| TROVIEW INTELLIGENCE | Real Estate AI and Analytics Market | Q2 2026 |

By Technology - By Solution - By Deployment - By End-User - By Region

The global AI in real estate market is projected to grow at a CAGR of 30.5% from 2024 to 2033 reaching approximately USD 41.50 Billion by 2033 per McKinsey and Company, AI in real estate is projected to reach USD 3,286.78 Billion by 2032 at a CAGR of 30% per verified market analysis with chatbots holding 28.98% market share in 2025, global proptech market size reached USD 47.08 Billion in 2025 projected to reach USD 209.43 Billion by 2035 at CAGR of 16.10% with North America holding 55.29% share and software segment commanding 68% share per verified market data, CRETI confirmed VC firms invested USD 16.70 Billion in proptech in 2025 at 67.9% year-on-year increase with USD 1.70 Billion in January 2026 alone at 176% year-on-year increase, AI-centered proptech grew at 42% annualized rate in 2025 versus 24% for non-AI per PitchBook, JLL research confirmed 90.1% of real estate firms plan AI investment and 700 of 7,000 global proptech companies are AI-powered with 62% VC-backed, and generative AI could add USD 110 Billion to USD 180 Billion annually to the real estate sector per PwC and ULI Emerging Trends 2025 and 2026.

