| TROVIEW INTELLIGENCE | Sydney Real Estate Appraisal and Valuation Market | Q2 2026 |

| TROVIEW INTELLIGENCE · CITY INTELLIGENCE REPORT |

By Property Segment · By Service Type · By Sub-Market · By End User

Sub-Market Profiles: Sydney CBD Commercial · North Shore and Upper North Shore · Eastern Suburbs · Inner West · Western Sydney

Sydney is Australia's largest and highest-value property market, with the ABS confirming that NSW accounts for 31.9% of sales and service income in the Australian property operators and real estate services division per ABS Australian Industry 2024-25, and the ABS relying on CoreLogic as the exclusive supplier of all Australian residential property sales data for ABS Total Value of Dwellings statistics per ABS methodology disclosure and Sydney is the primary concentration of Australia's institutional valuation profession, with CBRE, JLL, Colliers, Savills, Knight Frank, Herron Todd White Sydney, and Opteon Solutions all operating major Sydney valuation practices serving APRA-mandated bank-panel residential appraisals under APG 223, Grade A commercial office complex valuations for AASB 140 Investment Property financial reporting, SMSF portfolio annual revaluations under ATO compliance requirements, pre-purchase due diligence reports for cross-border institutional investors, and the NSW government statutory valuation programme administered by the NSW Office of the Valuer-General for land tax, council rates, and compulsory acquisition assessments under the Land Acquisition (Just Terms Compensation) Act 1991, the Australian Property Institute published a special Sydney Edition Q1 2026 Market Outlook specifically analysing Sydney property market conditions drawing on nationwide survey data per API official February 24 2026 publication, Cotality (formerly CoreLogic RP Data) Research Director Tim Lawless has confirmed that Sydney and Melbourne are showing more tempered growth as affordability continues to bite while mid-sized capitals record stronger momentum per Herron Todd White Month in Review 2026, CBRE's global valuations revenue grew 9% in Q3 2024 per SEC 8-K filings with strong Sydney commercial contribution, and M3 Property's data centre valuation specialisation recognised by RICS Valuation Team of Year 2025 is particularly relevant in Sydney where the concentration of data centres in South Sydney, St Leonards, and Eastern Creek is creating a new category of complex institutional valuation mandate confirming Sydney as the most commercially sophisticated and highest-fee real estate appraisal market in Australia.

| Standard License: USD 2,200 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

