By Zone - By Property Type - By Guest Profile - By Season

Zones: Patong Beach - Kata and Karon - Phuket Town - Bang Tao - Rawai

Phuket recorded H1 2025 hotel occupancy of 79.5% with ADR of THB 5,652 up 7.8% year-on-year per Knight Frank Thailand, January 2025 occupancy reached 91.8% exceeding pre-pandemic levels, hostel dormitory bed rates run USD 10 to USD 20 per night 25 to 50% above mainland Thailand rates the island processed 19.7 million airport passengers in 2024 with a second international airport planned for 12.5 million additional annual capacity, and December 2025 to February 2026 peak reservations were near-exhausted months in advance with budget and mid-range accommodation seeing 10 to 25% price increases.

MARKET SYNOPSIS

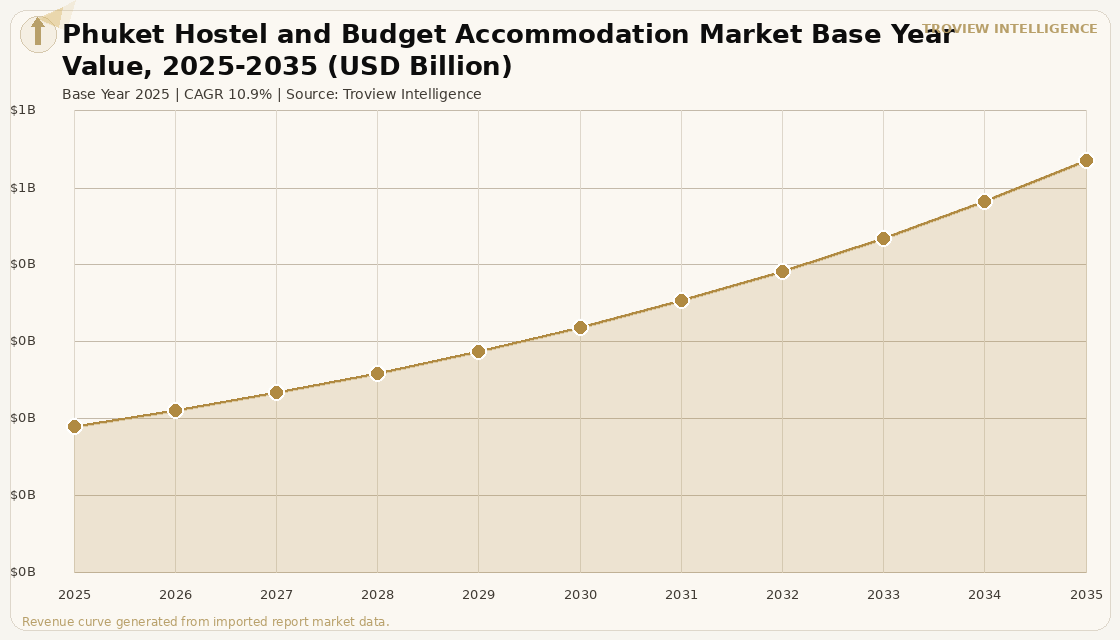

The Phuket hostel and budget accommodation market size was USD 0.22 Billion in 2025 and is expected to register a revenue CAGR of 10.9% during the forecast period, reaching USD 0.62 Billion by 2035. Phuket is Thailand's highest-ADR major tourism destination and the country's most supply-constrained island budget accommodation market, with dormitory bed rates of USD 10 to USD 20 per night running 25 to 50% above mainland Thailand rates due to island logistics premium costs and peak-season demand concentration that drives December to February occupancy above 85% and January occupancy to 91.8% per GuestMetrix and Knight Frank verified data. The island processed 19.7 million passengers through Phuket International Airport in 2024 confirming its position as Thailand's second-largest aviation hub with direct international flights serving more than 64 countries and European source markets including Russia (1.9 million Thailand-wide in 2025), United Kingdom (850,000), Germany, and France generating the year-round leisure demand base that Phuket's hostel and budget accommodation sector relies upon for above-75% annual occupancy. Phuket's H1 2025 hotel market recorded ADR of THB 5,652 a 7.8% year-on-year increase and occupancy of 79.5%, outperforming Bangkok's H1 2025 occupancy of 75.1% by 4.4 percentage points per Knight Frank Thailand H1 2025 hotel market report published September 2025. For instance, in advance of the December 2025 to February 2026 high season, Phuket accommodation across budget, mid-range, and resort categories recorded 10 to 25% price increases with advance reservations near-exhausted months before the arrival dates per The Asian Affairs reporting, confirming that Phuket's supply-constrained peak season creates pricing power for budget hostel operators that Bangkok's oversupplied market cannot replicate. These are some of the key factors driving revenue growth of the market.

