tokens (0.01% each) | Wholesale, institutional, SMSF AFSL platform required | AFSL-licensed platform enables institutional allocation | Grade-A office rental distributions + capital appreciation |

The Sydney CBD and North Sydney commercial office market represents the institutional tokenisation opportunity in the Sydney real estate digital assets market, with Cadena Legal specifically using the example of a commercial building in Sydney tokenised into 10,000 tokens each representing a 0.01% ownership stake in its analysis of Australian real estate tokenisation frameworks per Cadena Legal NSW-registered legal practice analysis, confirming that Sydney CBD commercial office is the primary institutional tokenisation use case being actively analysed by Australian legal practitioners advising on the Digital Assets Framework Bill's implementation. The April 2026 passage of the Digital Assets Framework Bill creates the regulated platform environment for AFSL-licensed digital asset platforms to offer Sydney CBD commercial office tokenisation to wholesale and institutional investors including the AUD 900 billion SMSF sector, family offices, and superannuation funds through a licensed market structure that satisfies the compliance obligations of sophisticated Australian institutional capital. Sydney's CBD Grade-A office vacancy recovery confirmed by JLL's Q4 2025 global office market report, combined with the corporate disposal pipeline from Japanese companies selling Australian-held assets and the foreign cross-border investment activity documented in CBRE's Asia Pacific investment data, creates a pipeline of well-located, institutional-quality Sydney office assets that are candidates for tokenisation as part of corporate portfolio restructuring or as new fundraising vehicles for property developers.

| Investment Minimum | Target Suburbs | Property Type | Cultural Appeal |

| AUD 100+ per brick retail accessible | Newtown, Glebe, Marrickville, Leichhardt, Annandale | Named residential properties terrace houses, apartments | Inner West cultural identity strong tenant demand, gentrification |

The Inner West Sydney residential market encompassing Newtown, Glebe, Marrickville, Leichhardt, Annandale, and the adjacent inner suburbs constitutes the primary geographic focus of BrickX's Sydney tokenised residential property portfolio, where the combination of accessible entry prices relative to the Eastern Suburbs and Lower North Shore, strong cultural identity that sustains above-average rental demand from the young professional and creative economy demographic, and the gentrification trajectory that has delivered above-average capital growth in Inner West property over the past two decades creates the investment fundamentals that attract both retail tokenised property investors and the conventional real estate investors that tokenised fractional platforms are seeking to replicate at lower entry points. BrickX's model of allowing retail investors to buy bricks in named Inner West properties at from a few hundred dollars per brick provides the specific, address-level investment identity that generic managed fund units cannot offer, with the tokenised investor knowing they own a fractional stake in a specific terrace house in Newtown or a specific apartment in Glebe rather than an undifferentiated unitised interest in a diversified managed fund portfolio. The Inner West's strong rental market, driven by proximity to the University of Sydney, UNSW, and the CBD employment core, sustains the rental income distributions that make tokenised Inner West residential investment return profiles compelling for investors seeking both rental income and capital growth exposure.

| Property Values | Western Airport Driver | Tokenisation Appeal | Land Tokenisation |

| Lower median more tokens per AUD investment | Aerotropolis employment zone uplift potential | Growth area + affordability = high investor demand | Development site token potential in Airport Precinct |

Greater Western Sydney encompassing Penrith, Parramatta, Blacktown, Liverpool, and the Western Sydney International Airport Aerotropolis precinct represents the highest-growth potential Sydney tokenisation market from a capital appreciation perspective, where the property value uplift driven by the Airport's planned opening and the Aerotropolis employment zone development creates significant near-term development value uplift that tokenised land and development site structures can capture at entry prices well below the AUD 4 million medians of the Eastern Suburbs. The Western Sydney property market's lower absolute property values compared to the Eastern Suburbs and North Shore create more accessible per-token entry points for retail investors a AUD 500,000 Greater Western Sydney property tokenised into 5,000 tokens creates a per-token value of AUD 100 making Greater Western Sydney the most accessible-entry tokenisation market in the Greater Sydney region at current property values. Development site tokenisation in the Aerotropolis precinct where properties within the Western Sydney International Airport employment zone are expected to appreciate significantly as infrastructure construction advances and employers commit to the Aerotropolis represents an emerging tokenisation category that enables retail investors to access the development uplift of Western Sydney's most consequential infrastructure-driven property growth story at fractional investment sizes.

SYDNEY INDUSTRIAL AND LOGISTICS EMERGING TOKENISATION CATEGORY INSTITUTIONAL RWA + RETAIL, OUTER WESTERN SYDNEY LOGISTICS

| Driver | Tokenisation Appeal | Primary Zones | Investor Profile |

| E-commerce growth sustaining Greater Sydney logistics demand | Stable income + transparent warehouse-level ownership | Outer Western Sydney, Eastern Creek, Wetherill Park | SMSF and institutional seeking industrial income exposure |

Sydney industrial and logistics real estate concentrated in the outer Western Sydney logistics corridors including Eastern Creek, Wetherill Park, Moorebank, and the Outer Metropolitan Ring Road industrial precincts represents the emerging institutional tokenisation category in the Sydney market where the combination of strong and predictable rental income from logistics tenants, the transparent cash flow profile of warehouse-and-logistics leases, and the growing investor appetite for industrial real estate exposure creates an attractive asset class for both institutional tokenised real estate fund structures and retail fractional ownership products. The Australian industrial and logistics sector's above-average rent growth trajectory driven by e-commerce fulfilment demand from Amazon, Coles, and the broader Australian retail e-commerce ecosystem creates the income growth profile that institutional tokenised real estate investors using the post-Digital Assets Framework AFSL-licensed platform infrastructure will underwrite in their acquisition models, with the Sydney metro logistics market's rent premiums over secondary Australian logistics markets providing the premium return that justifies digital capital market structuring costs. Several logistics and data-centre portfolios in Australia traded above AUD 100 billion equivalents in the broader real estate transaction market per Tokyo Portfolio data referencing Australia's logistics market, and the Sydney industrial market is expected to attract institutional tokenisation programmes as the AFSL-licensed platform ecosystem matures through 2026 to 2028.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from ASIC official releases, Parliament of Australia records, Cadena Legal analysis, Tokenizer Estate, and verified Australian trade press.