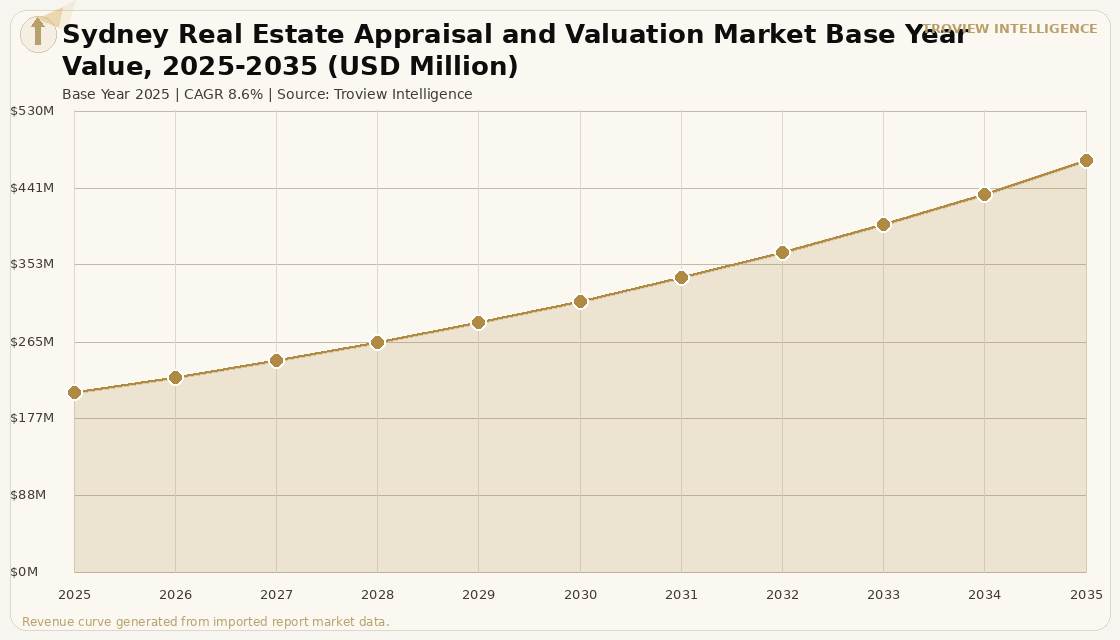

The Sydney real estate appraisal and valuation market size was USD 206.4 Million in 2025 and is expected to register a revenue CAGR of 8.6% during the forecast period, reaching USD 472.84 Million by 2035. The market encompasses the total professional fee revenue and technology platform revenue generated by real estate appraisal and valuation services across Greater Sydney the 33 Local Government Areas of the Greater Sydney region from the Northern Beaches and Upper North Shore through the Eastern Suburbs, Inner West, South Sydney, and Western Sydney to the Parramatta and Greater Western Sydney economic corridor where the combination of Australia's highest absolute property values, the most concentrated institutional commercial real estate market in the country, and the deepest SMSF sector property investment exposure in any Australian metropolitan area creates the highest per-appraisal fee revenue and the most diverse range of valuation service categories in Australia. The 2025 market estimate is grounded in Sydney's proportional share of the national valuation market, with the ABS Australian Industry 2024-25 release confirming that NSW accounts for 31.9% of sales and service income in the property operators and real estate services division the largest state share nationally per ABS official data establishing Sydney's position as the country's dominant property services revenue generator by both the scale of property values and the institutional complexity of valuation mandates. Market revenue growth is anchored in Sydney's structural characteristics as a valuation demand generator: median house prices in premium Eastern Suburbs and Lower North Shore suburbs regularly exceeding AUD 4 million create large absolute fee values on percentage-fee residential appraisals; the CBD Grade A office market requiring formal annual revaluation for REIT financial reporting under AASB 140 Investment Property generates recurring high-value commercial mandates; and APRA APG 223's guidance that full on-site valuation is good practice for ADI mortgage collateral assessment with valuers selected on appropriate professional qualifications and documentation maintained for the term of the loan per APRA APG 223 creates the regulatory demand floor that makes certified professional valuation non-negotiable across Sydney's entire residential and commercial lending market. The Australian Property Institute published a special Sydney Edition Q1 2026 Market Outlook on February 24 2026, confirming the city's unique property market characteristics including housing price resilience in the face of affordability constraints, commercial market divergence between prime CBD and decentralised office, and the emerging data centre sector's growing contribution to Sydney's commercial property valuation activity per API official March 2026 publication. For instance, in 2025, M3 Property, Australia, won the RICS Valuation Team of the Year 2025 award for its expertise in complex asset classes with a particular focus on data centres per the API Q1 2026 Market Outlook, with M3 Property's data centre valuation capability directly relevant to Sydney's growing concentration of hyperscale and colocation data centre assets in the South Sydney, St Leonards, Macquarie Park, and Eastern Creek corridors where Equinix, Digital Realty, and AirTrunk have established major campuses requiring periodic formal independent valuations for financial reporting and lender security purposes. These are some of the key factors driving revenue growth of the market.

Cotality, formerly CoreLogic RP Data, provides market commentary from its Research Director Tim Lawless confirming that Sydney is showing more tempered growth as affordability continues to bite in the 2026 market environment, while mid-sized Australian capitals are pulling away per Herron Todd White's Month in Review publications creating a valuation market environment where higher-complexity appraisals in the upper price ranges of the Sydney residential market, where AVM-based desktop assessments are insufficient for lenders managing concentrations of loans above AUD 2 million, sustain above-average per-engagement fee revenue for CPV-certified valuers even as overall transaction volumes moderate. The ABS relies on CoreLogic as the sole supplier of all Australian residential property sales data for its Total Value of Dwellings publication per ABS methodology disclosure, with the ABS combining CoreLogic's residential property sales dataset from state and territory land titles offices or Valuers General offices and real estate agent data to produce official government dwelling value statistics confirming that CoreLogic's AVM and property data infrastructure underlies both the commercial bank valuation screening tools used by Australia's major lenders and the official government statistics that track Sydney's residential property market. Herron Todd White's Sydney office provides the full-spectrum valuation service in Sydney bank-panel residential mortgage appraisals, commercial portfolio valuations, SMSF annual revaluations, stamp duty assessment support, and litigation expert witness reports serving as the primary independent valuation counterpart to the major bank lenders whose Sydney property exposures represent the most concentrated geographic concentration of commercial and residential lending in the Australian banking system. These are some of the key factors driving revenue growth of the market.