Phuket's hostel and budget accommodation market in 2025 is characterised by a structural geographic tension between the island's premium positioning which pushes midscale hotel ADR above Bangkok's average and compresses the absolute affordability that defines budget backpacker travel and the continued strong demand from European and long-haul backpackers for whom Phuket's beaches, nightlife, and island-hopping access justify paying a budget premium. SKHAI's STAYLAR-managed properties in Phuket reported net rental yields of 7.8% to 8.4% in 2025, with occupancy ranging from 72% to 78% and average daily rates at USD 285 per SKHAI platform data, confirming the premium yield dynamics of Phuket's accommodation market across all accommodation tiers. The island's geographic supply constraint available development land on Phuket's west coast is increasingly scarce, particularly in prime Patong, Kata, and Karon locations per SKHAI verified analysis creates a structural undersupply dynamic that prevents the kind of new budget hostel supply competition that characterises Bangkok's oversaturated market. A planned second international airport for Phuket, projected to handle 12.5 million passengers annually per government plans, will expand airlift capacity and add new source market arrivals that should sustain hostel occupancy growth through the forecast period.

However, the Phuket hostel and budget accommodation market faces structural constraints that limit sustainable occupancy growth. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating long-haul airfare cost increases from fuel surcharges that raise the total cost of the Thailand backpacking trip for European and North American source markets with Phuket already carrying a 25 to 50% accommodation cost premium over mainland alternatives, additional airfare increases compress the all-in budget of price-sensitive travellers and may redirect some circuit routing toward lower-cost Bali, Vietnam, or Laos alternatives. Chinese tourist arrivals to Thailand declined approximately 35% in H1 2025 year-on-year while Phuket is less exposed to this than Bangkok due to its European demand predominance, the Chinese market historically contributed significant low-season hostel and guesthouse occupancy in Phuket's Patong and Karon zones that is difficult to replace at the same booking volumes from alternative source markets. Seasonal demand concentration with December to February generating 85 to 95% occupancy while May to October monsoon season occupancy falls to 45 to 65% creates cash flow management challenges for hostel operators who carry fixed costs including staff, lease, and utilities year-round but generate the majority of annual revenue in four to five peak months. These factors substantially limit Phuket hostel and budget accommodation market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "Phuket is the most expensive budget travel destination in Southeast Asia and it is the most popular. That apparent contradiction resolves when you understand what Phuket is actually selling to the budget traveller. It is not just a beach. It is the Andaman Sea, Phi Phi Island proximity, world-class diving access, a live music and nightlife scene, and infrastructure ATMs, 7-Elevens, English menus, reliable medical facilities that backpackers in genuine budget destinations like Laos or Cambodia cannot take for granted. Phuket charges a premium for infrastructure convenience and product quality, and its guest base predominantly European, Australian, and North American backpackers and flashpackers pays that premium willingly. The USD 10 to USD 20 dorm bed in Phuket generates better RevPAR for the hostel operator than a USD 7 dorm bed in Bangkok because it is sold at higher occupancy in peak season and the ancillary spend tours, bars, activities is dramatically higher per guest in Phuket than in any mainland Thailand destination. The structural risk is airfare cost. If the per-person round-trip cost from London or Sydney increases by USD 150, some of those travellers choose Bali or Vietnam. But Phuket's total value proposition especially Phi Phi and the Similan Islands creates stickier demand than any other Southeast Asian beach destination." Troview Intelligence Senior Analyst, Phuket Accommodation Markets

