| TROVIEW INTELLIGENCE | Luxury Hotel Real Estate Market | Q2 2026 |

By Geography - By Property Type - By Brand Category - By End-User

The global luxury hotel real estate market generated RevPAR of USD 342 for five-star and luxury-classified properties in 2025 a 9.4% year-on-year improvement as Marriott International and Hyatt Hotels Corporation expanded their luxury pipelines across the Middle East and Asia Pacific, Atlantis The Royal in Dubai achieved USD 1.4 billion in development investment to become the UAE's landmark ultra-luxury asset, and the global high-net-worth individual population grew at a sustained rate that is adding net new luxury travel demand at a pace that supply pipelines in constrained gateway cities including Dubai, Singapore, and Paris cannot match.

MARKET SYNOPSIS

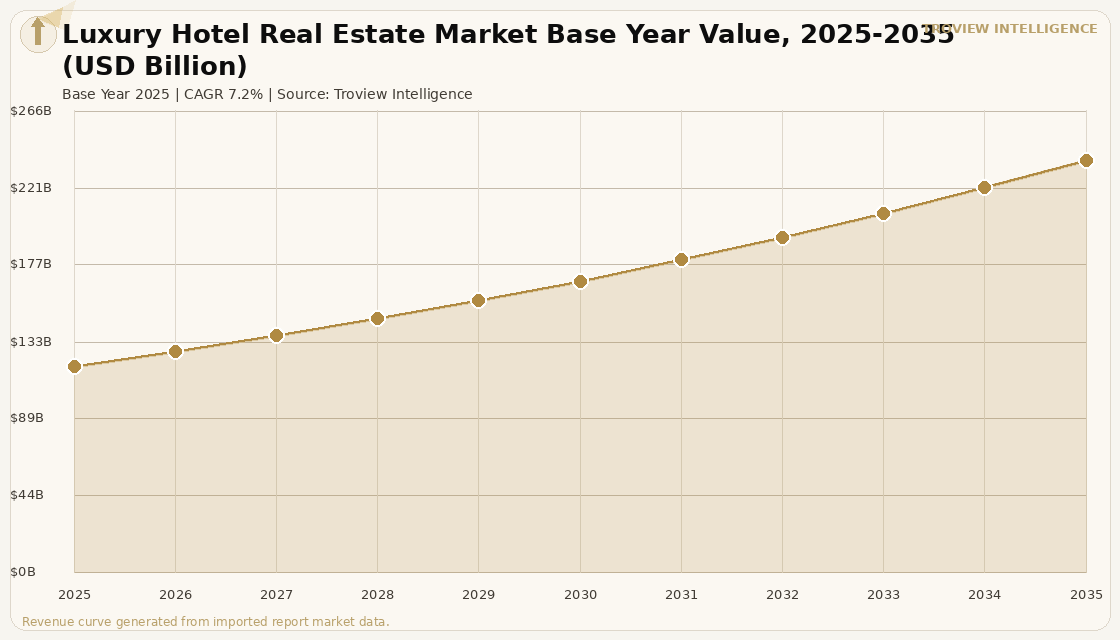

The global luxury hotel real estate market size was USD 118.64 Billion in 2025 and is expected to register a revenue CAGR of 7.2% during the forecast period, reaching USD 237.29 Billion by 2035. The luxury hotel real estate market encompasses the investment, development, and operational revenues generated by five-star and ultra-luxury hotel properties including branded urban hotels, resort developments, branded residences integrated with hotel infrastructure, and destination wellness and experiential lodges that serve the global high-net-worth and ultra-high-net-worth traveller base. Global RevPAR for five-star and luxury-classified properties averaged USD 342 in 2025, representing a 9.4% year-on-year improvement from 2024 per verified hospitality industry data, as elevated leisure demand converged with a strong recovery in corporate and MICE travel that had lagged leisure RevPAR recovery by approximately 18 months. North America held the largest market revenue share at 36.1% in 2025, with branded luxury hotel chains holding a 65.2% revenue share versus independent properties and generating ADR premiums of 15 to 25% over comparable unbranded inventory per verified market data. For instance, in January 2025, Mandarin Oriental Hotel Group, Hong Kong, announced plans to open a new luxury resort and residences in Cabo Rojo, Puerto Rico, set to debut in 2028 as part of the Esencia coastal community featuring 106 rooms and suites, private villas, five dining venues, a beach club, a Spa at Mandarin Oriental, and a Rees Jones-designed golf course, demonstrating the continued commitment of global luxury hospitality brands to resort-format development in high-demand leisure destinations. These are some of the key factors driving revenue growth of the market.