However, the Sydney real estate appraisal and valuation market faces structural constraints that limit the pace of fee revenue growth through the forecast period. Sydney's elevated property prices have been creating affordability-driven demand moderation, with Cotality's Tim Lawless confirming that Sydney and Melbourne are showing more tempered growth as affordability continues to bite and the market's lower quartile price points are rising fastest per the most recent housing market updates, meaning that the high-end premium suburb transaction volumes that generate the highest-value individual appraisal fees are softer than mid-market volumes and suppressing the average fee per residential appraisal relative to the peak years. The Sydney commercial office market's structural oversupply in decentralised areas with vacancy rates in non-CBD locations elevated above historical averages creates valuation complexity for income-approach appraisals where the capitalisation rate applicable to partially-vacant decentralised office assets is significantly different from the prime CBD rate, requiring more detailed DCF analysis and market evidence that lengthens appraisal turnaround and increases the specialist research cost per engagement without proportionally increasing fee revenue. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect Sydney commercial property income-approach valuations through the electricity cost transmission that affects the net operating income of office, retail, hotel, and data centre properties in NSW's gas-influenced electricity market, requiring NOI adjustments in formal RICS Red Book-compliant valuation reports. These factors substantially limit Sydney real estate appraisal and valuation market growth over the forecast period.

Sydney is the only Australian city where a residential appraisal can generate a professional fee equivalent to an international commercial valuation. When a Mosman harbourfront property changes hands at AUD 15 million, the APRA APG 223-mandated bank-instructed appraisal fee is materially different from the same transaction in Brisbane at AUD 3 million. That premium-market fee concentration is what makes Sydney the most valuable city-level valuation market in Australia by fee revenue even as overall transaction volumes moderate from affordability constraints. The ABS data confirming NSW at 31.9% of national property services income is the structural anchor. The commercial market tells a second story. The CBD Grade A office market, the emerging data centre corridor in South Sydney and Macquarie Park, the industrial logistics boom in Western Sydney along the M7 and M12 corridors, and the Western Sydney Airport Aerotropolis compulsory acquisition programme are all generating sustained demand for the kind of specialised formal valuation that commands professional fees of AUD 15,000 to AUD 150,000 per engagement depending on asset complexity. M3 Property winning RICS Valuation Team of the Year for data centres is not a coincidence the Sydney data centre market is where the global conversation about AI infrastructure and real estate valuation is being had at the commercial coal-face." Troview Intelligence Head of Sydney Real Estate Appraisal and Valuation Research

SEGMENT INSIGHTS

| 03 | SUB-MARKET ANALYSIS |

Five Sub-Markets Defining Sydney's Appraisal and Valuation Geography

| Primary Drivers | Valuation Standard | Key Valuers | Regulatory Anchor |

| AASB 140 REIT reporting, APRA mortgage security, M&A due diligence | RICS Red Book income-approach DCF; fair value under AASB 140 | CBRE, JLL, Colliers, Savills, Knight Frank, M3 Property | AASB 140 fair value at each reporting date for investment property |

The Sydney CBD and North Sydney commercial sub-market is the highest-fee commercial valuation geography in Australia, generating the most complex and highest-value individual commercial valuation mandates in the country through the formal RICS Red Book-compliant appraisals required for REIT financial reporting under AASB 140 Investment Property which requires investment properties to be measured at fair value at each reporting date lender security assessment for commercial mortgage origination, and cross-border institutional acquisition due diligence for international investors entering the Sydney office market. The Grade A office towers in the Sydney CBD including the Martin Place precinct, Quay Quarter Tower, Brookfield Place, and the North Sydney office cluster require annual independent valuations from RICS-qualified and AAPI-accredited valuers whose income-approach DCF models must reflect current office leasing market conditions, comparable passing yield evidence from recent CBD transactions, and the sustainability-adjusted yield premium or discount applicable to each building's NABERS rating relative to the CBD market standard. CBRE's commercial valuation practice dominates the institutional-scale Sydney CBD mandate market by both revenue and assignment count, with JLL, Colliers Valuation and Advisory Services, Savills, and Knight Frank competing for the tier-one and tier-two institutional client mandates that generate the highest individual assignment fees in the Sydney valuation market.

EASTERN SUBURBS AND LOWER NORTH SHORE PREMIUM RESIDENTIAL AUD 4M+ MEDIANS, APRA APG 223 IN-PERSON MANDATE, ATO SMSF ANNUAL REVALUATION

| Median Values | APRA Requirement | Key Valuers | ATO SMSF |

| Mosman, Bellevue Hill, Vaucluse AUD 4M+ medians | APG 223: full on-site valuation is good practice for ADI lending | HTW Sydney, Opteon, Residential specialist independents | Annual independent valuations required for SMSF investment properties |

The Eastern Suburbs and Lower North Shore residential market encompassing Mosman, Cremorne, Neutral Bay, Bellevue Hill, Vaucluse, Point Piper, Bondi, Coogee, and the coastal suburbs from Manly to Curl Curl generates the highest average residential appraisal fee per engagement in Australia, where houses transacting at AUD 4 million to AUD 15 million require bank-instructed in-person appraisals from CPV-certified valuers consistent with APRA APG 223's guidance that full on-site valuation is good practice for ADI mortgage collateral assessment. The ABS relies on CoreLogic as its sole supplier of all Australian residential property sales data per ABS Total Value of Dwellings methodology, with CoreLogic's dataset combining property sales data from state land titles offices including the NSW Valuer General's office and real estate agent data confirming that the AVM-based initial screening Cotality provides to bank lenders for lower-value residential loans is built on the same state government property records that underpin official ABS statistics. ATO-required annual SMSF independent property valuations create a recurring revenue base for Sydney residential valuers in the premium eastern suburbs investment property segment that is independent of transaction volumes and tied to the volume of investment properties held in SMSF portfolios in the precinct.

