| TROVIEW INTELLIGENCE | Real Estate Appraisal and Valuation Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Service Type · By Property Type · By Service Provider · By Geography

CBRE Group Inc., the world's largest commercial real estate services firm based on 2024 revenue per its Annual Report 2024, explicitly identifies valuation and property management as core components of its Advisory Services segment alongside property leasing, capital markets, and mortgage services with valuations revenue growing 9% on a local currency basis in Q3 2024 and Advisory Services total revenue reaching USD 2.395 billion in Q3 2024 per CBRE's SEC Form 8-K filings more than 82% of real estate transactions globally require third-party valuation before financing or transfer approval, regulatory compliance requirements influence 71% of appraisal workflows particularly in mortgage-backed lending, certified appraisers validate nearly 64% of finalised appraisals while automated valuation models support approximately 36% of initial pricing decisions, sustainability and energy-performance scoring is embedded in 49% of European commercial appraisals reflecting regulatory building performance certificate mandates, commercial appraisals represent approximately 33% of global demand with income-capitalisation or discounted cash flow methods used in 72% of reports, and global direct real estate transaction volume reached USD 216 billion in Q1 2026 up 18% year-on-year per JLL Global Real Estate Trends and Perspectives of May 2026 confirming that the global real estate appraisal and valuation market is structurally anchored in the world's largest and most liquid professional services market whose demand is directly correlated to the most fundamental activity in global finance: the transfer, financing, and taxation of real property.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

