| TROVIEW INTELLIGENCE | Real Estate Tokenization and Digital Assets Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Geography · By Asset Class · By Blockchain Infrastructure · By Investor Type

Deloitte's Center for Financial Services projected in April 2025 that the global real estate tokenization market could reach USD 4 trillion by 2035 growing at a compound annual rate of 27% from current levels under USD 300 billion, RWA token value on public blockchains neared USD 18 billion by June 2025 representing a 380% increase from approximately USD 5 billion in 2022 per Chainalysis 2025 crypto market report, the total on-chain RWA market excluding stablecoins reached approximately USD 24 billion by mid-2025 per RWA.xyz on-chain market datatsville with private credit accounting for USD 14 billion or 58% of that total, the GENIUS Act passed in July 2025 establishing a federal framework and standardised settlement infrastructure for payment stablecoins and providing the legal clarity that unlocked institutional capital deployment into the RWA tokenization space, BlackRock's BUIDL fund tops the tokenized asset leaderboard by total value locked at USD 2.88 billion, BCG estimated the real estate tokenization market growing from approximately USD 120 billion in 2023 to USD 3.2 trillion by 2030 at approximately 49% CAGR, TVL in the RWA tokenization sector hit USD 65 billion in 2025 per RWA.xyz on-chain market data with 800% growth since 2023, as of June 2024 nearly 12% of global real estate companies had already adopted tokenization with 46% in the pilot phase, and Aave Labs launched Horizon in August 2025 as a dedicated institutional platform targeting stablecoin loans collateralized by tokenized real-world assets confirming that real estate tokenization has crossed the threshold from conceptual innovation to production-scale institutional deployment at the speed of a once-in-a-generation paradigm shift in property ownership and capital market structure.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