The Middle East is the fastest-growing luxury hotel real estate region, with the UAE delivering record performance across all key metrics in 2025: UAE RevPAR and ADR grew 11.9% year-on-year in the year to August per Knight Frank UAE Hospitality Market Review Autumn 2025, with Abu Dhabi recording RevPAR growth of 24% and ADR growth of 20.2%, and Dubai posting RevPAR growth of 10.1%. Branded luxury properties in Dubai command ADR premiums of 15 to 25% and achieve 5 to 7 percentage points higher occupancy than unbranded equivalents per verified market analysis, while Dubai's luxury segment specifically operates with average ADRs of approximately AED 1,470 (USD 400) and RevPAR of approximately AED 1,100 (USD 300) per verified hospitality intelligence. Asia Pacific generated the second-fastest CAGR in 2025, with Japan's yen depreciation driving an exceptional surge in luxury inbound tourism that LVMH confirmed contributed to a 32% performance improvement in its hospitality and retail operations in Q1 2024, and India's luxury hotel pipeline expanding to serve a domestic high-net-worth population that ranks fourth globally in ultra-high-net-worth individuals. Hyatt Hotels Corporation announced plans to open 50 luxury hotels by 2026, having opened 28 upscale properties in 2024 including the Park Hyatt London River Thames and Thompson Palm Springs, per Hyatt investor disclosure.

However, the global luxury hotel real estate market faces structural constraints that temper the pace of expansion. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation and travel uncertainty across the Middle East that threatens to dampen inbound luxury tourism from European and North American source markets at the margin particularly affecting properties in Abu Dhabi, Dubai, Ras Al Khaimah, and Qatar whose luxury RevPAR metrics are partially dependent on Western high-net-worth traveller flows that are sensitive to regional security perceptions. The construction and fit-out standards required for ultra-luxury hotel development with the USD 1.4 billion Atlantis The Royal representing the upper end of development cost per key at approximately USD 2.3 million for its 795 rooms and suites mean that new ultra-luxury supply in established gateway cities faces return on investment timelines of 12 to 20 years at unlevered IRRs of 8 to 12%, deterring all but the most patient institutional and sovereign capital from greenfield luxury hotel development. The acceleration of new luxury hotel supply in Dubai, where 12,000 new luxury keys are due by 2030, creates yield compression risk unless differentiation through experience, brand equity, and location remains strong enough to sustain ADR premiums above the weighted average of the expanding supply base. These factors substantially limit global luxury hotel real estate market growth over the forecast period.

The global luxury hotel real estate investment thesis in 2025 and 2026 rests on two structural forces that are simultaneously compressing cap rates and expanding the HNWI demand base. On the supply side, irreplaceable luxury hotel assets in gateway cities the Ritz-Carlton in DIFC, the Four Seasons on the Bosphorus, the Aman in Tokyo are genuinely irreplaceable: the land, the heritage, and the interconnected systems of brand, service culture, and physical asset cannot be replicated for any price within a reasonable time horizon. On the demand side, the global HNWI population is growing at a rate that outpaces luxury hotel key additions in every established gateway market. The constraint is not demand. The constraint is the planning, capital, and operational complexity of delivering ultra-luxury hotel product that can command ADRs above USD 400 with consistent quality of service. Dubai has solved this by combining sovereign capital, developer ambition, and a genuine demand surge from HNWI migration and event-driven tourism at a pace that no other city has matched in the post-pandemic cycle." Troview Intelligence Head of Global Luxury Hotel Real Estate Research

SEGMENT INSIGHTS

By Property Type

Urban luxury hotel property type is expected to account for a significantly large revenue share in the global luxury hotel real estate market during the forecast period.