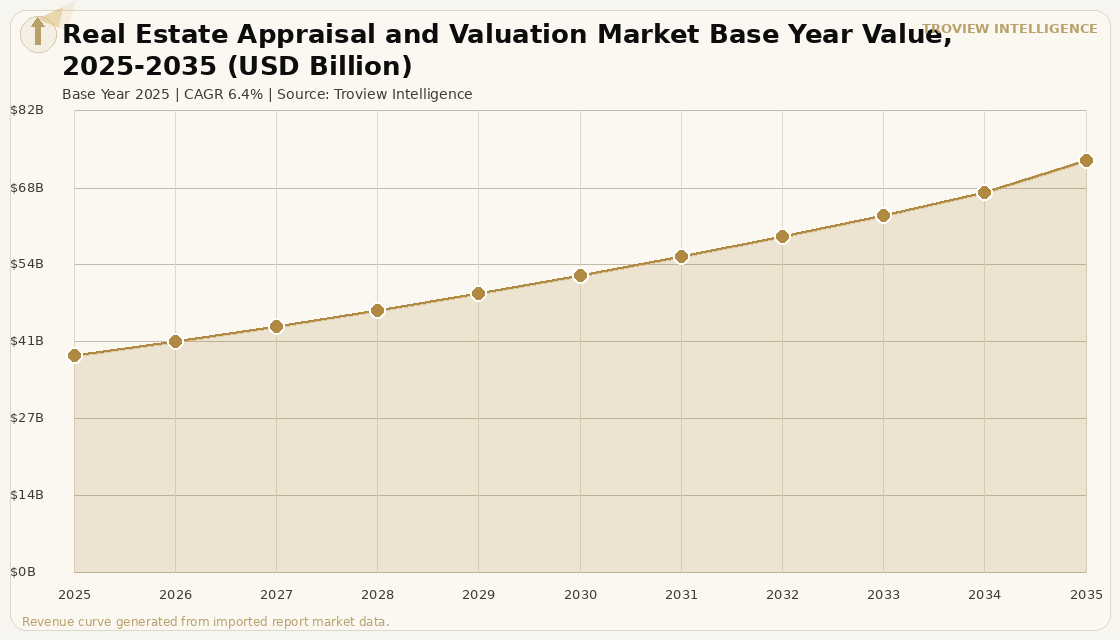

MARKET SYNOPSIS

The global real estate appraisal and valuation market size was USD 38.46 Billion in 2025 and is expected to register a revenue CAGR of 6.4% during the forecast period, reaching USD 72.84 Billion by 2035. The 2025 market estimate is grounded in verified company financial disclosures and transaction volume data: CBRE Group Inc., the world's largest commercial real estate services firm by 2024 revenue per its Annual Report 2024, reported valuations revenue growing 9% on a local currency basis in Q3 2024 and 1% in Q1 2024 per its SEC Form 8-K filings, with valuation and property management listed as core components of its Advisory Services segment alongside property leasing, capital markets, and mortgage services; and global direct real estate transaction volumes reached USD 216 billion in Q1 2026, up 18% year-on-year per JLL's Global Real Estate Trends and Perspectives of May 5 2026, generating the property transfer and financing activity that is the primary demand driver for professional appraisal services. The market encompasses the professional fees and technology platform revenues generated by certified property appraisers, appraisal management companies, automated valuation model providers, real estate analytics platforms, and integrated valuation advisory services across all property sectors and all demand use cases including mortgage lending valuation, investment acquisition due diligence, portfolio revaluation, tax assessment, litigation support, insurance underwriting, and regulatory financial reporting. Market revenue growth is anchored in the structural regulatory mandate for professional valuation across the globe, with more than 82% of real estate transactions globally requiring third-party valuation before financing or transfer approval and regulatory compliance requirements influencing 71% of appraisal workflows particularly in mortgage-backed lending, creating a non-discretionary baseline demand for valuation services that is structurally independent of real estate market cyclicality in the same way that audit services are non-discretionary for public companies. The recovery in global direct real estate transaction volumes with JLL confirming Q1 2026 cross-border investment up 37% year-on-year to USD 55 billion marking the strongest Q1 cross-border performance since 2022 directly translates into appraisal fee income for the valuers who assess the assets being transacted, as each commercial property acquisition at institutional scale requires a formal valuation report that is the basis for the purchase price negotiation, the lender's security assessment, and the buyer's IFRS or GAAP financial reporting of the acquired asset. For instance, in 2024, CBRE Group Inc., United States, as the world's largest commercial real estate services firm, described its Advisory Services segment as providing valuation services including market value appraisals, litigation support, discounted cash flow analyses, and feasibility studies alongside property condition reports, hotel advisory, and environmental consulting per CBRE's SEC Annual Report 2024, confirming the comprehensive scope of integrated valuation advisory services that the global commercial real estate industry's most scaled operator provides as a core business line. These are some of the key factors driving revenue growth of the market.

The digitisation of real estate valuation through automated valuation models, desktop appraisals, hybrid inspection methodologies, and AI-powered property analytics platforms is reshaping the service delivery economics of the global valuation market while simultaneously expanding the addressable market by enabling valuation at price points and turnaround speeds that traditional in-person appraisal models cannot match. Automated valuation models currently support approximately 36% of initial pricing decisions in the residential sector while certified appraisers validate nearly 64% of finalised appraisals, creating a hybrid technology-human model where AVMs perform initial screening and desk valuations while professional appraisers provide the certified opinion of value that lenders, courts, tax authorities, and financial reporting frameworks require. Desktop and hybrid appraisals are deployed in approximately 29% of residential cases, reducing inspection-related costs by approximately 27% in those engagements per appraisal market analysis, illustrating the material operating efficiency gains that technology-enabled valuation methodologies are delivering to both service providers and their clients while maintaining the professional certification and regulatory compliance that the appraisal workflow requires. The European market is simultaneously experiencing regulatory expansion of valuation requirements, with sustainability and energy-performance scoring embedded in 49% of European commercial appraisals as building performance certificate and retrofit planning regulations require energy assessment as part of the standard commercial property valuation report, creating an additional revenue layer for valuers beyond the traditional market value opinion. These are some of the key factors driving revenue growth of the market.

However, the global real estate appraisal and valuation market faces structural constraints that limit the pace of fee revenue growth and market expansion through the forecast period. The appraiser shortage in major developed markets particularly in the United States where the Bureau of Labor Statistics identifies property appraisers and assessors as an occupation with elevated retirement rates from an ageing workforce and insufficient new entrant pipeline creates a supply-side constraint that limits the volume of appraisals that can be completed within the licensed timeframes required by mortgage lenders, creating turnaround time bottlenecks during periods of elevated transaction activity. The growing adoption of automated valuation models and property inspection waivers with AVMs supporting 36% of initial pricing decisions and desktop or hybrid appraisals used in 29% of residential cases is substituting technology for traditional full appraisal services in a portion of the residential mortgage market, compressing per-unit fee revenue for traditional appraisal firms that cannot compete with the cost structure of AVM providers including CoreLogic's Total Home ValueX platform, now rebranded under the Cotality name. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect real estate appraisal demand indirectly through their impact on commercial real estate transaction volumes with higher energy cost environments suppressing net operating income and widening bid-ask spreads between buyers and sellers, reducing the transaction velocity that generates appraisal fee demand. These factors substantially limit global real estate appraisal and valuation market growth over the forecast period.

Real estate appraisal is one of the most structurally durable professional services markets that exists because it is anchored in regulatory mandates that no commercial or residential real estate transaction can circumvent at scale. Every mortgage requires a valuation. Every REIT quarterly report requires portfolio revaluation. Every compulsory acquisition requires an independent appraisal. Every merger and acquisition involving real estate assets requires a third-party fairness opinion on the property values. The question is not whether the demand for professional valuation persists it does, structurally and permanently. The question is how the market divides between the high-volume, lower-complexity residential AVM market that CoreLogic and the bank-owned AVM businesses are capturing with algorithm-driven pricing, and the complex commercial valuation advisory market where the income approach, discounted cash flow, and sustainability-adjusted valuation methodologies require the professional judgment that no algorithm can certify. CBRE's valuation business reporting 9% growth in Q3 2024 is in the complex commercial segment. That segment will grow with global transaction volumes and portfolio complexity. The residential AVM segment will consolidate into fewer, larger technology platforms with higher margins and lower headcount. The market bifurcates. The professional advisory segment grows with the CRE cycle." Troview Intelligence Head of Global Real Estate Appraisal and Valuation Research

