| TROVIEW INTELLIGENCE | Outpatient and Ambulatory Care Facility Market | Q2 2026 |

By Geography - By Facility Type - By Service - By Payer

The global ambulatory services market was valued at USD 928.95 Billion in 2025, outpatient surgeries accounted for 55% of all surgical procedures in developed economies in 2024, ambulatory surgical centres now handle over 60% of all US outpatient surgeries with ASC reimbursements rising 25% over five years per CMS data, the American Hospital Association reported a 15% rise in freestanding ambulatory surgery centres alongside a 15% increase in ambulatory care funding in 2025, and Australia reported 43.6 million non-admitted patient care service events in 2024-25 per Australian Institute of Health and Welfare data, confirming the structural migration of care from inpatient hospital settings to outpatient and ambulatory facilities across all major healthcare systems.

MARKET SYNOPSIS

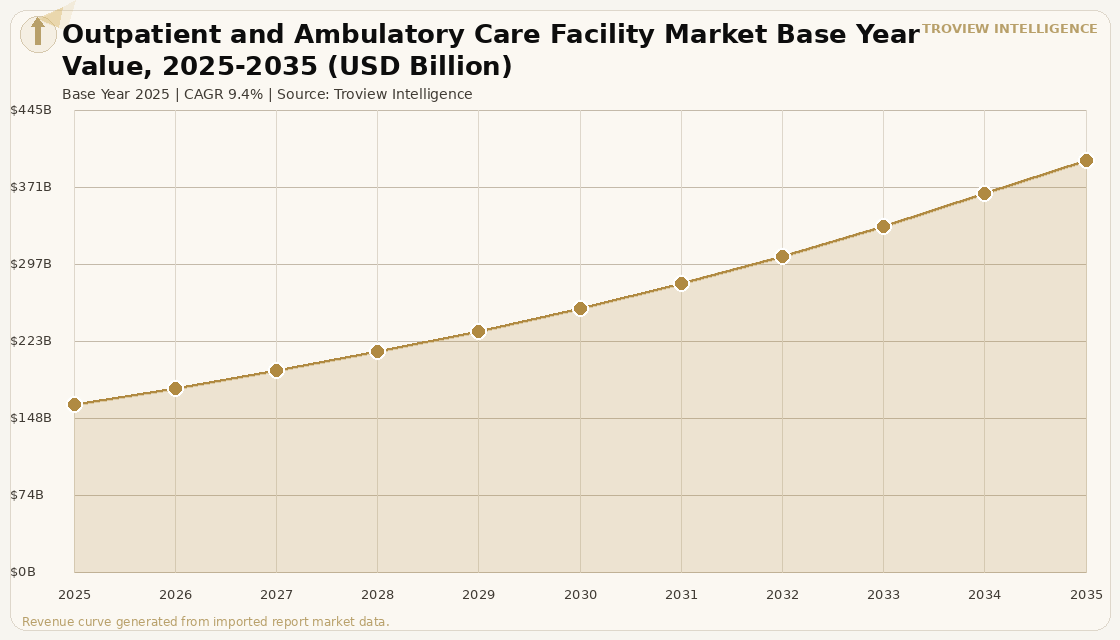

The global outpatient and ambulatory care facility market size was USD 162.84 Billion in 2025 and is expected to register a revenue CAGR of 9.4% during the forecast period, reaching USD 397.62 Billion by 2035. The outpatient and ambulatory care facility market encompasses ambulatory surgical centres, urgent care centres, diagnostic imaging and pathology clinics, primary care and specialist physician offices, community health centres, and hospital outpatient departments that collectively provide medical, surgical, and diagnostic services without requiring a patient overnight admission. Ambulatory surgical centres are the leading facility type, contributing 31.2% of total revenue in 2024, with ASCs in the United States alone handling over 60% of all US outpatient surgeries and performing more than 23 million procedures annually per verified market data. Outpatient surgeries accounted for 55% of total surgical procedures in developed economies in 2024, with outpatient visits in the United States rising 12% between 2022 and 2023 and outpatient visits increasing 9% annually in 2024 per verified industry data, confirming the structural migration of surgical and diagnostic volume from inpatient hospital settings to ambulatory facilities that reduce per-procedure cost by 35 to 50% compared to hospital-based inpatient alternatives. The 2025 market estimate is grounded in verified provider revenues: HCA Healthcare, United States, reported rising revenues and increased outpatient-related admissions in 2025; the US Department of Health and Human Services announced a USD 60 Million investment in 125 HRSA-funded community health centres in 2025; and CMS data showed a 25% increase in ASC reimbursements over five years, supporting rapid ASC expansion per Toward Healthcare ambulatory healthcare services market analysis. These are some of the key factors driving revenue growth of the market.

