| TROVIEW INTELLIGENCE | Smart Building Technology Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Component · By Application · By End Use · By Geography

Johnson Controls International plc's Building Solutions North America segment generated USD 11.3 billion in fiscal year 2024 with a Building Solutions backlog reaching USD 12.6 billion up 10% organically year-on-year and data center solutions representing 10% of company revenue in Q3 2025 with a USD 14 billion project backlog, Honeywell International Inc.'s Building Automation segment reported USD 6.54 billion in net sales for fiscal year 2024 an 8% organic increase year-on-year in Q4 2024 and 8% organic growth in Q1 2025 with building solutions growing 11% organically in both consecutive quarters per Honeywell's SEC Form 8-K filings, Siemens Smart Infrastructure achieved an 11% compound annual growth rate in revenue between fiscal years 2020 and 2024 with digital portfolio revenue increasing above 20% in fiscal 2024 and SI's addressable market projected to grow 5% to 6% annually to reach EUR 300 billion by 2029 from EUR 185 billion in 2020 per Siemens AG December 2024 Capital Market Event press release, Schneider Electric's Energy Management business saw 10% organic revenue growth in 2025 with its buildings end market expected to grow 4% to 5% annually over five years driven by EcoStruxure AI-powered solutions per Facilities Dive February 2026 reporting of Schneider full-year results, India's Smart Cities Mission delivered ICCCs using AI and IoT in all 100 smart cities with over 8,000 multi-sectoral projects representing INR 1.6 lakh crore (approximately USD 19.2 billion) in total investment at over 90% completion as of January 2025, and Honeywell's February 2025 study revealed that 84% of commercial building decision makers intend to increase AI usage over the next year confirming that the global smart building technology market is in a high-velocity structural adoption cycle with demand compounding across hardware, software, and services simultaneously.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