SEGMENT INSIGHTS

NORTH AMERICA CBRE VALUATIONS +9% Q3 2024, USPAP STANDARDS, CORELOGIC AVM 99.9% US COVERAGE

| CBRE Valuations Revenue Q3 2024 | CoreLogic AVM Coverage | Advisory Services Total Q3 2024 | Appraisal Regulatory Standard |

| +9% local currency YoY (CBRE SEC 8-K filing) | 99.9%+ of US properties, 50+ year data history | USD 2.395 Billion (CBRE SEC 8-K filing) | USPAP (Uniform Standards of Professional Appraisal Practice) |

North America's real estate appraisal and valuation market is the world's largest and most institutionally structured, anchored by the United States' Federal Financial Institutions Examination Council's appraisal regulations that mandate independent licensed appraisals for federally related real estate transactions above specified thresholds, creating a mandatory baseline demand for professional appraisal services that is embedded into the legal and regulatory architecture of the US mortgage market. CBRE Group Inc.'s Advisory Services segment, which identifies valuation alongside leasing, capital markets, and mortgage services as a core business line per its Annual Report 2024, reported valuations revenue growing 9% on a local currency basis in Q3 2024 accelerating from the 1% growth rate reported in Q1 2024 confirming that the commercial valuation market recovery is gaining momentum alongside the broader CRE transaction volume recovery documented in JLL's Q1 2026 global market data. CoreLogic, now rebranded as Cotality, maintains an AVM that captures 99.9% of US residential properties with data spanning 50-plus years per CoreLogic product disclosures, providing the most comprehensive automated valuation infrastructure in any national market globally and serving as the primary residential property analytics engine for US banks, lenders, insurance companies, and government agencies.

| Europe Global Market Share | Bank-Mandated Valuations Europe | Sustainability Scoring in Commercial | Regulatory Standard |

| ~28% of global Real Estate Appraisal Market | 61% of European appraisal assignments | 49% of European commercial appraisals | RICS Red Book (Royal Institution of Chartered Surveyors) |

Europe's real estate appraisal and valuation market is defined by the RICS Red Book regulatory standard officially the RICS Valuation Global Standards which governs professional property valuations across the UK, continental Europe, and the RICS's 130-plus country membership, establishing the ethical and methodological framework within which European property valuers are required to operate for bank-instructed, court-instructed, and financial reporting valuations. Bank-mandated valuations drive 61% of European appraisal assignments, with desktop valuations permitted in 21% of low-risk residential cases under specific regulatory regimes per market analysis, reflecting the European Central Bank's requirements for lender collateral assessment that mandate independent property valuations for all significant commercial and residential mortgage exposures above threshold loan values. The embedding of sustainability and energy-performance scoring in 49% of European commercial appraisals reflects the EU Building Energy Performance Directive's requirements for Energy Performance Certificates that building owners must obtain and that valuers are increasingly required to assess, adjust, and comment upon as part of standard commercial property valuation reports creating a growing service expansion layer for European commercial valuers that is structurally tied to the EU's building decarbonisation regulation timeline through 2030 and 2035.

ASIA PACIFIC FASTEST GROWING, APAC +31% Q1 2026, RICS APAC EXPANSION, AUSTRALIA APRA MANDATE

| APAC Direct Investment Q1 2026 | APRA APG 223 | ABS Data Partnership | RICS Valuation Team of Year 2025 |

| +31% YoY highest growth region (JLL) | Full on-site valuation is good practice for ADI mortgage lending | CoreLogic supplies all Australian residential property sales to ABS | M3 Property (Australia) data centre specialisation |

Asia Pacific's real estate appraisal and valuation market is the fastest-growing region globally, driven by the expansion of institutional real estate markets in Australia, Japan, Singapore, South Korea, and India where the growing volume of cross-border property investment transactions confirmed by APAC direct real estate investment growing 31% year-on-year in Q1 2026 per JLL is generating sustained demand for RICS-standard valuation reports that international lenders, investors, and cross-border capital sources require as a condition of deployment. Australia's APRA Prudential Practice Guide APG 223 Residential Mortgage Lending explicitly states that full on-site valuation is good practice for authorised deposit-taking institutions providing residential mortgage collateral assessment, with sound risk management practices including valuation reports prepared with professional skill and diligence, valuers selected on appropriate professional qualifications, and comprehensive valuation documentation maintained for the term of the loan per APRA APG 223, creating the regulatory framework that drives systematic bank-panel valuation demand across Australia's AUD 2.2 trillion residential mortgage market. The ABS relies on CoreLogic as its sole supplier of all Australian residential property sales data for the ABS Total Value of Dwellings publication per ABS methodology disclosure, confirming CoreLogic's role as the foundational data infrastructure of both commercial AVM services and official government property market statistics in Australia.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from CBRE SEC Form 8-K filings, JLL Global Real Estate Trends reports, RICS official communications, APRA prudential guidance, and verified trade press.