North America dominated the global outpatient and ambulatory care facility market in 2025, holding approximately 37 to 42% of revenue, supported by strong demand for outpatient procedures, rising value-based care adoption across Medicare and Medicaid that incentivises lower-cost ambulatory settings, and the most advanced regulatory infrastructure for ASC licensing and reimbursement globally. The American Hospital Association reported a 15% rise in freestanding ambulatory surgery centres and a 15% increase in ambulatory care funding and incentivisation programmes in 2025, while 11,815 ASCs are currently active across the United States per Definitive Healthcare SurgeryView verified data. Asia Pacific is the fastest-growing region, expanding at 8.0% to 8.2% CAGR through 2035, driven by rising chronic disease prevalence across China, India, Indonesia, and Vietnam, rapid urbanisation creating demand for accessible non-hospital medical care, and government investments in primary care and community health infrastructure in markets including India's 2.5% of GDP healthcare spending target and China's foreign investment provisions for healthcare. The growing integration of telehealth with physical ambulatory facility networks with global telehealth adoption growing 25% year-on-year in 2024 per verified market data is expanding the effective service radius of ambulatory care facilities by enabling virtual pre-consultation, remote monitoring, and post-procedure follow-up that reduces facility visit frequency while maintaining clinical continuity.

However, the global outpatient and ambulatory care facility market faces structural constraints that limit the pace of expansion across multiple markets. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation and medical supply chain cost pressures that increase operating costs for ambulatory care facilities whose consumable supply chains including surgical drapes, disposable instruments, diagnostic reagents, and imaging contrast media depend on global logistics networks affected by elevated freight costs and energy surcharges. Staffing shortages and wage inflation represent a structural constraint across all global ambulatory care markets, with nursing and allied health professional workforce shortfalls projected to intensify as ageing population demand for care outpaces educational programme graduation rates particularly acute in Australia, United Kingdom, and Canada where Commonwealth Fund surveys confirm sustained primary care workforce gaps. Reimbursement rate compression from private health insurers who are applying claims review and prior authorisation processes that delay or deny ambulatory procedure approvals is limiting revenue realisation for ambulatory facility operators who carry fixed-cost infrastructure investments against variable procedure volumes. These factors substantially limit global outpatient and ambulatory care facility market growth over the forecast period.

The structural shift from inpatient to outpatient care is the most consequential long-term trend in global healthcare delivery. It is driven by three forces that are simultaneously reinforcing each other: technology has made complex procedures safe enough for same-day discharge; payers have re-priced inpatient and outpatient procedures to make the cost differential undeniable; and patients actively prefer the convenience, privacy, and lower infection risk of ambulatory settings. The 55% outpatient surgery share in developed economies in 2024 is the mid-point, not the ceiling. In the United States, CMS continues expanding the list of procedures approved for ambulatory surgical centre reimbursement. In Australia, 43.6 million non-admitted patient care events in 2024-25 represent a decade of sustained shift away from overnight admission. The market's challenge is not demand. The challenge is the staffing infrastructure nurses, anaesthetists, surgical technicians that limits throughput at well-capitalised ambulatory facilities from operating at the patient volumes their physical capacity could accommodate. Private equity has recognised this: at least 409 healthcare buyout deals occurred in North America and Europe in 2024, with ASCs among the most actively targeted assets precisely because the procedure growth pipeline is visible but the operational bottleneck is solvable." Troview Intelligence Head of Global Outpatient and Ambulatory Care Facility Research

SEGMENT INSIGHTS

By Facility Type

Ambulatory surgical centres facility type is expected to account for a significantly large revenue share in the global outpatient and ambulatory care facility market during the forecast period.

Based on facility type, the global outpatient and ambulatory care facility market is segmented into ambulatory surgical centres, urgent care and walk-in centres, diagnostic imaging and pathology clinics, primary care and general practice offices, specialist outpatient clinics, and community and federally qualified health centres. Ambulatory surgical centres dominated with a 31.2% revenue share in 2024 per verified market data, with ASCs now handling over 60% of US outpatient surgeries and performing more than 23 million procedures annually across orthopaedics, ophthalmology, gastroenterology, and pain management specialties. Diagnostic and therapeutic services are expected to register the fastest revenue CAGR at approximately 7.5% during the forecast period, driven by growing demand for outpatient diagnostic imaging, pathology, and point-of-care testing as early detection programmes and chronic disease management protocols drive patients through diagnostic touchpoints multiple times per year outside traditional hospital radiology departments.

By Service Type

Surgical services type is expected to account for a significantly large revenue share in the global outpatient and ambulatory care facility market during the forecast period.

Based on service type, the global outpatient and ambulatory care facility market is segmented into surgical services, primary care and preventive services, diagnostic services, rehabilitation and physiotherapy, urgent and emergency care, and telehealth-integrated virtual care. Surgical services dominated with a 55% share in 2025 per verified ambulatory services market data, as minimally invasive surgical techniques including laparoscopic, arthroscopic, and endoscopic procedures enabled same-day discharge for procedure categories cataract surgery, knee arthroscopy, hernia repair, colonoscopy that previously required overnight hospitalisation. Ambulatory surgery now accounts for more than 90% of cataract procedures and 75% of hernia repairs in developed markets per verified ambulatory care market data. Telehealth-integrated virtual care is expected to register the fastest CAGR during the forecast period, growing at approximately 8.4% through 2034, as ambulatory facility operators extend their patient relationship through virtual follow-up and remote monitoring that increases procedure throughput per physical facility.