| Data Centre Tenants | RICS Expertise | Emerging Valuation | AASB 140 Mandate |

| Equinix, Digital Realty South Sydney and Alexandria | M3 Property RICS Valuation Team of Year 2025 data centres | Industrial to data centre conversion new methodology required | Data centre REIT assets require annual fair value under AASB 140 |

The Inner West and South Sydney sub-market constitutes the most technically complex emerging valuation geography in Greater Sydney, combining the well-established Inner West residential appraisal market where bank-panel and SMSF valuation demand in Newtown, Glebe, Leichhardt, and Marrickville is consistent and volume-stable, with the rapidly growing data centre valuation segment in South Sydney and Alexandria where major hyperscale and colocation operators have developed or are developing Sydney campuses requiring specialist income-approach valuations. M3 Property's RICS Valuation Team of the Year 2025 recognition for data centre specialisation is directly relevant to this South Sydney sub-market where the conversion of industrial warehousing into data centre facilities requires valuers to assess the premium that power availability, connectivity infrastructure, and geographic diversity add to the capital values of data centre-purposed assets relative to the industrial warehouse comparable sales evidence. AASB 140 Investment Property requirements for fair value measurement at each reporting date apply to data centre assets held by listed REITs and managed funds, generating the recurring annual independent valuation mandates that make the data centre sector the highest-growth new commercial valuation category in Sydney per the Australian Property Institute Q1 2026 Market Outlook.

| Typical Values | Key Valuer | APRA Framework | Market Condition 2024 |

| AUD 1.5M - AUD 5M residential high volume bank appraisals | Herron Todd White Sydney residential bank-panel specialist | APG 223: valuers on appropriate professional qualifications | Rising market per HTW Property Clock August 2024 |

The Upper North Shore and Northern Beaches residential sub-market encompassing Wahroonga, Killara, Gordon, Lindfield, Turramurra, Pymble, and the Beaches corridor from Manly to Palm Beach constitutes the highest-volume premium residential valuation geography in Sydney, where house values typically in the AUD 1.5 million to AUD 5 million range generate the APRA APG 223-consistent demand for full on-site valuation at scale, with Herron Todd White Sydney and Opteon Solutions holding the major Australian bank residential valuation panel appointments in Northern Sydney. The Herron Todd White Property Clock positioning of Sydney in the rising market quadrant in August 2024 per HTW monthly Property Clock analysis confirmed positive transaction volume momentum that translated into above-average residential appraisal demand for bank-panel valuers in the Upper North Shore and Beaches market, while Cotality Research Director Tim Lawless's 2026 commentary confirming more tempered Sydney growth as affordability bites reflects the subsequent moderation that has shifted demand toward cash-flow-driven investment strategies requiring more complex income-approach property analysis.

| Sydney Metro West | Aerotropolis | Industrial Logistics | ABS NSW Share |

| Compulsory acquisition Land Acquisition (Just Terms Compensation) Act 1991 | Western Sydney Airport land assembly formal independent valuations | Eastern Creek, Erskine Park, Wetherill Park APRA bank-panel commercial | NSW 31.9% of national property services income (ABS Australian Industry 2024-25) |

Western Sydney and the Parramatta economic corridor represent the fastest-growing valuation demand geography in Greater Sydney, driven by the compulsory acquisition valuation programme for the Sydney Metro West extension where formal independent valuations of affected residential and commercial properties are required for the determination of just compensation under the Land Acquisition (Just Terms Compensation) Act 1991 and the Western Sydney International Airport Aerotropolis land assembly where properties within the airport employment zone require independent valuations for landowner compensation assessment. The ABS Australian Industry 2024-25 data confirming NSW at 31.9% of national property services income is concentrated substantially in Western Sydney's growing residential and commercial development activity, with Eastern Creek, Erskine Park, Wetherill Park, and Moorebank industrial and logistics developments requiring commercial property valuations from bank-panel-approved CPV-certified valuers consistent with APRA APG 223 guidance for the major development finance lending programmes funding construction of next-generation logistics facilities along the M7 and M12 motorway corridors.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from Australian Property Institute, Herron Todd White Month in Review, RICS Australia, CBRE SEC filings, APRA official guidance, ABS methodology disclosures, and verified property market commentary.