MARKET SYNOPSIS

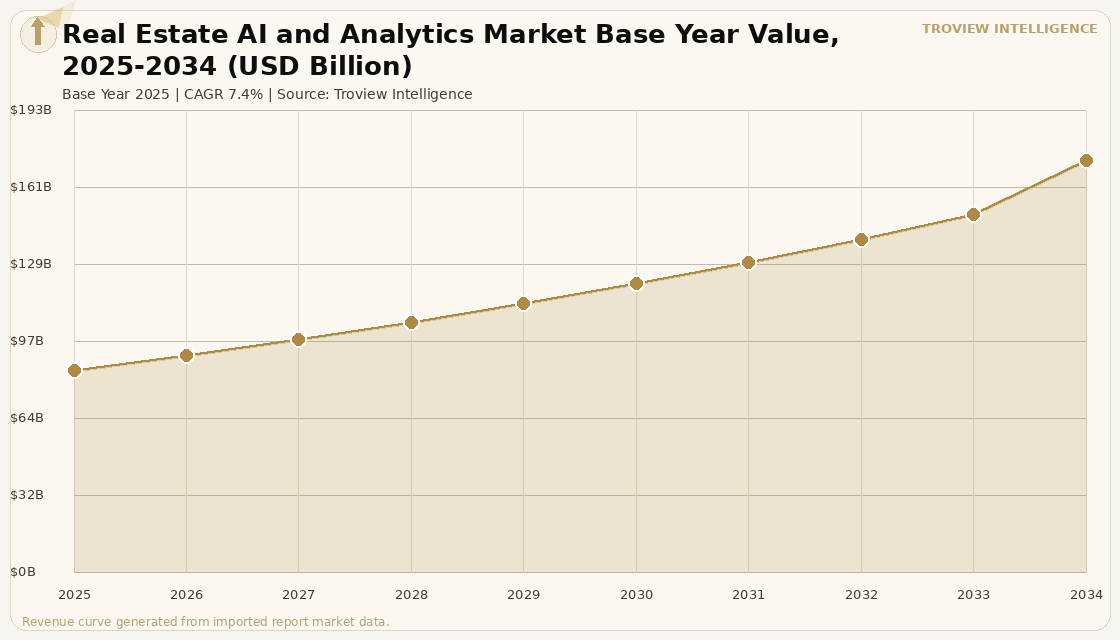

The global real estate AI and analytics market size was USD 84.62 Billion in 2025 and is expected to register a revenue CAGR of 7.4% during the forecast period, reaching USD 172.38 Billion by 2034. The global real estate AI and analytics market encompasses the full spectrum of artificial intelligence, machine learning, predictive analytics, computer vision, natural language processing, and data platform technologies deployed across the real estate value chain spanning property discovery and search, automated valuation and appraisal, investment underwriting and portfolio management, lease abstraction and contract intelligence, building operations and predictive maintenance, tenant communications and property management, construction planning and project monitoring, and sustainability and energy analytics for commercial and residential assets. The global AI in real estate market is projected to grow at a CAGR of 30.5% from 2024 to 2033, reaching approximately USD 41.50 Billion by 2033 per McKinsey and Company verified data cited by CRETI 2025 Emerging Trends research, while The AI in real estate market is projected to reach USD 3,286.78 Billion by 2032 at a CAGR of 30% per verified market analysis, with chatbots holding 28.98% of market share in 2025 as the largest solution segment per verified industry data. The global proptech market the broader market within which real estate AI and analytics operates as the fastest-growing sub-sector reached USD 47.08 Billion in 2025 and is projected to reach USD 209.43 Billion by 2035 at a CAGR of 16.10% per verified global proptech market data, with North America holding 55.29% market share in 2025, the residential segment commanding 53% share, and the software segment contributing 68% of global proptech revenue in 2025. The 2025 market estimate is grounded in verified company and investment data: CRETI confirmed that venture capital firms invested USD 16.70 Billion in proptech in 2025, a 67.9% year-on-year increase from 2024, with USD 1.70 Billion deployed in January 2026 alone representing a 176% year-on-year increase, and AI-centered proptech companies growing at an annualized rate of 42% in 2025 almost double the 24% growth rate of non-AI proptech companies per PitchBook data cited by Bisnow verified reporting. These are some of the key factors driving revenue growth of the market.

The global real estate AI and analytics market is in a phase of accelerating institutionalisation, transitioning from experimentation and pilot deployment toward scaled production adoption across institutional real estate investment, commercial property management, and residential consumer platforms. JLL Research confirmed that 90.1% of real estate firms plan to carry out corporate real estate activities with AI supporting human experts over the next five years, with over 60% already piloting different AI use cases in their real estate functions, and that among 7,000 global proptech companies approximately 700 (10%) are currently providing AI-powered solutions with 62% VC-backed and 83% already generating revenues or making profits per JLL verified research. The most recent CBRE Technology Report 2025 confirmed that 67% of institutional real estate investors now use some form of AI or machine learning in their investment decision process, up from 22% in 2021 per CBRE verified data cited by hourlydeveloper.io. The four major AI-powered proptech unicorns minted since July 2025 confirm the direction of institutional investment concentration: EliseAI founded 2017, valued at USD 2.20 Billion, raised USD 250 Million in August 2025 backed by Andreessen Horowitz and Bessemer Venture Partners provides agentic AI for multifamily landlords managing correspondence, tours, lease audits, and maintenance; Juniper Square founded 2014, valued at USD 1.10 Billion, raised USD 130 Million in June 2025 backed by Ribbit Capital and Fifth Wall launched an AI-powered CRM using natural language processing and predictive modeling in October 2025. US private AI investment reached USD 109 Billion in 2024, doubling the 2023 total, with AI companies in the US nearly doubling their real estate footprint to 2.04 million square metres and expected to reach 5.2 million square metres by 2030 per JLL Research verified data.

However, the global real estate AI and analytics market faces structural constraints that limit the pace of adoption and the depth of technology integration across the full institutional and retail real estate market. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation that directly increases the operating costs of the data centre and cloud computing infrastructure that underpins real estate AI and analytics platforms as data centre energy costs represent a significant and growing proportion of AI platform operating expenses, Hormuz-linked energy price increases compound the already elevated energy cost environment that cloud providers are managing across their global data centre portfolios. The concentration of USD 11.20 Billion of the USD 16.70 Billion in 2025 proptech venture capital into rounds of USD 100 Million or more with 31 companies accounting for 72.3% of total capital invested per CRETI verified data confirms a structurally bifurcated market where a small cohort of scaled AI proptech platforms is attracting the majority of institutional venture capital while the long tail of early-stage AI real estate startups faces significantly tighter funding conditions and valuation pressure. Data privacy concerns, regulatory compliance requirements across multiple jurisdictions, and the skills gap among real estate professionals who must deploy and interpret AI outputs without deep technology backgrounds represent persistent structural constraints to AI adoption in the real estate sector. These factors substantially limit global real estate AI and analytics market growth over the forecast period.

The real estate AI and analytics market in 2025 is no longer about whether AI will transform real estate it already has, for the players who moved first. The data points are unambiguous: 67% of institutional investors now use AI in investment decisions, up from 22% in 2021. JLL's own research shows 90.1% of real estate firms planning AI investment. US private AI investment doubled to USD 109 Billion in 2024. AI companies doubled their real estate footprint to 2.04 million square metres in two years. The transformation is not hypothetical it is being measured in square metres of data centre demand, in CBRE Technology Reports, in JLL research surveys, and in the USD 16.70 Billion of proptech VC deployed in 2025 with 42% annualised growth in AI-specific proptech versus 24% for non-AI. The market structure question for the next five years is not adoption rates those are converging rapidly. The question is which AI proptech companies will build the defensible data loops and enterprise integrations that make switching expensive, because the winners in AI proptech will be determined by data monopoly, not algorithm superiority. EliseAI at USD 2.20 Billion valuation for multifamily AI leasing, Juniper Square at USD 1.10 Billion for investment management AI these valuations reflect the long-term recurring revenue potential of AI platforms embedded into the operational core of large real estate enterprises." Troview Intelligence Head of Global Real Estate AI and Analytics Research

SEGMENT INSIGHTS

By Technology

Machine learning and predictive analytics technology is expected to account for a significantly large revenue share in the global real estate AI and analytics market during the forecast period.