Based on property type, the global luxury hotel real estate market is segmented into urban luxury hotels, luxury resort properties, branded residences integrated with hotel infrastructure, and destination wellness and experiential lodges. Urban luxury hotels dominate total revenue by generating the highest occupancy consistency through the combination of MICE, corporate, and leisure demand that fills rooms year-round without the seasonal volatility that afflicts pure resort assets. Branded luxury chains including Marriott Luxury Collection, Hilton Luxury and Lifestyle, and Hyatt's luxury portfolio held a combined 65.2% revenue share in 2025 per verified market data. Branded residences integrated with hotel infrastructure are expected to register the fastest revenue CAGR during the forecast period, as ultra-luxury brands including Four Seasons, Aman, and Mandarin Oriental expand their mixed-use development strategies that blend private residential sale revenue with ongoing hotel operating income, creating a dual revenue model that significantly improves development-stage returns and provides institutional investors with partial capital recovery at sale before the hotel stabilises.

By Brand Category

International luxury chain brand category is expected to account for a significantly large revenue share in the global luxury hotel real estate market during the forecast period.

Based on brand category, the global luxury hotel real estate market is segmented into international luxury chains, ultra-luxury independent and collection brands, soft brand collections, and unbranded independent luxury. International luxury chains dominate, with Marriott International's luxury portfolio including The Ritz-Carlton, St. Regis, W Hotels, EDITION, and The Luxury Collection generating the broadest geographic reach and the deepest loyalty programme distribution among the global luxury segment. Ultra-luxury independent and collection brands including Aman Resorts, Four Seasons Hotels and Resorts, and Rosewood Hotels are expected to register the fastest CAGR during the forecast period, as the global ultra-HNWI population's preference for exclusive, low-key-count properties with personalised service creates a demand premium for assets with 50 to 150 rooms that command ADRs of USD 800 to USD 3,000 per night in established luxury destinations.

By End-User

Leisure traveller end-user segment is expected to account for a significantly large revenue share in the global luxury hotel real estate market during the forecast period.

Based on end-user, the global luxury hotel real estate market is segmented into affluent leisure travellers, business and MICE travellers, bleisure travellers combining business and leisure, and luxury branded residence owners. Affluent leisure travellers dominate luxury hotel revenue, accounting for a structurally larger share since the post-pandemic period reshaped booking patterns in favour of extended leisure stays as hybrid working reduced the friction of combining travel with remote work. Business hotel guests constituted 32.3% of the luxury hotel market by type in 2025 per verified market data, with corporate and MICE travel recovery driving RevPAR growth in city-centre urban luxury properties including Dubai's DIFC corridor, Singapore's Marina Bay financial district, and New York's Midtown Manhattan hotel cluster. The bleisure traveller segment is expected to register the fastest CAGR during the forecast period as hybrid work schedules permanently extend business trip durations, converting 3-night corporate stays into 6-night combined business-and-leisure visits that generate significantly higher total spend per guest.