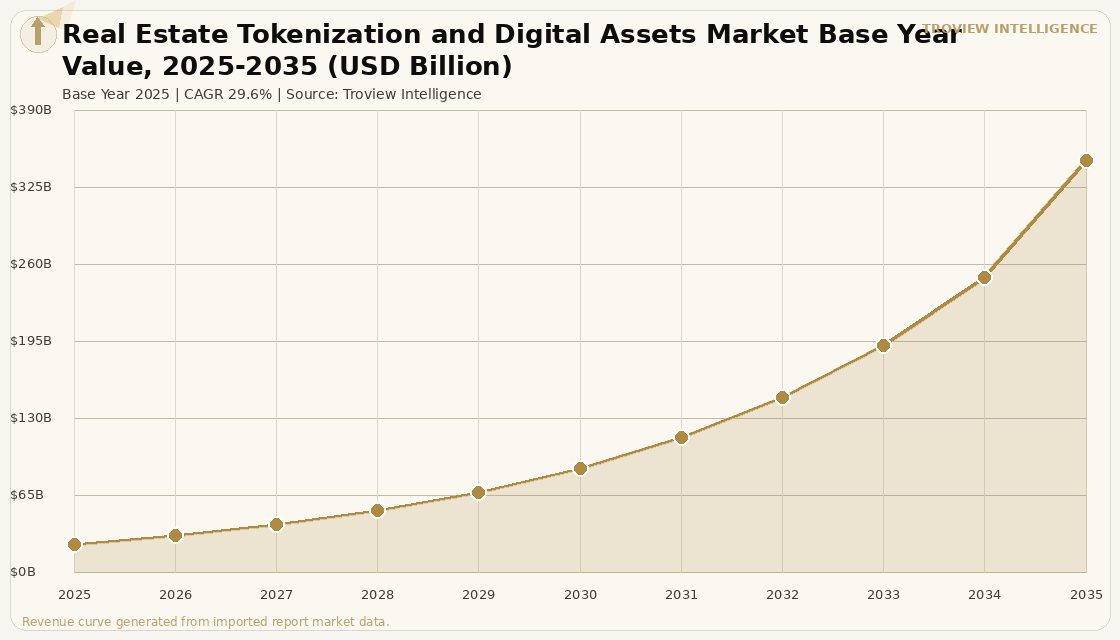

MARKET SYNOPSIS

The global real estate tokenization and digital assets market size was USD 24.18 Billion in 2025 and is expected to register a revenue CAGR of 29.6% during the forecast period, reaching USD 348.42 Billion by 2035. The 2025 market estimate is grounded in verified market data: the total value of non-stablecoin tokenized real-world assets grew from approximately USD 5 billion in 2022 to approximately USD 24 billion by mid-2025, a 380% increase in approximately three years per RWA.xyz on-chain market data; RWA token value on public blockchains neared USD 18 billion by June 2025 per Chainalysis 2025 crypto market report; and total value locked in the broader RWA tokenization sector hit USD 65 billion in 2025 with 800% growth since 2023 per RWA.xyz on-chain market data. The market encompasses the investible revenue-generating ecosystem of real estate tokenization platforms, on-chain property tokens, digital real estate securities, tokenized real estate investment funds, smart contract infrastructure for property transactions, and advisory and compliance services supporting the conversion of traditional real estate ownership structures into blockchain-based digital asset formats. Market revenue growth is anchored in the compound acceleration of three simultaneous forces: the legislative clarity created by the GENIUS Act passage in July 2025 establishing a federal stablecoin framework that unlocked institutional capital deployment at scale, the institutional conviction of the world's largest asset managers with BlackRock's BUIDL fund topping the tokenized asset leaderboard at USD 2.88 billion in total value locked, and BlackRock, Fidelity, Apollo, and JPMorgan all launching tokenized fund initiatives and the structural economic advantages of blockchain-based real estate ownership that reduce settlement from months to hours, enable fractional investment from a few hundred dollars, and create 24/7 tradable real estate positions that conventional property investment cannot match. Deloitte's Center for Financial Services projected in its April 2025 report that real estate tokenization could reach USD 4 trillion by 2035 growing at a compound annual rate of 27% from current levels under USD 300 billion, citing the automation of complex financial agreements through coded on-chain rules and the three-pronged evolution of tokenized property across private real estate funds, securitised loan ownership, and under-construction or undeveloped land projects. For instance, in August 2025, Aave Labs, United States, launched Horizon, a dedicated platform targeting institutional borrowers to access stablecoin loans collateralised by tokenised real-world assets including US Treasury products and other institutional-grade RWAs, reflecting the USD 26 billion RWA tokenisation market at the time and providing institutions a mechanism to deploy capital efficiently on-chain per Coinbase and Chainalysis institutional research. These are some of the key factors driving revenue growth of the market.

BCG's analysis estimated that the real estate tokenisation market will grow from approximately USD 120 billion in 2023 to USD 3.2 trillion by 2030, indicating an average annual growth rate of approximately 49% per BCG Global Asset Tokenisation Report 2023, positioning real estate tokenisation as the fastest-growing sub-segment of the broader tokenised real-world assets universe that expanded 308% over three years to USD 24 billion as of 2025. As of June 2024, nearly 12% of global real estate companies had already adopted tokenisation while 46% were in the pilot phase per Deloitte Global Blockchain Survey 2024, confirming that the majority of global real estate enterprises are already engaged with tokenisation technology even before widespread regulatory clarity had been established, suggesting that the post-GENIUS Act and post-Australia Digital Assets Framework Bill regulatory environment will accelerate the transition from pilot to production across the majority of global real estate firms. Private credit accounted for 61% of tokenised assets and treasuries for 30% per Coinbase institutional research and RWA.xyz on-chain data for April 2025, with real estate representing the primary non-financial tokenised asset category and the one most directly connected to the USD 38.1 trillion global commercial real estate value base that represents the tokenisation opportunity at full penetration. These are some of the key factors driving revenue growth of the market.

However, the global real estate tokenisation and digital assets market faces structural constraints that limit the pace of adoption and investible market expansion through the forecast period. Asset custody, regulatory clarity, and default scenarios in tokenised real estate remain the three primary challenge areas identified by Deloitte in its April 2025 real estate tokenisation analysis, as the conversion of physical real estate title a jurisdiction-specific legal document registered in a government land registry into a blockchain-based digital token requires legal engineering that connects the on-chain token to an enforceable off-chain property right in a way that has not been uniformly tested in national courts across the 40-plus relevant jurisdictions where property tokenisation is commercially meaningful. Blockchain interoperability restrictions limit tokenised real estate scalability, with private blockchains often incompatible with each other and a tokenised real estate fund on Ethereum unable to integrate with Polygon-based DeFi protocols per global RWA market analysis, creating fragmented secondary market liquidity that prevents the continuous price discovery and instant settlement that tokenisation's theoretical benefits promise. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect the operating costs of the blockchain infrastructure supporting real estate tokenisation platforms including the data centres and server infrastructure whose 24-hour computational operations for smart contract execution and blockchain validation consume energy at above-average rates linked to LNG-dependent electricity grids in Asia Pacific and Europe. These factors substantially limit global real estate tokenisation and digital assets market growth over the forecast period.