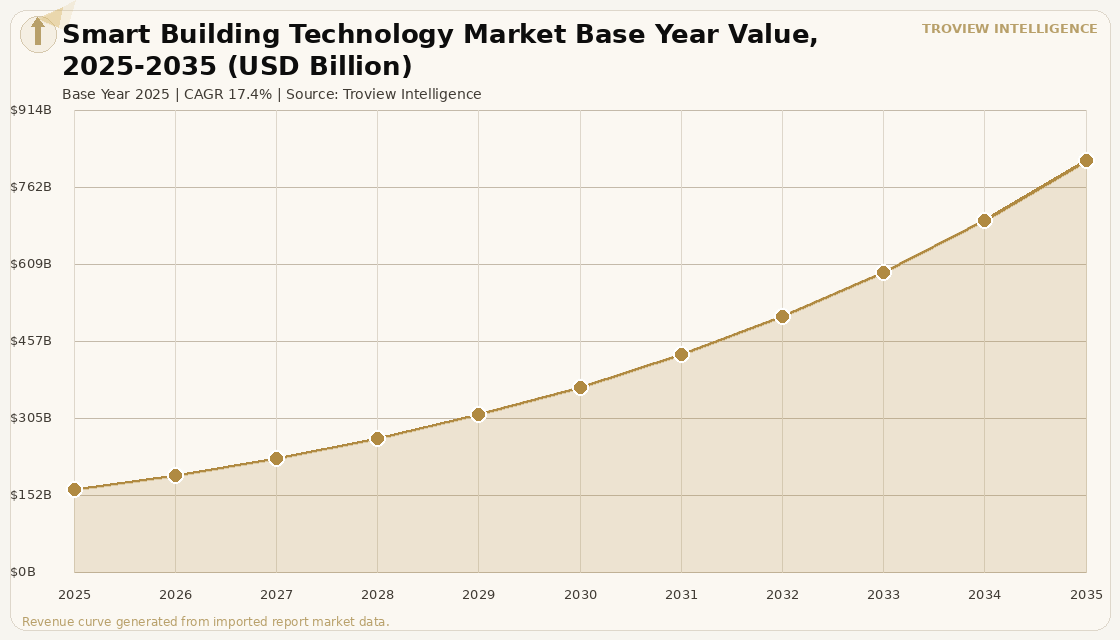

MARKET SYNOPSIS

The global smart building technology market size was USD 164.82 Billion in 2025 and is expected to register a revenue CAGR of 17.4% during the forecast period, reaching USD 816.24 Billion by 2035. The 2025 market estimate is grounded in verified company financial disclosures: Johnson Controls International plc's Building Solutions North America segment generated USD 11.3 billion in fiscal year 2024 with total company building solutions and global products revenues reaching approximately USD 22.9 billion, per company SEC 8-K filings; Honeywell International Inc.'s Building Automation segment reported USD 6.54 billion in net sales for fiscal year 2024 with organic sales growing 8% year-on-year in Q4 2024 and 8% again in Q1 2025 per Honeywell SEC Form 8-K disclosures; and Siemens Smart Infrastructure achieved an 11% compound annual growth rate in revenue between fiscal years 2020 and 2024 with the division's addressable market projected to grow 5% to 6% annually to EUR 300 billion by 2029 from EUR 185 billion in 2020 per the Siemens AG December 2024 Capital Market Event. The market encompasses the total addressable revenue generated by the hardware, software, and services ecosystem that converts conventional structures into intelligent, data-driven buildings spanning building management systems, IoT sensors and controllers, energy management platforms, HVAC automation, smart lighting, safety and security systems, access control, and the cloud-based analytics and AI software layers that optimise building performance across commercial, residential, and industrial segments. Market revenue growth is anchored in the convergence of three independently powerful demand forces: the corporate and regulatory drive toward net-zero carbon commitments that make energy-efficient building operations mandatory rather than optional, the AI and IoT technology wave that has transformed building management from periodic manual adjustment to continuous real-time optimisation, and the explosive growth of the data centre sector that is generating the largest single category of smart building infrastructure investment in the current cycle. Schneider Electric's buildings end market continues to drive performance due to robust demand in non-residential and technical buildings including healthcare and retail, reflecting its comprehensive offers across medium and low-voltage technologies, building management systems, and EcoStruxure advisors products to boost building energy efficiency, decarbonisation, reliability, availability, comfort, and safety per Schneider Electric's Q3 2024 earnings release. For instance, in March 2025, Siemens Smart Infrastructure, Germany, launched Building X Portfolio Manager, a SaaS platform consolidating real estate, energy, sustainability, and operational data across multiple sites and delivering AI-driven insights, emissions reporting, and real-time asset visibility per Siemens Smart Infrastructure press release of March 17 2025, representing the production-scale deployment of AI-powered smart building management infrastructure across Siemens' global commercial real estate customer base. These are some of the key factors driving revenue growth of the market.

The scale of smart building technology adoption in the commercial sector is confirmed by Honeywell's February 2025 study finding that 84% of commercial building decision makers intend to increase AI usage over the next year to optimise security, predictive maintenance, energy, water, and temperature management, a figure that signals that AI adoption in smart buildings is transitioning from early-adopter differentiation to mainstream operational standard across the commercial property sector. Buildings consume approximately 40% to 42% of global electricity per IBM Corporation and Schneider Electric reporting, creating both the environmental imperative and the economic incentive that drive smart building technology adoption across all geographies and property categories, as building operators who fail to deploy energy management and automation systems face both escalating utility costs and increasingly stringent regulatory compliance obligations under building energy performance standards being tightened in the European Union, United States, India, and China simultaneously. Siemens Smart Infrastructure helped customers avoid 44 million tonnes of CO2 emissions in fiscal 2024 alone per Siemens AG Capital Market Event December 2024, and Schneider Electric has enabled customers to avoid 679 million tonnes of CO2 emissions since 2018, illustrating the scale at which smart building technology platforms are delivering verified carbon reduction outcomes for the commercial real estate sector. These are some of the key factors driving revenue growth of the market.

However, the global smart building technology market faces structural constraints that limit the pace of adoption and penetration through the forecast period. The cost of implementing building management systems ranges from USD 2.50 to USD 7.00 per square foot, creating a return-on-investment calculation challenge that has led over 35% of medium-sized building developers in developing nations to delay smart upgrades due to financial constraints as of 2024, with the initial capital expenditure for comprehensive smart building infrastructure remaining a significant barrier for building owners with shorter investment horizons or lower tolerance for technology implementation risk. Integrating smart building systems with legacy infrastructure including the installed base of proprietary building automation systems, non-networked HVAC controls, and analogue security systems that characterise the vast majority of the existing global building stock requires technical expertise and investment that adds substantially to total project cost, with approximately 28% of smart buildings with networked systems experiencing some form of cyber threat in 2023 per global building security analysis, creating an additional cost and risk dimension that lowers the marginal return on smart building investments. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, create an energy cost environment that simultaneously motivates smart building adoption for its energy reduction benefits and constrains the capital budgets of building owners who are absorbing higher energy costs, reducing discretionary capital available for smart building system investment. These factors substantially limit global smart building technology market growth over the forecast period.

The most consequential change in the smart building market over the past three years is not the technology it is the customer. Johnson Controls' Building Solutions North America at USD 11.3 billion with a USD 14 billion data center backlog is not selling HVAC controllers. It is selling AI-powered infrastructure management for hyperscale computing facilities where the difference between an optimally managed thermal environment and a poorly managed one is measured in uptime, power usage effectiveness, and the contractual penalties that come with either. When Schneider says its buildings end market will grow 4% to 5% annually and its data center end market is the single biggest driver of companywide growth, what they are communicating is that the smart building technology market has bifurcated: the conventional office and retail building technology market has moderate, steady growth, and the mission-critical buildings market data centres, hospitals, pharmaceutical manufacturing, and advanced industrial facilities has structural double-digit growth driven by technology deployment requirements that building owners cannot defer regardless of interest rate cycles or capital budget constraints. Siemens projecting its addressable market to grow to EUR 300 billion by 2029 is not an aspirational statement. It is an accounting of the transition that is already underway." Troview Intelligence Head of Global Smart Building Technology Research