SEGMENT INSIGHTS

Zone Deep-Dives

| Zone Hostel Profile | Dorm Rate Range | Peak Occupancy | Key Anchors |

| Highest bed count in Phuket | USD 12-20 per dorm night | 85-95% Dec-Feb | Bangla Road, Central Festival, Patong Beach |

Patong Beach is Phuket's primary hostel and budget accommodation zone, concentrating the majority of the island's dormitory hostel inventory, budget guesthouses, and social backpacker bars along and adjacent to Bangla Road one of Southeast Asia's most intensely developed nightlife and entertainment streets. Hostel dorm rates in Patong range from USD 12 to USD 20 per night, with peak December to February occupancy reaching 85 to 95% as European winter escapees and Australian and North American year-end travellers fill every available hostel bed on the island. Patong's competitive hostel advantage is proximity to function: the beach, Bangla Road nightlife, Central Festival shopping, and the Rassada Pier departure point for Phi Phi Island ferry services are all within 10 minutes of the central hostel cluster, providing the activity density and social environment that motivates backpackers to pay Patong's premium over quieter and cheaper island alternatives. Mad Monkey Hostels and several independent social hostel operators have built their Phuket operations around Patong's activity ecosystem, offering organised Phi Phi snorkelling day tours, sunset beach bar events, and poolside social programming that differentiates their properties from commodity dorm competitors at similar bed rate levels.

Kata and Karon FAMILY-FRIENDLY ZONES, LOWER PRICE POINT, SURF AND DIVE LED

| Zone Character | Dorm Rate Range | Key Activities | Guest Profile |

| Quieter beach, surf, family resort | USD 10-16 per dorm night | Surfing (Kata), PADI dive courses | Couples, small groups, adventure travellers |

Kata and Karon beaches south of Patong represent Phuket's mid-market hostel zone, offering dormitory accommodation at USD 10 to USD 16 per night in a quieter beach environment that attracts couples, small travel groups, and adventure travellers seeking surf and dive activity bases without the intensity of Patong's nightlife. Kata Beach is Phuket's primary surfing beach, with consistent waves during the May to October southwest monsoon season creating a counter-seasonal demand driver that sustains hostel occupancy in the months when Patong's beach-and-party demand drops to its seasonal minimum. PADI dive certification courses operating from Karon and Kata bases generate multi-night stays of 3 to 5 days for travellers completing open water or advanced dive certification, providing hostel operators in these zones with above-average length-of-stay income that partially compensates for lower per-night ADR relative to Patong. The zone's quieter character compared to Patong and its beach road cafe and restaurant culture attract a slightly older and higher-spending backpacker cohort the 25 to 35 year-old flashpacker who will pay USD 50 for a private hostel room over a USD 14 dorm bed that generates better RevPAR per booking than the pure-economy dorm guest.

| Heritage Profile | Dorm Rate Range | Growth Driver | Guest Profile |

| Sino-Portuguese Old Town architecture | USD 10-18 per dorm night | Instagram, food culture, design hostels | Cultural travellers, digital nomads, DTV visa |

Phuket Town is the island's fastest-growing hostel and budget accommodation zone, driven by the growing travel media coverage of Phuket Town's Sino-Portuguese Old Town heritage architecture, vibrant independent food and beverage scene, and Sunday Walking Street market that collectively provide the cultural programming that beach-focused Patong and Kata cannot match. Lifestyle hostel operators have established design-led properties in converted shophouses within the Old Town's protected heritage streetscapes, creating accommodation with genuine architectural character teak floors, mosaic tile bathrooms, indoor courtyard gardens, rooftop cafes that commands dorm rates of USD 10 to USD 18 and generates strong social media content value that drives organic discovery and high direct booking conversion rates. Phuket Town's position as the island's transport hub with songthaew routes to all major beaches, the ferry port to Phi Phi, and proximity to Phuket Bus Terminal makes it a logistically convenient base despite being 15 to 20 kilometres from the primary beach zones. Digital nomads and Destination Thailand Visa long-stay travellers increasingly choose Phuket Town over the beach zones for extended stays, drawn by lower costs, better coffee shop and coworking infrastructure, and the liveable neighbourhood character of the Old Town's residential streets.