Based on technology, the global real estate AI and analytics market is segmented into machine learning and predictive analytics encompassing property valuation models, investment underwriting algorithms, and market trend forecasting; natural language processing covering lease abstraction, contract intelligence, tenant communication automation, and document processing; computer vision including property condition assessment, virtual staging, construction progress monitoring, and spatial mapping; generative AI for property description generation, marketing content automation, and synthetic data creation; and IoT-integrated building intelligence combining sensor data with AI analytics for energy management, predictive maintenance, and occupancy optimisation. Machine learning and predictive analytics dominates the global real estate AI and analytics market by deployed revenue as the most mature and institutionally validated AI application in real estate, with the CBRE Technology Report 2025 confirming 67% of institutional investors use AI or ML in investment decisions, up from 22% in 2021. Generative AI is expected to register the fastest revenue growth during the forecast period, as PwC and ULI Emerging Trends 2025-2026 confirmed generative AI could add USD 110 Billion to USD 180 Billion annually to the real estate sector, with the McKinsey projection of 30.5% CAGR for AI in real estate through 2033 reflecting the compounding adoption of generative AI across property marketing, lease management, and investment reporting.

By Solution

Automated valuation and property analytics solution is expected to account for a significantly large revenue share in the global real estate AI and analytics market during the forecast period.

Based on solution, the global real estate AI and analytics market is segmented into automated valuation models delivering property price estimation with sub-3% error rates through machine learning algorithms trained on transaction data; AI-powered investment management platforms encompassing underwriting automation, portfolio optimisation, and investor reporting; lease abstraction and contract intelligence using NLP to extract key terms from lease documents at scale; tenant communication and property management AI handling correspondence, maintenance scheduling, and leasing automation; predictive building maintenance and energy analytics using IoT sensor data; property search and discovery platforms using AI personalisation and recommendation; and construction technology and project monitoring platforms. Chatbots as a subset of the AI-powered tenant communication and property management solution segment held 28.98% of global AI in real estate market share in 2025 per verified market data, reflecting the most widespread and tangible AI deployment across real estate enterprises of all sizes. AI investment management platforms are expected to register the fastest revenue growth during the forecast period, driven by the Juniper Square USD 130 Million raise in June 2025 for its AI-powered CRM with NLP and predictive modeling, the expansion of AI underwriting automation among institutional investors, and the 64% of commercial real estate investors planning to increase AI-powered proptech investment per PwC verified data.

By Deployment

Cloud-based deployment is expected to account for a significantly large revenue share in the global real estate AI and analytics market during the forecast period.

Based on deployment, the global real estate AI and analytics market is segmented into cloud-based deployment enabling scalable AI model training and inference with subscription-based pricing accessible to real estate enterprises of all sizes, on-premises deployment for institutional investors and large REITs requiring data sovereignty, security control, and integration with proprietary systems, and hybrid deployment combining cloud AI inference with on-premises data storage and compliance controls. Cloud-based deployment captured 61% of the global proptech market share in 2025 per verified global proptech market data, reflecting the structural alignment between cloud scalability, AI computational requirements, and the subscription revenue model that proptech companies favour for recurring revenue generation and investor valuation metrics. On-premises deployment is expected to register strong growth in the global real estate AI and analytics market over the forecast period as institutional investors with proprietary deal flow data, tenant data, and portfolio performance data require the security architecture and data sovereignty controls that cloud-only deployments cannot provide at the compliance standards demanded by large pension funds and institutional asset managers.