SEGMENT INSIGHTS

NORTH AMERICA JCI USD 11.3B N.AMERICA, HONEYWELL BA +8% ORGANIC, DATA CENTRE USD 14B BACKLOG

| JCI Building Solutions N. America FY2024 | Honeywell Building Automation FY2024 | JCI Data Center Backlog Q3 2025 | More than 138,000 |

| USD 11.3 Billion (SEC 8-K filing) | USD 6.54 Billion (+8% organic, SEC 8-K) | USD 14 Billion 10% of company revenue | Smart systems installed in US commercial buildings 2024 |

North America leads the global smart building technology market by both revenue and technology sophistication, anchored by the United States' deep commercial real estate ecosystem and the extraordinary data centre construction programme driven by AI infrastructure investment. Johnson Controls' Building Solutions North America segment generated USD 11.3 billion in fiscal year 2024 per company SEC 8-K filings, with a building solutions backlog reaching USD 12.6 billion up 10% organically in Q2 fiscal year 2024, and first half fiscal year 2024 orders for data centres having already surpassed all of fiscal year 2023 data centre orders per Johnson Controls' executive commentary on the Q2 earnings call. Honeywell Building Automation's Q1 2025 organic growth of 8% the second consecutive quarter of that rate was led by building solutions growing 11% organically in North America and over 50% in the Middle East per Honeywell's Q1 2025 SEC Form 8-K, with orders growing double digits year-on-year in both building solutions and fire products. More than 138,000 smart building systems were installed across commercial and institutional buildings in the United States in 2024 alone, with demand surging in cities including New York, Los Angeles, and Chicago per building automation market analysis.

| Siemens SI FY2024 Revenue | SI Buildings Revenue Growth FY2024 | SI Digital Portfolio Growth FY2024 | Building X Portfolio Manager |

| EUR 21.4 Billion (Siemens Annual Report 2024) | +6%, driven by solutions and services | Above 20% digital revenue EUR 1.7B | Launched March 2025 SaaS AI multi-site platform |

Europe's smart building technology market is defined by Siemens Smart Infrastructure's dominant market position, the European Union's regulatory-driven building energy performance agenda, and the Schneider Electric EcoStruxure ecosystem that serves the building energy efficiency requirements of European commercial real estate operators across Germany, France, the UK, and the broader EU. Siemens Smart Infrastructure achieved FY2024 revenues of EUR 21.4 billion with a record profit margin of 17.3% per Siemens AG's Annual Report 2024, having delivered an 11% compound annual growth rate in revenue between fiscal years 2020 and 2024, and with the Buildings sub-business growing 6% in FY2024 led by solutions and services per Memoori analysis of Siemens' Q4 FY2024 results. The March 2025 launch of Siemens Building X Portfolio Manager a SaaS platform consolidating real estate, energy, sustainability, and operational data across multiple sites with AI-driven insights and emissions reporting per Siemens Smart Infrastructure's press release of March 17 2025 represents the production-scale deployment of next-generation multi-site building management that European building portfolio owners and operators require to meet the EU's building energy directive compliance timelines.

| India Schneider Electric Growth 2024 | India Smart Cities Mission | NICDP 12 Smart City Projects | IGBC Green Buildings Registered |

| Double-digit non-residential buildings and Data Centre | INR 1.6 lakh crore total; 90%+ completion Jan 2025 | USD 3.41B investment approved August 2024 (CCEA) | 12 Billion sqft; 14,500+ certified projects |

Asia Pacific's smart building technology market is the fastest-growing region globally, anchored by India's double-digit growth in both non-residential buildings and data centre segments for Schneider Electric in 2024 and 2025 per Schneider's full-year results communication, and by China's data centre market recording strong growth from banking, telecoms, and social media customers per Schneider Electric's FY2024 earnings release. India's government has approved 12 new smart city projects under the National Industrial Corridor Development Programme with an investment of INR 286.02 billion (USD 3.41 billion) expected to attract INR 1.52 trillion (USD 18.12 billion) in private investment from large industries and MSMEs per the Cabinet Committee on Economic Affairs announcement of August 28 2024. Siemens Smart Infrastructure has specifically identified India as a stronghold market per its December 2024 Capital Market Event communications, and completed the acquisition of C&S Electric in 2021 to address India's growing power needs. The Indian Green Building Council has registered 12 billion square feet of green buildings and certified more than 14,500 projects per IGBC data, with the IGBC Bengaluru Chapter setting a target to certify 10 billion square feet over the next 10 years per Business Standard October 2024 reporting.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from company SEC filings, Siemens Annual Report 2024, Schneider Electric full-year results 2024, and verified company press releases.