Real estate tokenisation has crossed the threshold from concept to institution in 2025. BlackRock is not running a pilot. JPMorgan is not running a pilot. Aave launching Horizon for institutional stablecoin lending against tokenised real-world assets is not a pilot. The GENIUS Act is not a pilot. Australia's Digital Assets Framework Bill is not a pilot. These are production-scale infrastructure decisions made by the largest financial institutions and the most consequential legislative bodies in the world. Deloitte projecting USD 4 trillion by 2035 at 27% CAGR is the most credible long-range forecast in the market because it is grounded in the specific mechanics of how tokenisation improves the economics of the three largest categories of private real estate finance fund ownership, securitised loans, and land development. The BCG projection of USD 3.2 trillion by 2030 at 49% CAGR implies that even conservative institutional adoption scenarios generate multi-trillion dollar market sizes before the end of the decade. The disagreement between Deloitte and BCG is not about direction or order of magnitude. It is about pace. Both projections confirm that real estate tokenisation will be one of the largest financial market structure transitions of the next decade." Troview Intelligence Head of Global Real Estate Tokenization and Digital Assets Research

SEGMENT INSIGHTS

Four Regions Defining Global Real Estate Tokenisation Market Development

| North America Global Share 2024 | BlackRock BUIDL TVL | GENIUS Act | Propy 2025 |

| 38.8% of global tokenised asset market (Market.us) | USD 2.88 Billion largest tokenised asset fund | Passed July 2025 federal stablecoin/RWA framework | USD 4 Billion+ in blockchain property transactions |

North America leads the global real estate tokenisation market with a 38.8% share, anchored by the United States' institutional tokenised asset ecosystem that includes BlackRock's USD 2.88 billion BUIDL fund, Securitize as the administrator of the largest tokenised fund offerings, JPMorgan's blockchain tokenisation infrastructure, and Franklin Templeton's tokenised government money fund. The GENIUS Act's passage in July 2025 established a federal framework and standardised settlement infrastructure for payment stablecoins that directly addresses one of the primary institutional barriers to tokenised real estate adoption the absence of a stable, federally regulated on-chain settlement medium with the act's passage cited by Chainalysis as triggering the acceleration of capital into the RWA space that was visible in the latter half of 2025's on-chain RWA market data. Propy, United States, facilitated over USD 4 billion in blockchain property transactions in 2025 including celebrity listings by Grant Cardone per Zoniqx platform analysis, demonstrating that commercial-scale tokenised real estate transaction volumes are achievable in the current US regulatory environment even before full GENIUS Act implementation.

| Switzerland / Singapore | Australia Digital Assets Bill | ASIC INFO 225 Update | No-Action Position |

| Regulatory leaders DLT Act, MAS framework | Passed both houses April 1 2026 AFSL for tokenization | October 29 2025 tokenised real estate example added | ASIC sector-wide no-action until June 30 2026 |

Europe and Asia Pacific constitute the two fastest-growing regions for real estate tokenisation adoption, with Switzerland's DLT Act providing the most comprehensive property tokenisation legal framework in Europe and Singapore's Monetary Authority of Singapore framework establishing the most institutionally mature tokenisation regulatory environment in Asia Pacific. Australia passed the Corporations Amendment (Digital Assets Framework) Bill 2025 through both houses of Parliament on April 1 2026, amending the Corporations Act 2001 and the ASIC Act 2001 to bring digital asset platforms and tokenised custody platforms into Australia's financial services framework per Tokenizer Estate reporting, with the legislation specifically covering real world assets including bonds, property, and commodities represented as tokens. ASIC updated its Information Sheet 225 on October 29 2025 to add tokenised real estate as a new example category per Global Regulation Tomorrow analysis, with ASIC Commissioner Alan Kirkland confirming that distributed ledger technology and tokenisation are reshaping global finance and that ASIC's guidance provides the regulatory clarity that firms have been calling for to innovate confidently in Australia.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from Deloitte Center for Financial Services, Chainalysis, ASIC official releases, CoinDesk, Tokenizer Estate, and verified platform reporting.