REGIONAL ANALYSIS

NORTH AMERICA

| NA PropTech Market Share (2025) | US Private AI Investment (2024) | EliseAI Valuation (Aug 2025) | Juniper Square Raise (Jun 2025) |

| 55.29% verified proptech market data | USD 109 Billion doubled from 2023 per JLL Research | USD 2.20 Billion Andreessen Horowitz / Bessemer / Sapphire | USD 130 Million Ribbit Capital / Fifth Wall / Redpoint |

North America dominates the global real estate AI and analytics market with a 55.29% proptech market share in 2025 per verified global proptech market data, anchored by the United States' extraordinary AI investment ecosystem that deployed USD 109 Billion in private AI investment in 2024 alone doubling the 2023 total making the US the world's largest single market for AI capital formation with China in second position at USD 9.30 Billion per JLL Research verified data. The United States hosts the world's most mature real estate AI ecosystem, encompassing AI native platforms including EliseAI (USD 2.20 Billion valuation, USD 250 Million raise August 2025, agentic AI for multifamily landlords, backed by Andreessen Horowitz and Bessemer Venture Partners, working with Greystar, AvalonBay, Bozzuto, Brookfield, and Equity Residential), Juniper Square (USD 1.10 Billion valuation, USD 130 Million raise June 2025, AI-powered CRM with NLP and predictive modeling for private investment management, backed by Ribbit Capital, Fifth Wall, and Redpoint Ventures), Fundrise (deployed AI-powered portfolio management for automated rebalancing in 2024), Arrived Homes (integrated AI valuation tools reducing property analysis from weeks to hours), and thousands of early-stage AI proptech companies across the CRETI ecosystem. US AI companies nearly doubled their real estate footprint to 2.04 million square metres in two years and are expected to reach 5.2 million square metres by 2030 per JLL Research, creating significant data centre and office demand that is simultaneously a product of AI growth and an investment theme within the real estate sector.

EUROPE UK USD 3.32BN PROPTECH 2024 GROWING TO USD 25.08BN BY 2035, 845 ACTIVE UK COMPANIES, LONDON 600+

| UK PropTech Market (2024) | UK PropTech Forecast (2035) | UK PropTech CAGR | Active UK PropTech Companies |

| USD 3.32 Billion | USD 25.08 Billion | 20.181% CAGR | 845 active companies 180% growth since 2015 per Beauhurst 2025 |

Europe is the world's second-largest real estate AI and analytics market, with the United Kingdom as the dominant European hub, and London as the European capital for proptech with over 600 active proptech companies ranking second globally after San Francisco for improving real estate longevity per grow.london verified data. The UK proptech market was valued at USD 3.32 Billion in 2024 and is projected to reach USD 25.08 Billion by 2035 at a CAGR of 20.181% per verified UK proptech market data, with 845 active UK proptech companies representing 180% growth over the past decade (2015-2025) per Beauhurst 2025 verified data. UK proptech investment rose from GBP 192.40 Million in 2024 to GBP 230.40 Million in 2025 per Beauhurst verified data, confirming continued investor confidence despite a slowdown in new company formations from 69 in 2018 to 21 in 2025. The 78% of UK real estate professionals using at least one proptech solution per UK PropTech Association 2025 survey, and the 67% of institutional real estate investors using AI or ML in investment decisions per CBRE Technology Report 2025, reflect an industry at advanced AI adoption rates relative to global averages. PwC UK confirmed PropTech startup investment grew 22% year-on-year with over GBP 3.10 Billion invested in 2024 alone, reflecting sustained institutional and venture capital commitment to the UK proptech ecosystem anchored in London's global proptech VC community including Europe's largest proptech VC A/O PropTech and early-stage specialist Pi Labs.

ASIA PACIFIC FASTEST GROWING CAGR

| APAC PropTech CAGR (2026-2035) | China AI Investment (2024) | APAC Global RE Market Share | Key APAC Growth Markets |

| 18.60% fastest among all regions per verified market data | USD 9.30 Billion second globally per JLL Research | 52.8% verified market data | India (fastest growing), Japan (reforms + low rates), South Korea, Singapore |

Asia Pacific is the fastest-growing regional market for real estate AI and analytics, with the global proptech market's APAC segment projected to expand at a 18.60% CAGR between 2026 and 2035 per verified global proptech market data the highest CAGR of all regions driven by massive residential and commercial real estate infrastructure investment in China, India, Japan, and Southeast Asia that is creating the data density and operational scale at which AI proptech platforms generate the most compelling return on investment. China ranked second globally in private AI investment at USD 9.30 Billion in 2024 per JLL Research verified data, with Chinese residential real estate platforms deploying AI at scale across search, valuation, mortgage underwriting, and property management for a market of approximately 1.4 billion potential real estate consumers. India is identified as one of the fastest-growing real estate investment markets in Asia Pacific per Savills Impacts research, with government infrastructure investment, urbanisation, and the expanding professional real estate services ecosystem creating accelerating demand for AI valuation, property management, and investment analytics platforms. Japan's corporate reforms and still relatively low interest rate environment per Savills are generating increased real estate investment activity that supports AI analytics platform adoption by institutional investors seeking data-driven underwriting capabilities in a market with historically limited digital data infrastructure.