By Payer

Private insurance payer segment is expected to account for a significantly large revenue share in the global outpatient and ambulatory care facility market during the forecast period.

Based on payer, the global outpatient and ambulatory care facility market is segmented into private health insurance, public insurance and Medicare or Medicaid equivalents, self-pay and out-of-pocket patients, and employer-sponsored occupational health plans. Private health insurance contributed the highest revenue share at 40% in 2025 per verified market data, financing the majority of elective outpatient procedures in markets including the United States, Australia, and Germany where private insurance supplements public healthcare coverage for specialist and elective care. Public insurance and Medicare or Medicaid equivalents are expected to register the fastest CAGR during the forecast period, as government programmes in the United States, Australia, and European nations expand ambulatory care reimbursement to reduce pressure on publicly funded inpatient hospital systems that face chronic bed capacity constraints and elective surgery waiting list backlogs.

REGIONAL ANALYSIS

NORTH AMERICA DOMINANT, 11,815 ACTIVE ASCs, CMS REIMBURSEMENT EXPANDING

| NA Revenue Share 2025 | Active US ASCs (2024) | US Outpatient Surgery Share | CMS ASC Reimbursement Trend |

| ~38-42% of global market | 11,815 facilities (Definitive HC) | 60%+ of all US outpatient surgeries | 25% increase over 5 years CMS data |

North America is the global outpatient and ambulatory care facility market leader, anchored by the United States where 11,815 ambulatory surgical centres are currently active per Definitive Healthcare SurgeryView data, handling more than 60% of all US outpatient surgeries and performing over 23 million procedures annually. The CMS demonstrated a 25% increase in ASC reimbursements over five years, with the American Hospital Association reporting a 15% rise in freestanding ASC count and a 15% increase in ambulatory care funding and incentivisation programmes in 2025 . Private equity investment in ASCs is accelerating, with at least 409 healthcare buyout deals in North America and Europe in 2024 per Bain and Company data, with ASCs among the most actively targeted assets as PE firms with significant dry powder deploy capital into procedure-growth-visible, operationally scalable ambulatory platforms. Medicare spending increased by USD 8.5 Billion as outpatient visits rose, reinforcing the reimbursement infrastructure that makes ASC investment financially sustainable for institutional capital.

ASIA PACIFIC

| APAC CAGR (through 2035) | Australia Non-Admitted Events 2024-25 | Australia Hospital Spend 2023-24 | India Healthcare GDP Target |

| 8.0-8.2% fastest global region | 43.6 million service events (AIHW) | AUD 113.8bn AUD 4,223 per person | 2.5% of GDP by 2025 |

Asia Pacific is the fastest-growing global outpatient and ambulatory care facility market region, driven by rising chronic disease prevalence, rapid urbanisation, and government investments in primary care infrastructure. Australia's outpatient and ambulatory care market is the region's most mature, with the Australian Institute of Health and Welfare confirming that 43.6 million non-admitted patient care service events were provided for public patients in 2024-25 encompassing 22.7 million allied health and clinical nurse specialist services, 14.1 million medical consultation services, and 3.6 million diagnostic services per AIHW hospitals data. Australia spent AUD 113.8 billion (AUD 4,223 per person) on hospital care in 2023-24 per AIHW health expenditure data, representing 42% of all Australian health expenditure, with private hospitals admitting 5,142,645 patients in 2023-24 including 3,812,478 same-day admissions a 3% increase on the prior year confirming the structural growth of day-surgery and ambulatory care across Australia's private hospital sector per Australian Private Hospitals Association verified data. India's ambulatory care market is the region's fastest-growing, with the Indian government targeting 2.5% of GDP in healthcare spending by 2025 and expanding Primary Health Centre and community health infrastructure across underserved districts.

EUROPE STEADY

| Europe Market Position | UK NHS Ambulatory Investment | German ASC Growth Driver | Europe ASC Procedure Share (2024) |

| 2nd largest region, mature markets | Cancer and Advanced Ambulatory Building 2027 | Long-wait elective surgery migration | 55%+ of surgical procedures in developed EU |

Europe is the second-largest global outpatient and ambulatory care facility market, with mature markets in Germany, France, the Netherlands, and the United Kingdom driving sustained demand for ambulatory surgical and diagnostic services. The UK National Health Service revealed plans for a Cancer and Advanced Ambulatory Building that will offer integrated cancer care and outpatient surgery services with an expected 2027 opening per Market.us ambulatory care market data, reflecting the broader European trend of combining specialised treatment with outpatient convenience to reduce inpatient admission pressure on hospital systems operating at near-full bed capacity. Germany's ambulatory care market is growing rapidly as the country's healthcare system addresses elective surgery waiting list backlogs through ASC network expansion that provides surgical capacity outside the tariff-constrained public hospital system. European value-based care adoption where ambulatory procedures are reimbursed on a bundled outcome basis rather than a fee-for-service episode is creating incentive structures that reward ambulatory facility operators for achieving faster recovery and lower readmission rates.