REGIONAL ANALYSIS

NORTH AMERICA LARGEST

| NA Revenue Share 2025 | US Share of NA Market | Hyatt 2024 Openings | Luxury Chain Revenue Share |

| 36.1% of global revenue | 87.8% of North America | 28 upscale properties | 65.2% of total luxury segment |

North America is the largest luxury hotel real estate market globally, driven by the combination of the world's highest density of HNWI demand in New York, Los Angeles, Miami, and San Francisco, the deepest corporate and MICE travel market for luxury hotel occupancy in major financial and technology centres, and the broadest luxury chain brand portfolio management infrastructure including Marriott's 30-plus luxury brand umbrella, Hilton's Luxury and Lifestyle division, and Hyatt's Alila, Andaz, Park Hyatt, and Thompson brands. Hyatt Hotels Corporation, United States, announced plans to open 50 luxury hotels by 2026, having successfully opened 28 upscale properties in 2024 including the Park Hyatt London River Thames and Thompson Palm Springs, per Hyatt investor disclosure and verified luxury hotel market data. The US market benefits from the deepest capital market liquidity for hotel real estate investment, with institutional hotel REITs including Host Hotels and Resorts and Park Hotels and Resorts providing liquid exit options for luxury asset investors at cap rates of 5 to 7% for stabilised urban luxury properties in gateway cities.

MIDDLE EAST

| UAE RevPAR/ADR Growth (YTD Aug 2025) | Dubai Luxury ADR (H1 2025) | Abu Dhabi RevPAR Growth | UAE Average Occupancy (YTD Aug) |

| +11.9% YoY (Knight Frank) | AED 1,470 (~USD 400) | 24% YoY growth | 78.5% (+4% YoY |

The Middle East is the fastest-growing luxury hotel real estate region in 2025, with the UAE delivering exceptional performance across all key operational metrics per Knight Frank's UAE Hospitality Market Review published October 2025. Dubai's luxury segment operates at average ADRs of approximately AED 1,470 (USD 400) and RevPAR of approximately AED 1,100 (USD 300), with branded luxury properties commanding 15 to 25% ADR premiums over unbranded equivalents and achieving 5 to 7 percentage points higher occupancy through distribution strength and brand recognition per verified hospitality intelligence. Atlantis The Royal, UAE, completed at an investment of USD 1.4 billion and representing approximately USD 2.3 million per key across its 795 rooms and suites, established the benchmark for ultra-luxury development investment and performance expectations in Dubai, with the property's automated-operational model which automated 40% of routine tasks while investing in specialist roles including sommelier teams, wellness experts, and experience curators providing an operational template for next-generation ultra-luxury hotel management. Saudi Arabia's Vision 2030 programme is the region's secondary growth driver, with NEOM, The Red Sea Project, and Diriyah collectively adding thousands of ultra-luxury keys targeting 100 million annual tourist arrivals by 2030.

ASIA PACIFIC SECOND

| APAC Revenue Share 2025 | Japan Luxury Driver | India HNWI Global Rank | Asia Pacific Pipeline Leader |

| ~22% of global luxury | Yen weakness LVMH +32% Q1 2024 | 4th globally by USD 100M+ holders | Japan, India, Thailand, Vietnam |

Asia Pacific is the second-fastest growing luxury hotel real estate region, with Japan recording exceptional luxury hotel performance driven by yen depreciation that made Japan one of the world's most cost-competitive luxury destinations for HNWI travellers from North America and Europe, with LVMH confirming a 32% performance improvement in its luxury retail and hospitality operations in Japan in Q1 2024 attributable to yen weakness and inbound tourist inflows. India's luxury hotel market is expanding to serve a domestic ultra-HNWI population that ranks fourth globally in individuals with net assets exceeding USD 100 million, with branded luxury hotel operators including ITC Hotels, Oberoi Hotels, and Taj Hotels investing in new properties in Bengaluru, Hyderabad, and Mumbai adjacent to the technology sector campuses that employ India's fastest-growing HNWI cohort. Thailand's luxury resort markets Koh Samui, Phuket, and Koh Lanta sustained premium ADR performance through 2025 as the post-pandemic experiential travel preference maintained European HNWI leisure demand for beach and wellness destination luxury resorts operating at 200 to 400 keys.